Now what appears even more shocking to me: ETF returns in CHF seem to severely outperform 3a fund returns in CHF.

How can this be?

Sources: justetf.com for ETFs, swissfunddata.ch for 3a funds.

Now what appears even more shocking to me: ETF returns in CHF seem to severely outperform 3a fund returns in CHF.

How can this be?

Sources: justetf.com for ETFs, swissfunddata.ch for 3a funds.

They accept 2nd pillar pledges, why wouldn’t they accept an external 3a pledge?

A vested benefits account pledge (which I believe you are referring to - paging @Cortana as that is the only such case I have read about ) is equivalent to the pension fund pledge. Not really a money maker for the bank giving you the mortgage.

But I have never heard or read about an external 3a being accepted as either down payment pledge or for indirect amortisation by any bank. If this is possible indeed, I would love to know more about the providers accepting such a setup.

I’m thinking about just using Swisscanto funds. Then I don’t have to worry about what will happen with UBS/CS funds next year.

Different countries (FTSE) and higher inclusion of small caps (both ETF).

Same thinking here… its sad that there is no news from UBS on the CS Index Fund offering. They were the best but looks like they let it die…

Any reason to believe this? Could they simply not rebrand them?

Damn it I just saw that my vested benefits account has this exCS fund. 1.61% redemption spread, wtf. Why is Finpension using such scammy funds?

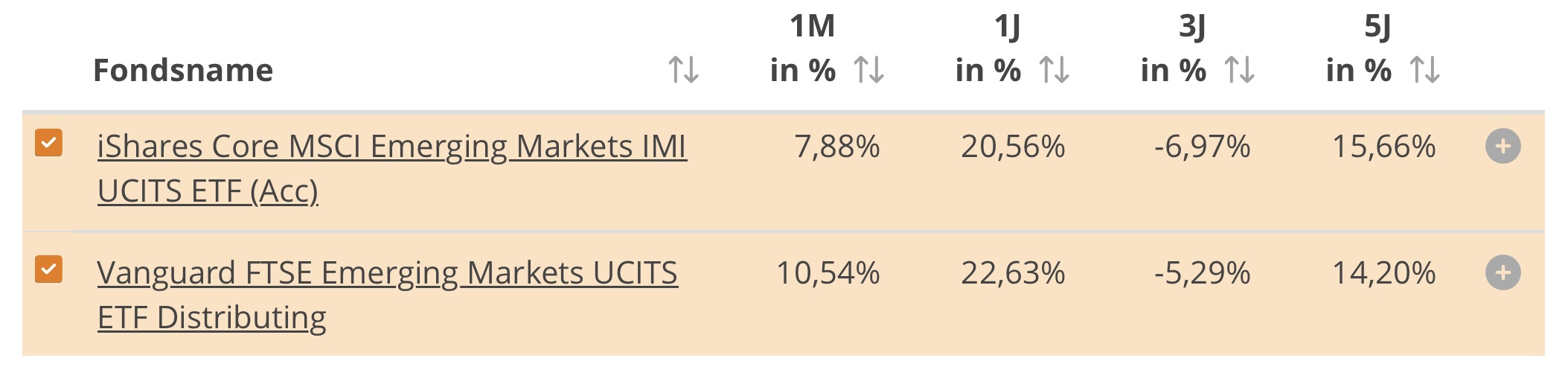

@Compounding have you compared the performance to a CHF-ETF or fund on MSCI EM (no IMI), just to exclude that possibility?

Still weird, there can’t ca be such a big difference between IMI or not, or between MSCI and FTSE.

Could it be that the online tools include some possible fees of the funds, which are actually waved on your 3a version of the fund?

Or simply has bad data or time periods for the funds?

Yeah, I don’t understand either. If this fund performed 1.6% better than its competitors, I wouldn’t have an issue, but this does not seem to be the case. So the India-WHT issue can’t be the problem, because other EM funds hold India too. Also, it’s worrying to me that this spread keeps growing silently.

Valid points, I have compared to some ETFs, and they all have performed better. The advantage is smaller for EM ETFs without small caps, but still significant imo. So Truewealth’s argument about index funds in 3a not always being the best choice seems correct.

And among 3a index funds for EM, the difference between UBS & exCS vs. Swisscanto seems inexplicably big. Makes me wonder if that’s the case for other funds too.

On the fund data: Sure, since I unfortunately don’t have access to a Bloomberg terminal or other non-open data sources, there might always be flaws. But I’m not sure how these could be that significant. I did check for fund fees.

I think we should not get hung up on this number. Because this number varies and changes based on what’s the expected capital gains tax in India that the fund needs to pay when any member redeem their units. So rather than putting it in the NAV, the fund puts it in the redemption spread.

Remember this number is going to be different depending on when the fund started, when the contributions were made, and how much Indian stock market grow over time etc. A fund which is operating for long term, the capital gains tax have also accrued over time. If suddenly there is a 20% crash in India, I think redemption spread would also change.

You put it on NAV or redemption spread is a matter of principle but as long as these numbers get adjusted over time, it cannot be detrimental to investors.

However I have to say , for me personally having NAV adjusted is much better because it gives clear idea of what you are buying into.

BUT - If you think about it carefully, 3a. 1e or VB etc are not meant for buying in and going out every year. If you believe that redemption spread is unfair; If the redeeming members are charged a spread then the remaining members by default get benefit of that. Isn’t it?

And with continuous influx of money coming in, the need to redeem (for rebalancing purposes) would also be low.

For all practical purposes, there is not going to be much difference in large funds who buy MSCI EM companies other than the TER costs. NAV + redemption would take care of each other.

If CS fund was bad, no one will invest in Credit suisse fund. So please let’s give some credit to people who built this fund, buy this fund etc

If that showed in the total returns of the fund, I’d be fine with it. But as is, performance seems comparatively weak, and you get the spread on top of that.

So, with all due respect, whatever exCS has been doing with this spread mechanism, I’m really not into it. It’s nothing personal, just business. I’m quite sure they wouldn’t hesitate to squeeze any Rappen possible out of me either ![]()

I am not defending CS. I just feel the mechanism might not be how we think.

It could be the redemption spread is charged differently to different units depending on when they were bought and redeemed.

That would be a more fair system perhaps, but someone here mentioned that this is unrealistic, because it would be an administrative nightmare for them to manage that

I agree it’s all fairly intransparent, and that’s another issue I have with them

You do realize that CS doesn’t earn a single cent on the redemption spread? The spread is credited to the fund, and is there to not dilute the shares of existing investors due to trading costs, capital gains taxes, etc.

And Swisscanto, UBS and the others are more transparent about how they handle indian capital gains taxes? I don’t think so.

ExCS tried all the options there are for handling indian capital gains taxes. Initially they provisioned it in the NAV, then they billed the realized indian capital gains taxes directly to the redeeming investors and now they increased the redemption spread.

Other funds seem not to be influenced; e.g. the big blue pension one. Redemption spread of 0.01%. Same for other funds.

Why the EM especially has a high spread, I dl not know.

Yes, but that’s not the point. The point is that this fund has had poorer performance than other funds, and the spread on top of it. You might want to take a look at my comparison of index funds and ETFs above.

I’d appreciate if someone could help with hard numbers - either confirming or disproving my simple comparison above. And believe me, I’d be happy to be proven wrong.

Exactly, that’s the issue.

you used the wrong UBS/CS Find. Please use CH0017844686. It is currently not listed in Swissfunddata.

When you compare performance based on Fund Factsheets, you see that the CS Fund performed better than the Swisscanto one.

Overall, the situation is that CS by far was the best fund house for Swiss Index funds. But the question truly is how that will continue. The lack of transparency and communication, the fact that UBS was a terrible Index fund manager and the tendency that UBS just swallows CS culture and knowledge… makes me a bit sceptical. Overall, I mainly sit on the fence but with regard to EM Index Funds, I have already switched to Swisscanto.

Thanks for double-checking, data for UBS 5y returns (CH0252809717) seem wrong on Swissfunddata.

I checked all funds on www.finanzen.ch again for 5y returns in CHF:

Swisscanto (CH0117044971): 8.89% -0.23% spread= 8.66%

UBS (CH0252809717): 7.91% -0.21% spread= 7.7%

exCS/UBS (CH0017844686): 9.11%-1.61% spread= 7.5%

EM ETF EIMI (Truewealth 3a): 15.73% (including small caps)

EM ETF based on same index as 3a index funds (Swisscanto etc.): 10.88% (XTrackers EM ETF)

Difference Swisscanto vs. exCS: 1.16%. Not that dramatic in the end, but still quite a lag.

All index funds underperform when compared to EM ETFs: So my crude first conclusion:

Truewealth EM ETF > Swisscanto EM > exCS EM

Happy to be corrected, as I’m restricted to maybe unreliable free fund information.

The numbers I see are following.

| Total Return performance in CHF | ||||||||

|---|---|---|---|---|---|---|---|---|

| Source UBS Quotes for funds , justETF for ETF, Performance until 30.09.2024 as of different starting points | ||||||||

| from Nov 2014 | from Jan 2015 | from Jan 2016 | from Jan 2017 | from Jan 2018 | from Jan 2019 | from Jan 2020 | from Jan 2021 | |

| UBS | 28.24% | 34.94% | 57.09% | 38.89% | 5.23% | 21.47% | 4.30% | -3.57% |

| SWC | 26.86% | 33.92% | 57.15% | 39.12% | 5.80% | 22.33% | 5.12% | -2.71% |

| EX-CS | 27.73% | 34.40% | 57.16% | 39.15% | 5.75% | 22.40% | 5.47% | -2.52% |

| IEEM ETF | 23.42% | 27.32% | 49.72% | 32.34% | 1.28% | 18.25% | 2.30% | -4.64% |

These are excluding redemption spreads.

Note -: EIMI ETF is not a good comparison because it includes Small caps & at least in India Small caps have completely dominated the returns for last few years. Thus I used the ETF tracking MSCI EM index which is used in all the 3a funds

As we can see the ETF is the worst option of all. Not the best ![]()

We should always look at total return (TR) numbers.