I actually think I made one mistake

The number of replacement shares wouldn’t depend on actual value of DRPF shares but the NAV value of DRPF shares

So 100 CHF of DRPF would mean 75 CHF aid DRPF based on NAV and this results in 15 shares of NEWFUND

I actually think I made one mistake

The number of replacement shares wouldn’t depend on actual value of DRPF shares but the NAV value of DRPF shares

So 100 CHF of DRPF would mean 75 CHF aid DRPF based on NAV and this results in 15 shares of NEWFUND

Checked a few fund mergers. All happened at NAV ratios.

Current NAV premia

| ISIN | Bloomberg | NAV | Px | Premium |

|---|---|---|---|---|

| CH0026465366 | DRPF | 14.56 | 18.8 | 29.1% |

| CH0100612339 | STA | 108.89 | 124 | 13.9% |

| CH0031069328 | CSLP | 110.39 | 146 | 32.3% |

| CH0118768057 | HOSP | 76.19 | 94.6 | 24.2% |

| 29.5% |

With that STA (Residentia) still the cheapest despite 25% jump on Friday.

NAV weighted average premium currently stands at 29.5%. There is borrow and short selling possible on CSLP and DRPF.

Thanks for sharing

I would be happy to see how shareholders of DRPF & CSLP react to this & if UBS would share any presentation publicly. I hope so

Since premium is not only market sentiment but also includes things life deferred capital gains, I think market already did the math for us and priced all these Funds where they should be.

Such mergers would need some sort of voting by shareholders , right?

Skimmed the prospectus, that doesn’t seem to be the case. The fund direction can do it (if the funds are similar enough and have the same direction, which I assume is the case for UBS/CS funds), I think it only needs finma approval after that.

Eg check §24 for GREEN.

Yes, that’s how I read it as well

Only the funds that are a SICAV have shareholders votes generally speaking. This is the case for Procimmo, Bonhote, Edmond de Rotschild and soon for Streetbox next year.

I still cannot comprehend though, how is following possible . A fund trading at premium to NAV is merged with a fund trading at Discount to NAV using NAV as exchange ratio.

To make is clear, let me try to explain a bit with an example.

How is this possible & am I understanding this whole situation correctly? It would be great if someone was expert in M&A and clarify how these things are possible.

In my mind, above will only make sense if NAV is the only real value & everything else is fictional number. But we know that every fund in Switzerland for real estate is traded at AGIO which is on average is higher than 20% (perhaps much higher for RESIDENTIAL funds). Does it mean that AGIO is a pure market premium and can disappear with actions like mergers ? This would make investing in these funds very risky.

Of course the agio can dissapear in litteral seconds

My personal take is that indeed those funds are riskier and can trade away from fundamentals (like most/all closed end funds). Also given that the rebalance on friday took quite some time (and it’s not always very liquid), I don’t necessarily believe everything is fully priced it (even the merger).

What I’ve heard make sense is that you should keep those for decades and buy them for a given yield (so you don’t care that much about the market value but more about the cashflow it generates). The value will change but the dividend amount is pretty stable (I guess like some kind of riskier bond).

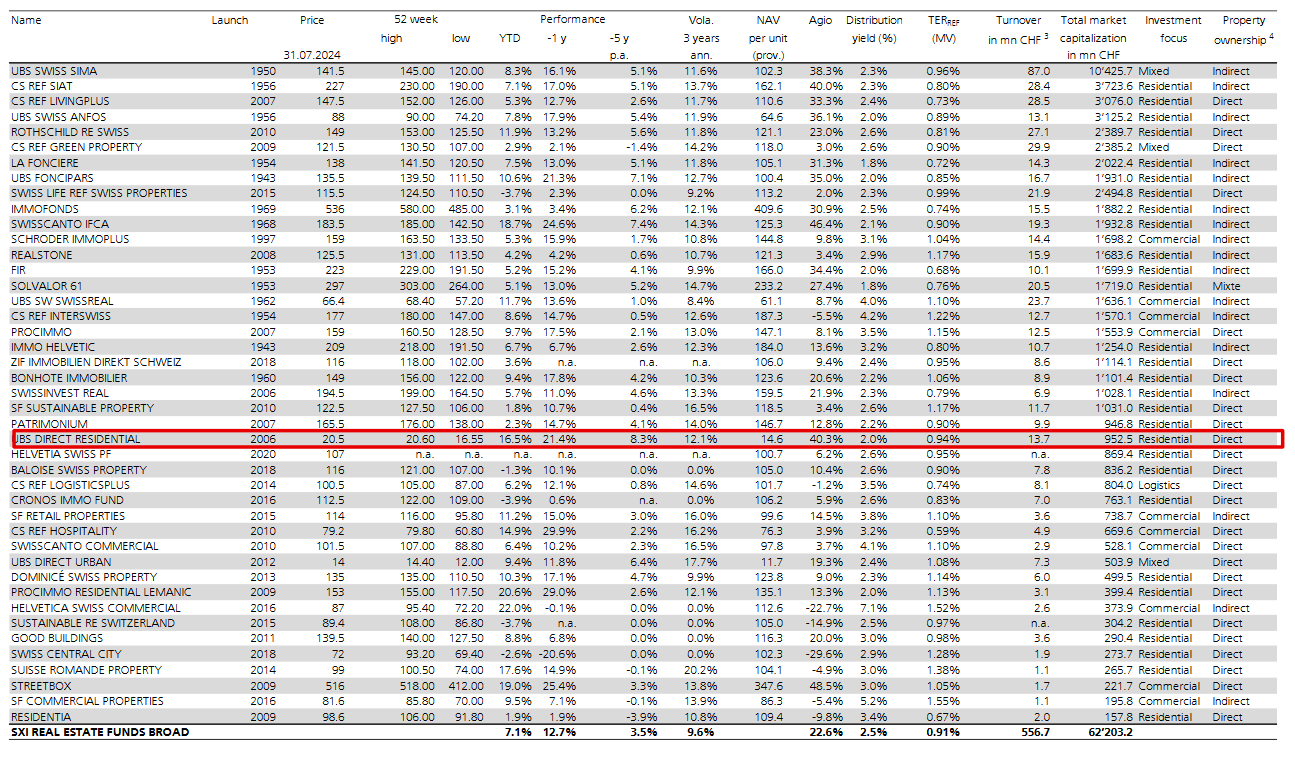

UBS Direct Residential new issue presentation had a nice overview of RE funds, direct and indirect with their premia etc.

There seem to be direct residential real estate funds with all kinds of premia. Theoretically I would pay more for funds with higher turnover, better risk-adjusted yields, lower fees etc.

Regarding the fund merger discussed above- of course nobody knows what the premium will be on day 1 of the new combined fund. Maybe it’s 40% then nobody loses any money and there are only winners. Maybe it’s -10% and everyone loses money. Imagine you have to place an order on day 1. You probably know the NAV/unit but what limit price are you going to enter? I guess few will be willing to sell the unit suddenly at 20% less than before, that would speak for a relatively stable premium. The current rapid changes are just because there is an element of technical arbitrage (buy the lower premia funds, sell/short the others). Most fundamental long only holders of the units probably don’t care. Friday’s volumes were only a fraction of units outstanding for all the funds.

For me, it is mainly a learning experience on how this works. I am happy that I got to learn this before I invested significantly in Direct RE Funds. This also helps me understand the inherent risks of closed funds where fund manager can do whatever they want. I will see how this turns out by 2044 for my holdings in DRPF.

I did some math, and some data collection.

The residential part will be higher than 65%. I looked into it as well. If you check the “mixed use” portions of their portfolios, they give a breakdown of what % of that mixed use is also residential (in the annual/semiannual reports). Basically I counted the reverse, 100% - “Definitely commercial portfolio share”. I.e. landbank I counted into resi as I don’t mind owning land. With that you’re closer to 75-80% residential/landbank.

Ahh I see. Yeah I ignored mixed use . But perhaps it’s also including some residential

Funds like these qualify as active funds, no?

They do. But that’s mainly about what they do within the fund adhering to the strategy.

For example -: if DRPF strategy says that they are majorly residential in German speaking area then I am fine if they buy or sell properties within these boundaries.

However here we have another problem to deal with. Which is that they can just merge with another fund. This means that not only we need to deal with active fund management risk, but we also need to deal with risk of fund house organising their funds.

To be honest UBS merger might not be that bad. But I read that sometime back AXA merged Commercial fund with Residential fund. This is going beyond the fund strategy and just doing whatever they feel appropriate.

Now I know that fund houses are not crazy and they would normally do these things keeping interest of their investors in mind. But this was just a surprise for me that it’s so simple.

Yeah but that’s not specific to these funds. I have had ETFs close down at inopportune times, locking in losses that I didn’t intend to take. AND: it was all in the prospectus.

I think UBS did the right thing here. I mean, 4 fund management teams for 4 funds? Maybe even competing with each other on bidding for properties.

Especially the STA Residentia team, small fund, bad performance (plenty of non performing tenants) etc. Put those properties into the hands of a better team plus you get economies of scale everywhere.

And let’s keep in mind that SNB is heading towards 0. Immigration still strong. Record rent growth. CH resi looks good in the long run.

Agreed

Great thing for STA

Kept following this quite closely.

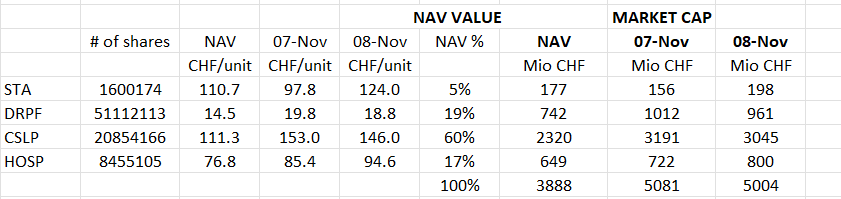

Looks like natural long only buyers/holders bought some CSLP, DRPF- ignoring the arbitrage with STA which is still very cheap vs the others. There are sizeable sell orders on the book in DRPF at around 19.20. Liquidity is rather low now. Wait-and-see it seems. Year end might be a relevant date for some as it is interesting to hold those funds over the year end for (asset) tax reasons.

HOSP drifting higher. STA catching up a little bit today. CSLP also drifting higher. DRPF stuck now with large offers higher up.

The restructuring of the 4 funds will take some months, judging from how long it took for AXA fund mergers, it’d say 4-5 months.

| ISIN | Bloomberg | NAV | Px | Premium |

|---|---|---|---|---|

| CH0026465366 | DRPF | 14.56 | 19 | 30.5% |

| CH0100612339 | STA | 108.89 | 129 | 18.5% |

| CH0031069328 | CSLP | 110.39 | 149 | 35.0% |

| CH0118768057 | HOSP | 76.19 | 96.6 | 26.8% |

| 32.0% |

Hi @DRPF

Thanks for the update, is the 32% capitalization/NAV weighted?

NAV weighted, as it is expected that the funds merge at NAV ratios