There are quite a bit more pages than 100 but they’re written in a big font.

Otherwise, I fear you’ll have to be a bit more specific, unless one of the AI gurus manages to make that magic “search without knowing what you’re searching for” sauce I’ve been touted work.

I’m taking this to mean I know how to use AI (in this case Copilot) to find things and feel vindicated that my feeling, that it may be useful for some fringe cases but is widely overused for 95% of what it’s used for currently by individuals and not specialized companies, doesn’t come from a place of ignorance.

AI-usefulness-sceptic here, so I googled “book about investing psychology free pdf” and the Nofsinger book was at 6th position. Did AI actually spit it out on top/indicate strongly, or did it also give a list which you then picked from?

What I have noticed is that they always maintain a home bias (which I previously thought was not good idea , but now I think it is)

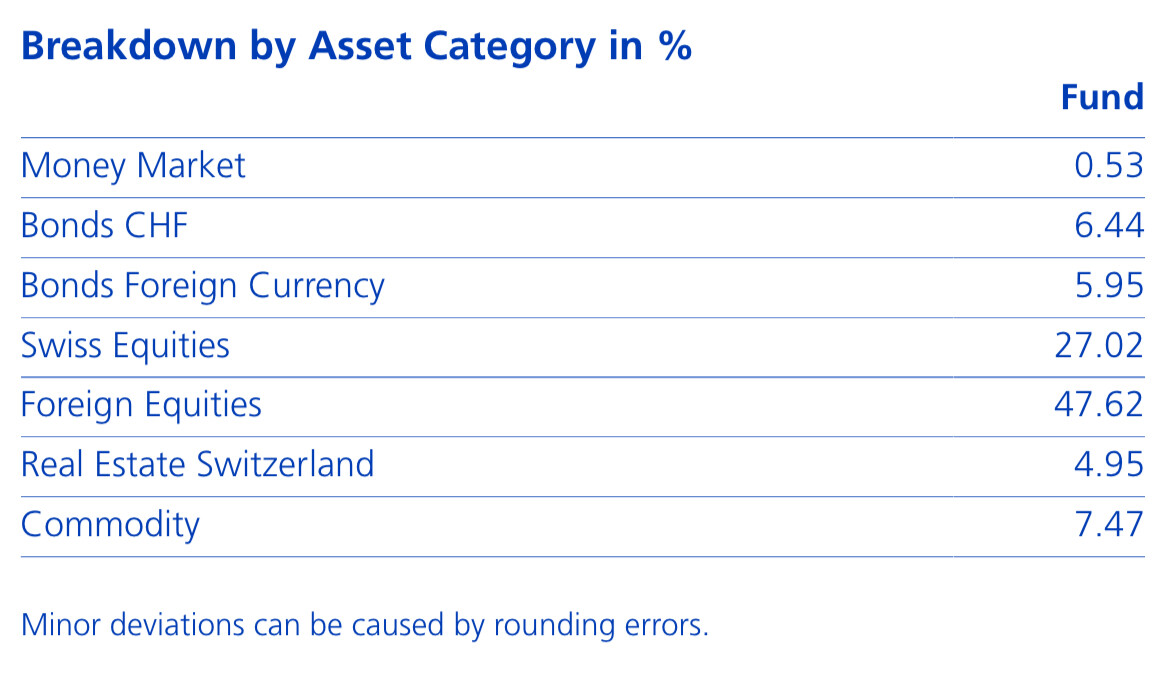

Active versions also keep an eye on what is more interesting at the time. But if we just look at passive ones, following is allocation for Frankly 75.

I noticed that Swisscanto funds always have a portion for commodities (includes precious metals) in screenshot

All their foreign bonds are hedged which makes sense and has been common advise. It’s not specially mentioned here but if you look at UBS Vitainvest, they always hedge foreign bond exposure.

This is just to get some ideas. Not to copy them completely.

Home bias is good as long as the shit show doesn’t take place in your own country - which should also never be ruled out. As an asset manager, however, there is certainly less blame to go around if the home bias makes losses than if the international part makes losses (People often perceive their own country as safer, partly because they are involved in its politics). From this perspective, I understand why many 3a providers, asset managers etc. have a very high home bias as standard.

I agree that familiarity & feeling of being safe drives a lot of this.

But I think there is more to this. These wealth management firms are in business for many years and have a lot of research. I think either based on research or intuitively they have been following right approach

Recent paper on equity portfolios shows that 35% home bias is optimal base case.

I think this is an important point often dismissed in the quest for efficiency. On the one hand wealth/asset management, advisors, “advisors” have indeed fleeced investors for many decades via ultra high costs and shit funds, on the other I still argue that doing something, even inefficient, is better than doing nothing. Even 3a with life insurance - and I am a zealot against 3a with life insurance!

Possibly a sign of maturity, or Dunning-Kruger effect, is in fact going past the neophyte stage where one thinks they have it all figured out and become more open to different opinions. I think one should pause for a bit before blurting out that UBS, JPM, Pictet etc etc and even Zurich, Helvetia, SwissLife and the like don’t know what they’re doing.

Oh, they know exactly what they’re doing. They’re ripping off their customers.

That could still mean that some clients are better off paying 200.-/month into a 3a life insurance from age 30 to 65.

Because even if they don’t get back more than the 84k they paid in, they may have 84k more for their retirement than they would’ve had without that 3a product (because they possibly wouldn’t have saved anything).

I think we should be careful while labelling people “rip off”. 3a insurance is a bit of different thing because some agents are misleading people. But the actual financial product does what it is supposed to do. Insurance costs money and hence it cannot be compared to Investment portfolio. Active wealth management costs resources and cannot be compared to DIY index investing.

Paying for a service is not the same thing as being ripped off. Customers are free to choose between different providers or choosing to DIY. The choice is based on individual`s knowledge, willingness & confidence while dealing with financial markets.

We can say asking for 1-1.5% fees for wealth management is high fees. But how many people know about investing anyways? If you do not know how to do things yourself, you need to pay for someone else to do it. This is the basic principle of business. Value creation costs money or time.

This is true everywhere. Amazon & Uber charging 20-40% commission to connect the buyer with seller, a painter asking for a price to paint our house or even the hair salon charging a fee to cut hair. Everything can be done for cheap or for free but it all depends on how effective it is.

Index funds have made investing easier for people but there are still many who do not know anything and do not feel comfortable with DIY style.

fwiw, I think you should take that in the context of the baseline historically being close to 100% domestic in many countries.

Any low home bias (low being below 50%) is people trying to convince their customer to reduce home bias. (I’m personally still not super convinced by the value of home bias, esp. for smaller economies, still feel like a lot of it is driven by US exceptionalism in past century, which biases the modeling)

Mostly this, exactly.

And from many talks with friends and collegues, they all had no clue what they were paying for und how much they were paying for it → both for 3a insurances and expensive balanced mutual funds.

As an example: Not one person knew about issue surcharges when investing into a fund. And even I have to dig deep, to actually find out about the fee.

So while there is nothing wrong with ‘paying for a service’, it does show that many people pay for a service they never asked for and/or are not aware of.

And that is - in my eyes - closer to a rip-off, than just a service.

Don’t get me wrong - for the majority of people a low cost robo-advisor is probably the best solution for them, in which cases they pay for a hands-off-solution.

But knowing so many people who own products they don’t have the slightest clue about, leaves me with the believe, that some companies try to take advantage of their non existent knowledge.

The “rip off” part of life insurance products is also due to other factors, such as the very agressive marketing full of lies (calling foreigners having just settled here, pretending to be “official” and selling them the products lying all the way). Or also the fact that the insurance premium is way too high compared to what’s insured in comparison with a life insurance not part of a 3a.

While I agree with the added value of someone handling things for people without a financial education, I still see these 3a life insurance as complete scams. This value applies more for managed funds, robo-advisor, etc.

It’s fairly correlated especially given how globalized things are those days, so probably some amount of home bias won’t hurt.

I definitely wouldn’t recommend with high level of home bias (> 50% which has historically been the case for many people), unless there’s non economic reasons (e.g. tax benefits, not allowed to invest, etc.).

(I’m personally not sure the standard US view to be 100% US is so wise, it’s served people well in the past 50y, but not sure why it will continue over performing, it’s the same as the people working in big tech that never sold their RSUs )

I think CH is somewhat large, but dominated by a few giant, so if you add home bias tilt you won’t want to invest in the megacaps. Once you remove the megacaps isn’t CH stock market kinda small?

iirc the paper doesn’t compare to global equity, only to a rebalanced domestic vs. international portfolio.

(and I skimmed it again, in my opinion you need to read this in the context of US investments where most people are 100% domestic, they repeatedly mention that many investors have no or way too low international equities, so they don’t even try to compare to global equity).\

Also personally still not fully convinced by the methodology, to recap here’s how they select the series:

We adopt a stationary block bootstrap approach in the spirit of Politis and Romano (1994) to draw a time series of monthly real returns for the four asset classes that covers the couple’s lifespan.

We randomly select a starting country-month observation in the full sample and draw a block of consecutive monthly returns from the same country to capture time-series dependencies in asset returns. The block length is drawn from a geometric distribution. The average block length is 120 months in the base case, so the blocks reflect long-term time-series properties of returns

it seems to me anytime you hit the US in a serie you’ll have a case of domestic dominating, not sure that’s how it plays out in practice.

I don‘t see any real advantages for Swiss investors. We pay taxes on dividends, we don‘t pay taxes on capital growth. So dividends are an unnecessary tax drag.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.