If I remember correctly, you still have to declare the gross dividend. However, you can deduct the US withholding tax in 16.3 “Kosten für die Verwaltung des beweglichen Privatvermögens”.

It’s not just in ZH, it’s the same for everyone.

The form on the estv website lists 100 CHF as the minimum refundable amount, it also confirms that if the amount is smaller you can just declare the net dividends instead:

I have read the tax guide for Swiss investors several times, however there is one thing that I do not understand, maybe you can enlighten me.

Using the Degiro annual report, I have therefore just entered in Getax (I am in Geneva yes :-), each title I own.

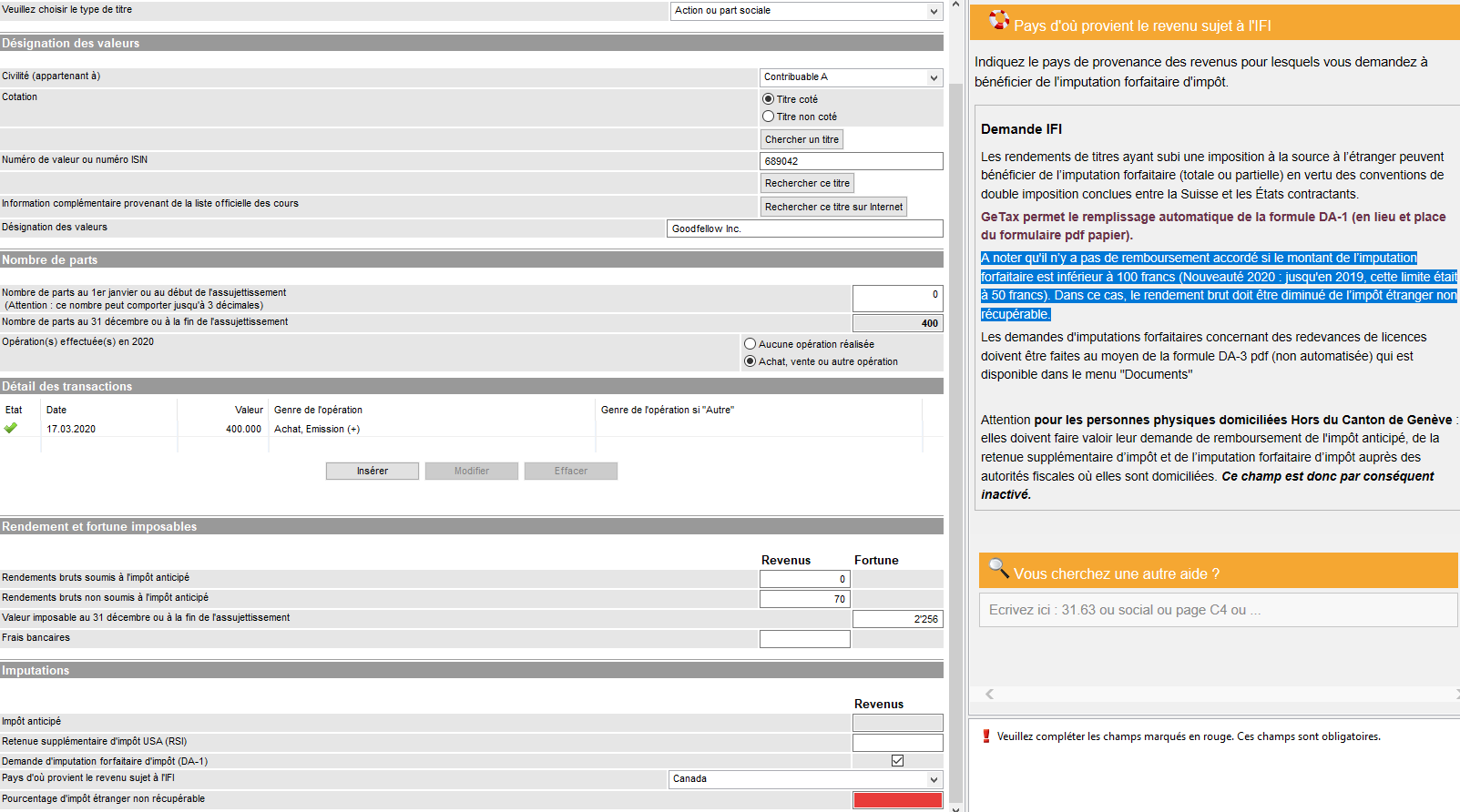

Take the example, below, foreign title → Goodfellow CA38216R1001 / domicile of the title = Canada → 25% non resident (PWC)

In the explanatory text, they say that “il n’y a pas de remboursement accordé si le montant de l’imputation forfaitaire est inférieur à 100 CHF. Dans ce cas, le rendement brut doit être diminué de l’impôt étranger non récupérable.”

When the AFC talks about this imputation, I guess he is talking about the dividend. In my case 70 CHF <100 CHF, in this case the gross return must be reduced by the non-recoverable foreign tax.

By going to see on PWC, I saw that there is a convention against the double taxation of 15% between the CH andCANADA, the tax is reduced by 10%.

How do you proceed in this scenario? Cf image at the bottom “Pourcentage d’impôt étranger non récupérable”, suddenly no check mark for the DA-1 form and we make 70x0.10 = 7

70-7 = 63 CHF gross returns not subject to IA correct?

If let’s admit my dividend amounted to 1000 CHF

CH whithholding tax 1000x0.35 = 350 CHF

CANADA withholding tax = 1000x0.25 = 250 CHF given the agreement I simply fill in the 10% non-recoverable tax percentage Getax right?

The 100 CHF limit applies to the total of the foreign withheld taxes that you can claim back.

The assets you’ve listed in your example will contribute for 70x0.15=10.5 CHF to this limit, this is assuming that you had 15% withholding taxes for Canada (didn’t check this).

You’ll need to do the same calculation for all the eligible assets, if when you add them all up you’re above 100CHF then you can go ahead with the DA-1.

If the total is below 100CHF you cannot claim back the withholding tax through DA-1, in that case instead of reporting the gross dividends in the tax declaration you can just declare the net dividends.

Thank you very much for your complete answer I understand better. I also called the taxes, even if the limit is not reached you can fill in by checking the form. In this case, given the 15% agreement, the non-recoverable part amounts to 10% to be entered in Getax and the amount will be deducted automatically.

If the limit of CHF 100 is not reached, this will be rectified by taxes.

As far as I know, it’s lost. However, you can deduct the CHF 81 as part of “Kosten für die Verwaltung des beweglichen Privatvermögens (weder rückforderbare noch anrechenbare ausländische Quellensteuern)”. I.e., at least you don’t have to pay Swiss taxes on that part.

1 Like

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.