I wonder if Nikkei basically is a broken market for last 30 years, does it mean that there should be a lot of value stocks there? I mean it has really bad press, so I’d expect the stocks are under valued.

I don’t know in what world you are living? The only thing that is guaranteed is that someday you are going to die, like the rest of us. There is no premium without risk. You want ~0 risk? Keep all your assets in cash in Kantonalbanks. You get 0 premium. Real estate has a pretty poor risk/premium ratio, you are basically getting less returns than equities but the same volatility as real estate is extremely correlated with stock markets. Bonds nowadays offer real negative returns. Gold has no real expected return, it doesn’t produce anything and in the best case will just cover inflation.

There are basically no alternatives to stocks.

@1000000CHF

It has. If you look at exUS value ETFs, a big part of it will be in Japan. Here is a known exUS small value ETF: https://www.avantisinvestors.com/content/avantis/en/investments/avantis-international-small-cap-value-etf.html

1 Like

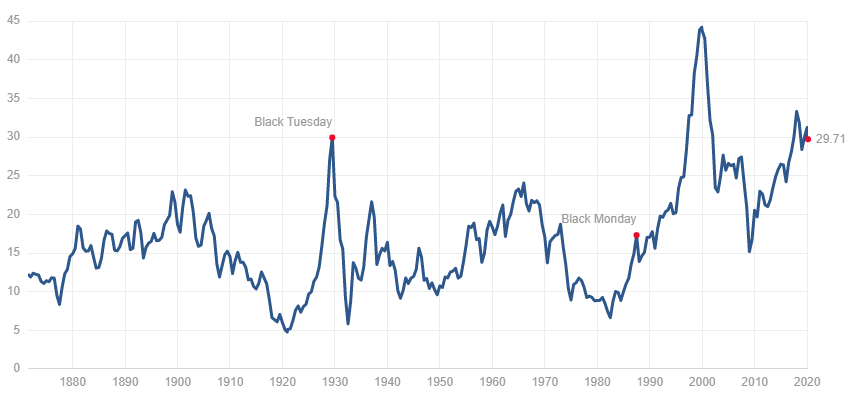

Guys, Nikkei had a P/E of 95 (!!!) in 1990. It indeed took 30 years for the valuations to retrace back to world averages. It’s now at around 18 which makes it good value. US is priced at a premium because earnings growth is higher. Markets really are NOT detached from fundamentals nowadays.

4 Likes

We must have clearly different statistics on that point. What are your figures?

Caution: “return” is ambiguous: do you mean by “return” the yield (the cash you get from your investment) or the price appreciation, or a mix of both?

Yup, see here:

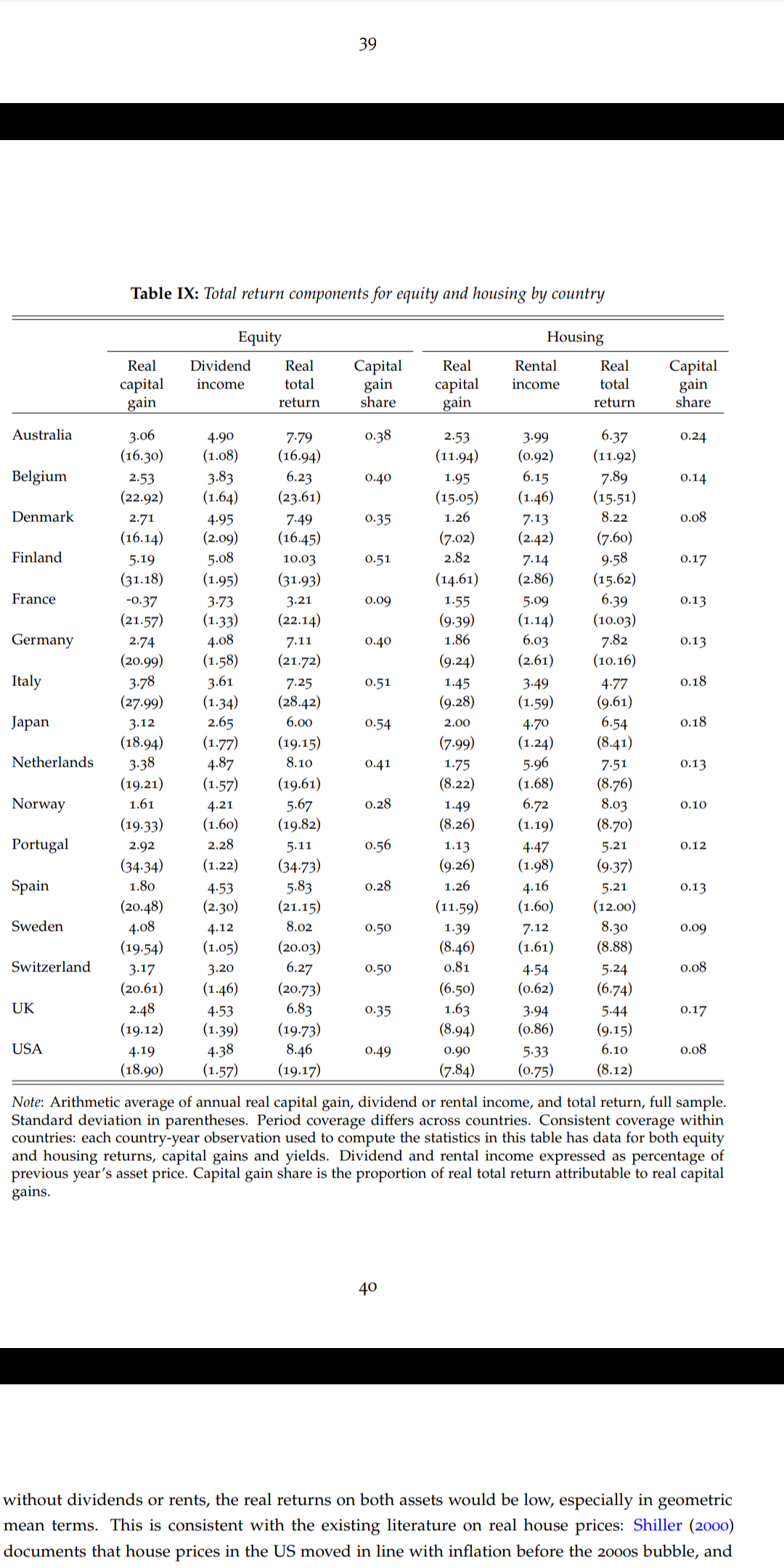

There was a study from Harvard analysing rate of return of different asset classes for 150 years in 16 different developed countries. The conclusion was that the return from real estate appreciation was close to inflation but the return from renting was in most countries better than from stocks (and it had smaller volatility). Best country for stocks was US (for obvious reasons - biggest, most profitable companies in the world), worst was France (due to series of nationalisations by socialist governments). Good example of stocks returns was also Finland because during this period it turned from 3rd world country to Nokia.

PS. Here’s the data:

2 Likes

OK, not exactly the same thing. EPS have climbed due to the magic of share buybacks, but it makes sense to compare them to the index. All is good!

Indeed. Fundamentals stick. Probably will not work the same for Nasdaq, but I would expect Nasdaq to follow the PEG (price to earnings growth) ratio due to the consituent structure. As you say, all is good, keep on investing.

but does it make sense to compare earnings per share? S&P 500 is not equally weighted like DJIA, it’s market cap weighted. Why not just look at the Price / Earnings or CAPE? Does not look too rosy, to be honest.

1 Like

The buyback topic raises a question. When the wheel of fortune turns and a company becomes a bit less profitable, it can do a capital increase (or capital hike), with a strong incentive for existing shareholders to give fresh money to the company. How does it work in practice when the shares are owned by an ETF?

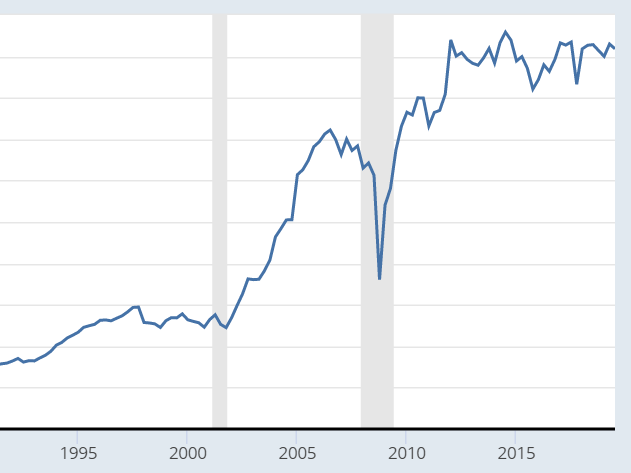

The graphic suggests that 1987-today was overpriced, yet the returns were fabulous.

Well to be precise they were fabulous in 90s and 2010s but not in 2000s. But frankly speaking I doubt in predicting power of CAPE. Last decade was very good and CAPE was very high. Maybe this anomaly will end in some gigantic crash (bubble of all bubbles), or maybe it’s the new normal (due to ETFs pumping the indices). God knows and time will tell. In the meantime I continue investing and in the future I plan to diversify the risk into other asset classes (like real estate).

1 Like

IMHO it has to do with the extreme reactivity of central banks to any slight downturn in the stock market, during that period.

1 Like

Perhaps, but this reactivity won’t change anytime soon. Near zero interest rates and new monetary policy tools are to stay with us. De iure FED’s role is to keep inflation in check while keeping low unemployment, de facto it’s new role is to keep the stock market up. So, it seems that the stocks growth with high CAPE is the new normal. We can continue investing.

A P/E of 25 implies a return of 4%. Quite poor. It reminds me of of the times when a flat in Poland had a rental yield of 8%, but in Switzerland only 4%. Low interest rates and cheap loans inflate the prices and kill the rate of return. I guess in Switzerland it only makes sense to own a flat for rent if you are leveraged with a mortgage. They can’t pump stock prices ad infinitum if the earnings don’t keep up. It’s really not sustainable.

No they can’t. That’s why you have crashes from time to time. The whole problem is with predicting those.

What they can do is to buy stocks directly.

I just say “all is good”.

BOJ is already doing this for years. I think other central banks will follow once they run out of ammo during next crash. This will be the new norm. Another monetary policy tool.

1 Like