I’ve been reading a lot of threads here, and the consensus seems to be that currency hedging comes with a cost and usually doesn’t pay off long term. Makes sense.

But I went on TradingView, compared ACWIS (hedged) vs ACWI (unhedged), and made sure to convert both into the same currency (CHF → CHF, so no CHF vs USD ).

The result? Over the last 10 years, ACWIS seems to have outperformed ACWI by almost 30%.

I suppose the UBS product you use is quiet expensive. They combine two bets, stocks and currencies. But then the Dollar was at CHF 1.03 at the beginning of your chart and is now at CHF 0.80, a big difference that seems to have been eaten up by the costs.

It comes up all the times here. I should keep a reference of my comparison of stocks with the Dollar Index. Currency movements are peanuts compared with stock movements. To “hedge” currencies is actually just another bet, added risk because the correlation is low. And it is a bet that can be expensive as you see…

In the case of CHF hedging, it’s a very unfavourable bet, considering the franc’s historical performance. Kinda like hurricane insurance in the Carribean. The premiums will have to cover the sure loss for the insurer, and then some.

There are probably some currency pairs for which hedging really would be a bet, and could pay off if your gamble goes right. But for CHF, it’s hardly a bet.

It is a bet. Always. If you bet on the sun rising tomorrow you probably won’t make much and pay quiet a premium…

If it is that sure just bet on it. But then as you say the bet will probably be expensive. On all currency bets you pay or get the interest difference…

And still a currency bet is always something else than a bet on equities.

That makes no sense, the performance should be better as the CHF gained.

Also I think TER is not the only cost. UBS trades at UBS, one of the most expensive brokers in the world. TER usually contains management fees, administrative expenses and marketing costs, but not trading commissions.

The performance of a hedged fund is only better if the CHF gained more than what the market already priced in, which is roughly the interest rate difference (as far as I know, hedged funds commonly use rolling 90 day forward contracts but I’m not familiar with the details). That’s if there are no fee differences. The TER may also have been reduced over the years.

Sorry, I am too stupid to understand this. You basically make two bets: stocks rise and CHF rises. You do this with a single product and… abracadabra… 1+1=0.5.

If I understand you correctly you say the actual price of CHF was already priced in 10 years ago? For me it looks more like the costs charged for that two-in-one product were way higher than the gain. Just imagine the CHF would have lost value too.

OK, thank you very much, now I think I understand. The interest rate difference multiplied by 10 years was way bigger than the gain of the CHF against the other currencies, mostly USD, and that explains the worse performance. In other words it is not 1+1=0.5 but 1-0.5=0.5.

Conclusion could be correct, but I think the comparison is flawed.

Chiefly because returns must always be compared on a risk-adjusted basis.

(Furthermore, the comparison involves different domiciles, providers, WHT…)

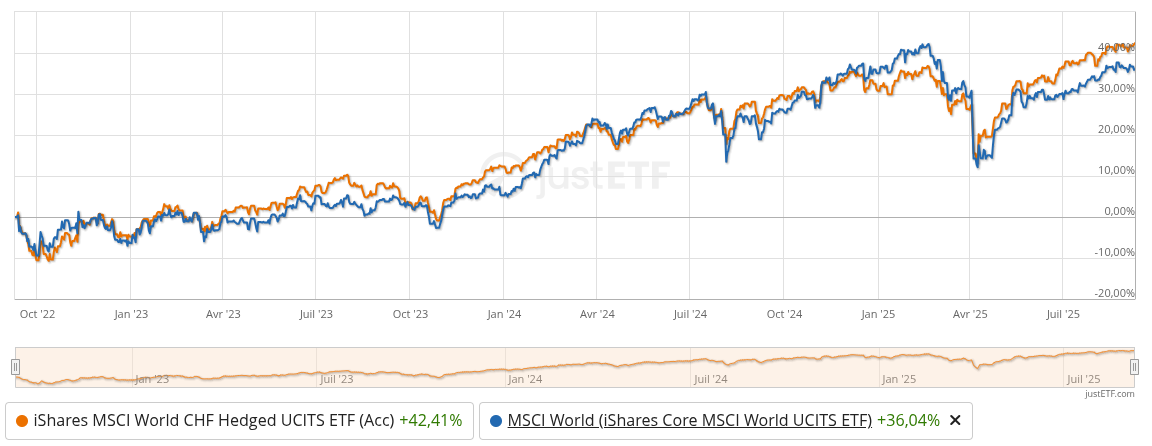

I’m attaching this screenshot of two ETFs from the same provider (iShares), both accumulating, with the same domicile (IE), over the past three years.

Doing so to illustrate that it’s more complex than comparing two lines. I don’t think one should reach a conclusion from this graph either.

If you are curious to hear a case in favor of hedging currency, see, e.g., this post by TrueWealth. I think their approach is sound. TL;DR: TW uses risk tolerance to determine the stock proportion. For a given risk level, hedging allows increased exposure to US stocks.

The Black paper (cited in the link) is a good starting point to debate hedging, but 40y later it don’t know if it’s that applicable.

Eg:

Foreign investors investing in the US or Japan, however, generally expect to see lower volatility without hedging and may be happy to forgo hedging. This also applies to investments that are dominated by US equities such as global cap-weighted equity indices

Also the model used by Black is heavily simplified and doesn’t take into account things like long term reversion to the mean of currencies (I think it’s not super controversial now to say that for long term investments equity hedging isn’t necessarily beneficial)

(Also with so many global companies, I don’t know if it’s even meaningful)

Over longer periods of time -: Hedging cost should more or less be similar to currency devaluation. Atleast that’s what is based on market expectations.

The difference comes in TER% of hedged products. I think UBS WORLDis a better hedged product for MSCI world exposure after UBS reduced their fees last year . It’s TER 0.09% is quite reasonable.

Personally I don’t hedge equities exposure because I think international investing has its pro & cons and currency risk is one of them. If I chose to invest in foreign equities , I need to bear the risk of currency too.

As I already said, it is not a hedge but an additional bet. You do a negative carry trade CHF-USD, had to pay the interest difference and got the value difference.

It is an additional bet with additional risk. But usually currency bets are way higher (and probably of shorter duration), because the currency movement is peanuts compared with the stock movement. And long Term you lose, just because of the higher cost of a hedged fund.

My point was actually to say that one can’t determine whether hedging “works” by comparing graphs of past returns. Returns need to be compared on a risk adjusted basis.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.