Total Cash outflows takes into account column C (“Amortization paid”) which is the trickiest one. This column is constant and equal to cell B14, which computes how much you need to pay every year to both repay the capital borrowed (say the 15% amortization), AND the interest on this capital, this over a fixed period of N years (here 15 years). I can provide further calculation if needed.

So actually the total cash outflows do take into account the interest of both parts of the mortgage!

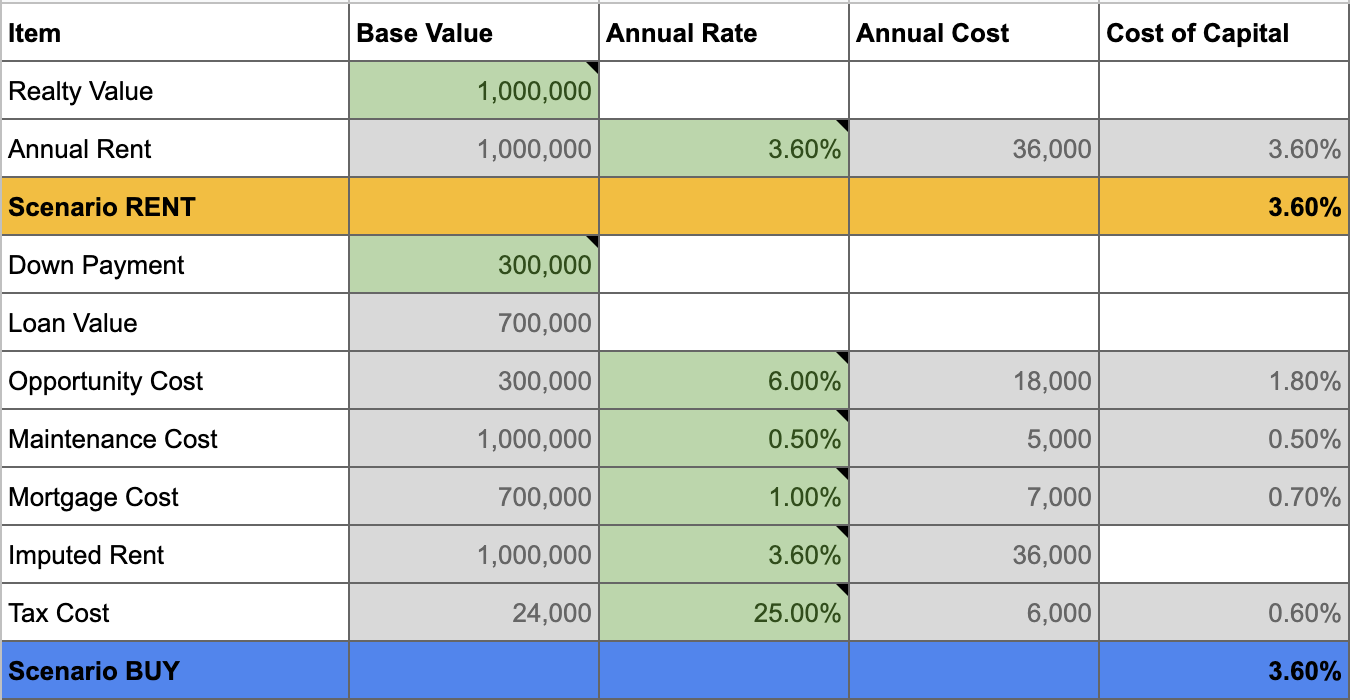

Well for sure if the rent was 3’000 CHF per month, then it is easier to find opportunities where you may be better off buying, even with 3% interest rate on your mortgage. Especially so if, as you say, you are not required to pay any amortization…

Those are all very valid points, especially the maintenance one. Regarding interest rates, I have no idea when they will be in 20 years, but indeed 3.5% is not farfetched. They might go into negative territory as well (as Denmark currently does… the guys are paid to borrow money for their house, crazy). And the capital gain tax makes things even worse indeed.

All i wanted to do is to provide the tools so than people can do their own simulation, so the thread does not goes in circle.

I agree with you though, buying in Zürich in the current market conditions is very unattractive.

It depends on your parameters. Usually in the very long term (25+ years), the stocks compounded returns takes over the leverage of the house if real estate does grow too much (<=2%).

In the short term, it all depends of your cash flows. The leverage on the house plays a big effect as well since you are leveraged x5 and it magnifies the real estate growth (a 2% becomes a 10% minus borrowing costs). But this effect will be less strong in the long term: as the value of the house grows, the proportion of liabilities compared to the house value becomes less and less, and your leverage diminishes.

These prices are for sure on the lower end of Zürich City. I live in a 65 sqm apartment in Leimbach, on the 16th floor of a Baugenossenschaft. While it is still technically Zürich City, 50 meters further and you are in Adliswil. But the connections to Hauptbahnof are very good, and this is the view on the Glarner Alps I had from my balcony early this morning… So the price is cheap-ish, but i really like it.