We’ve extensively compared fees among 3a providers, but what could be equally interesting than fund fees is fund performance: How do CSIF, UBS and Swisscanto compare to simple ETFs? Has anyone looked into this? Anyone know of online resources that have info on all these funds and can compare the performance currency-adjusted (CHF vs. USD)?

Of course, performance comparison only makes sense if we compare funds following the same indexes (eg MSCI)

For example, I have noticed an epic tracking error for CSIF EM Blue of 0.87 since inception.

Example: Truewealth has a nice ETF for Emerging Markets at 0.18% TER: iShares EIMI, IE00BKM4GZ66 (USD). Finpension offers CSIF, UBS, and Swisscanto EM funds (CHF), charges you 0.39% all-in. WHT should not matter for EM, correct?

Now looking at performance: Is there a way to compare the performance of the aforementioned iShares EM ETF (USD) to the 3a funds? I’m aware, EIMI tracks MSCI EM IMI index vs MSCI EM index for the rest, but difference should be marginal

Actually FP generally have very low TER funds in their offering for 3a. So yes 0.39% includes everything

For Truewealth- it appears they don’t charge anything on top of TERs. But yes the TER cost is important in that case

For emerging markets -: I think it doesn’t matter if you have ETFs or funds, they would all have similar issues of Indian capital gains tax and hence would be tough for them to track their benchmark indices. If you look specifically for India exposure, you can clearly see this for ishares NDIA or Franklin FLXI where both cannot match their benchmarks. In simple words, there is no way for any ETF/fund to match their benchmark for Indian exposure because of the assumption of capital gains tax (short term and long term)

To compare fund performance , I think best way is to use UBS quotes (if you have UBS account) and you can add multiple funds for comparison. They have all funds in general. In reality 3a fund is still a fund

P.S -: I tried to look into the Indian ETF matter in detail because I wanted to decide which ETF to buy. It looks like the portfolio turnover drives a lot the final performance due to capital gains in bull market. In bear markets this can change

Thanks, that’s helpful! Unfortunately not a UBS customer, any other idea how to best compare fund performance with the possibility to adjust for currency (USD vs. CHF)? Maybe IBKR?

The measure of performance that matters to me for passive ETFs is how good the fund managers are at tracking their benchmark index so, for comparison between funds tracking the same index, I’d use tracking difference as my metric.

The fund litterature and https://www.trackingdifferences.com can help. Unfortunately, local pension funds are less analyzed than global widely available ones and their metrics are harder to find in a fully comparable form (using the same methodology).

For the choice of the indexes I want tracked in my portfolio, I’d rely on fundamentals (methodology, including country coverage). Past performance isn’t a factor that enters my reflection, what enters it are if the conditions to nurture good future performance are met or if I’m doubtful that they are.

→ Total cost of holding CSIF EM with Finpension: 0.53% (0.39+0.14), and then 1.24% Rücknahmespread at redemption

→ Total cost of holdin iShares EM with Truewealth: 0.24% (0.18+0.06) (no Rücknahmespread, but 0.075% stamp duty and 0.1% FX markup at purchase)

→ OMG

Not a big fan of the iShares EM, much more so of the iShares EM IMI.

Also, imo, tracking difference remains a good measure of performance even when comparing funds based on different indexes. Of course, you’re not looking at absolute performance, but at performance relative to index.

So iShares EM IMI, containing much more EM stocks than CSIF EM, and less tracking diff., is the clear winner to me

(Ok, I shouldn’t even mention VIAC here due to their exorbitant currency conversion fees)

Now if @True_Wealth finally were to introduce some regular MSCI or FTSE all world funds used literally everywhere else in the investing world, they could easily blow away the Viacs & Finpensions. Pitty they stubbornly keep to their weird regional peacemeal ETFs.

Also, it’s data from chatgpt (best i got to work with, unfortunately), so use with great caution. initally it was unable to identify the right funds despite the isin provided…

I’m sure someone who has more precise tools at hand could perform more precise comparisons.

All I’m trying to figure out is whether UBS, CSIF and Swisscanto can really compete with simple iShares and Vanguard ETFs, especially accounting for tracking error.

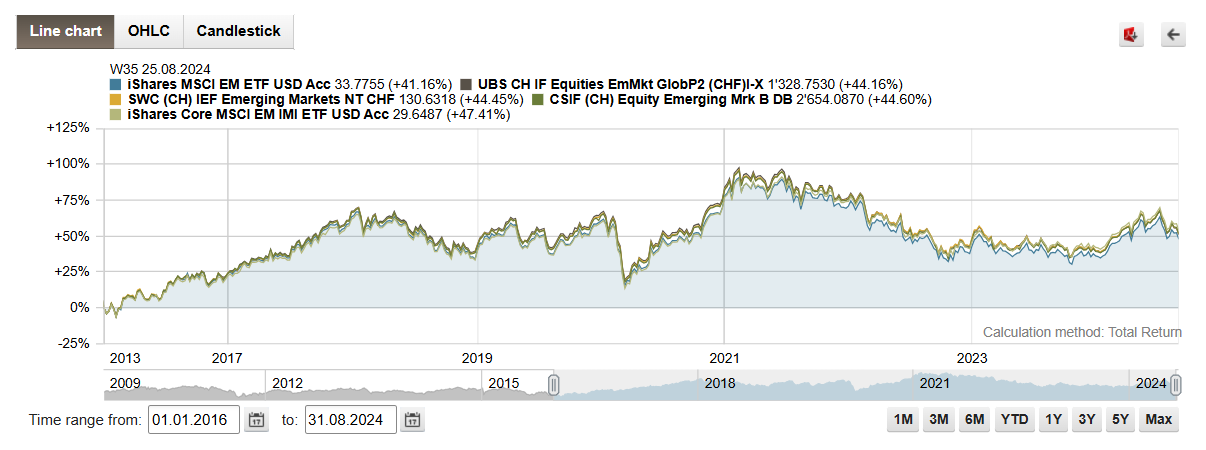

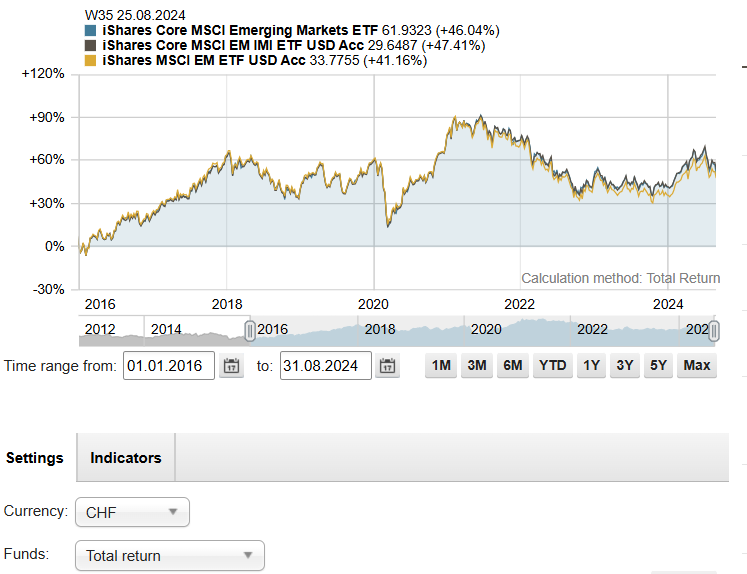

If we do a like to like comparison, Finpension offerings (CS, UBS or SWC) has outperformed ishares MSCI EM ETF. This is illustrated in post. In other words if FP offered ishares ETF IE00B4L5YC18 (41.16%) , then it would have underperformed the current option of CH domiciled funds (44.6%).

The difference in historical performance you are quoting is not because of use of CH domiciled funds vs. ishares ETF. It is due to underlying stocks. MSCI EM IMI (IE00BKM4GZ66), 47.4% has outperformed MSCI EM IE00B4L5YC18 , 41.16% over the period we downloaded the data most likely because small caps stocks in EM outperformed large caps. But this does not always mean that this would continue in future. This has nothing to do with ETF vs fund, it is simply the conviction on small caps vs. large caps.

Hence if investor seeks to invest in MSCI EM IMI via 3a, then only choice would be Truewealth. But the same outcome can be achieved by continuing to use FP and invest a small amount in MSCI EM Small caps in IBKR.

P.S -: I understand that CS funds have this high redemption fee, but I cannot confirm if this is good or bad for current fund holders vs UBS fund which provisions already in NAV. In general I tend to not over-optimize 3a offerings from Finpension. I just use the standard Global 60 or Global 80.

Another point to think about is that even though factsheet of Credit suisse Fund has redemption fees, it could very well be possible that this fees is not really charged to investor. This would depend who many redemption and purchases are made on the day of redemption at Finpension. I doubt that FP will sell these units unless there is a net outflow on the day of redemption

I would rather assume that you have been lured into it with the promise of a lower interest rate, and you might have not understood the full extend of this decision. (of course we can discuss transparency)

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.