I think whenever there is merger or acquisition, the terms can be defined by the company

Agio as we know is not just the market premium to NAV. It also includes capital gains that accrue over the years.

While raising capital to buy new properties , the valuation of new properties was done and then UBS could decide how many shares they wanted to create. They chose to issue new shares at NAV because most likely they expected that they were fairly valued at that price

Now we are talking about merging of funds. The new terms need to be decided. A fund which has a low agio also have a different mix of properties within it. Now the new terms should be decided based on what’s the fair value of these new properties. Fair value is not always NAV. If thats the case then current investors of CSLP & DRPF would not be compensated properly.

I would be curious to see what are the terms. Because I am not sure how this really works. I would be very surprised if deal will be structured in a way that existing shareholders of CSLP & DRPF are losers .

I liked that DRPF & CSLP was majorly residential

I don’t quite understand why they are merging mix use funds ( hospitality & Residential) with residential

It’s on swissfunddata (which is probably something you should subscribe to if you hold that kind of fund, that’s where all the communications get posted)

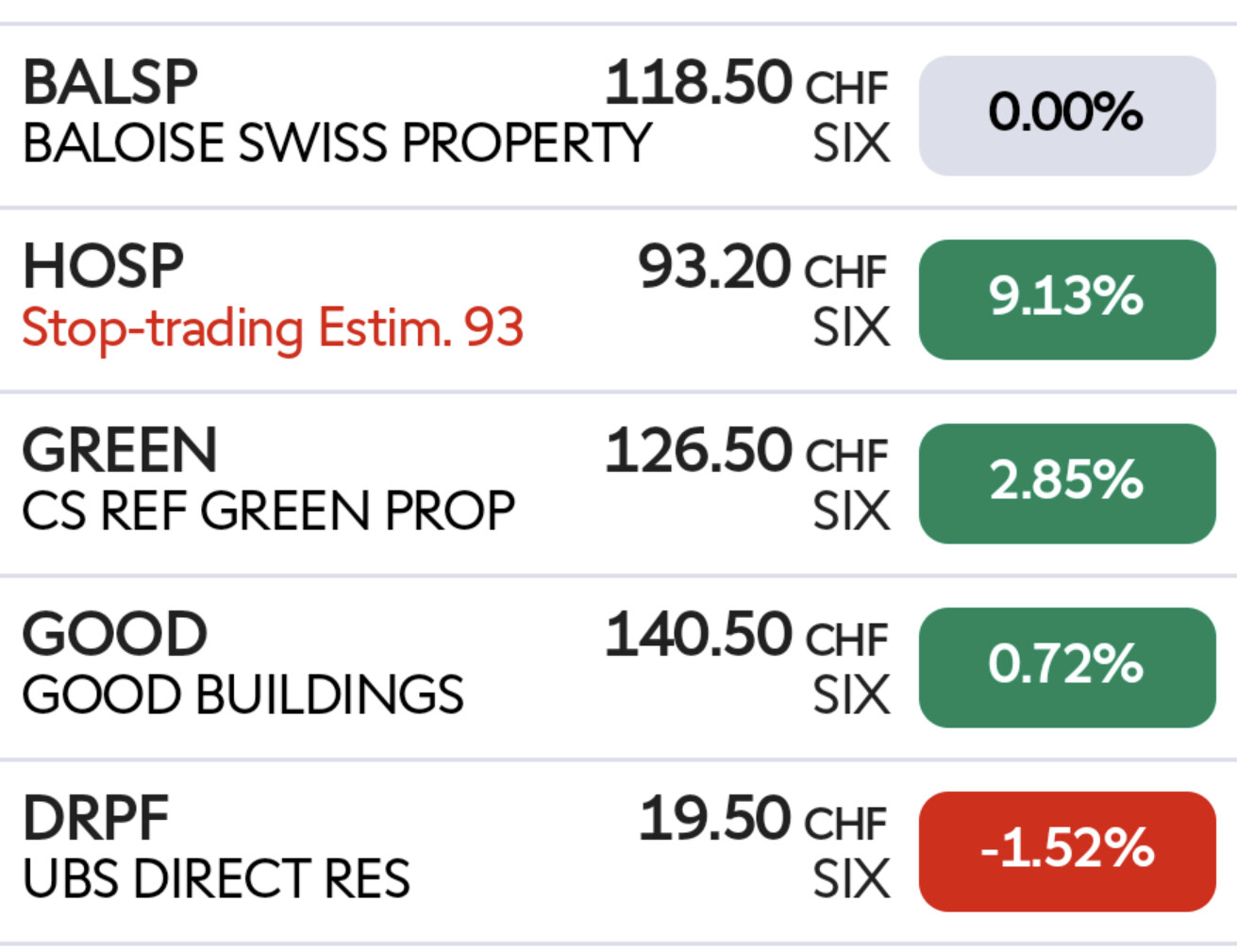

yep, look at those moves for “boring” RE this morning.

Market seems to “know” exchange will be by NAV, not market price. Agio’s narrowing between funds.

The “CS REF Hospitality Fund” is mainly Hotels (for example"25h Hotel" on Europaallee) and some “weird” private hospitals/clinics that one has never heard of (I haven’t, at least). No residential for elderly AFAIK.

DRPF raised recently new capital. This got them new shareholders and average price was about 20 CHF after dilution

Now they announced this merger and don’t provide clear information. If it’s really based on NAV, it is a bit weird that people who own higher quality fund suffer loss versus people who own lower quality fund

I am waiting for details to come. But I think market reaction is simply based on certain assumptions. But how many shares of new company will be given to each investor is still not clear.

I wouldn’t be surprised that DRPF & CSLP share holders would get more shares of NEWFUND and then total value at investor level remains constant. Otherwise investors of CSLP & DRPF would simply lose money which cannot be the purpose of this merger.

I haven’t seen any terms. But hard to argue for market price based exchange ratios. UBS Residentia barely traded. DRPF traded much more and it is nobodies fault that people paid 40% premium while the average SXI Real Estate fund premium was 22%.

Edit: Axa funds merged at NAV ratio

Edit 2: UBS Direct residential DRPF sale of new units recently was at NAV

I don’t think one can compare the average AGIO in Swiss real estate index . DRPF is a 82% residential fund and it also have older buildings. If a fund is completely commercial, the AGIO will be close to zero. Residential real estate is worth higher in CH and that is reflected into Agio.

The assets of CSLP & DRPF account > 80% of the new fund (based on NAV). I cannot imagine that this merger is designed to disappoint 80% of the owners and please <20% of the owners (of Residentia , HOSP)

I understand that NAV might be the logic for share distribution in the end. But I just find it a bit illogical.

If NAV is the eventual logic for distribution ratio , this whole merger would only make sense if the final entity is better than every individual entity. Or else this is a value destruction exercise for majority of shareholders & UBS should explain the rationale clearly.

P.S -: no wonder DRPF is the most hated stock today out of all four of them

I understand. My point right here is that you can buy STA at 14% premium right now. The premium of the new fund is up to market forces. I agree pure residential has the highest premium.

Also note, CS Living Plus is by far the largest fund and somehow it’s holding on to a 31% premium with live quote. DRPF is already below that.

Smallest premium still is STA

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.