The only thing that’s a bit unclear to me is the 1.5% yearly costs. It’s an estimate and I’ve asked to some friends of mine and they said that 1.5% is too high. They spend less. None of them had to rebuild part of the house though. Like the roof. But maybe for such big expenses can intervene an insurance, if it’s due to some damage (storms?)

Well 1.5% seems high if you own the property for less than 10 years or if it’s rather new. But after 30-40 years? Insurances won’t cover wear and tear of the roof, only partially destroyed parts due to a storm. Swiss banks usually suggest 1%/year and 0.7%/year if it’s not older than 10 years.

It’s not only about replacing damaged parts but also keeping the standard. You’ll probably want new bath rooms and a completely new kitchen after 20 years.

2 Likes

I’d be cool to know the costs for all that. I have no idea.

On 1Mil house you have 15k chf x 30 years = 450000 chf.

How much does it cost to remake a roof?

https://www.energieheld.ch/daemmung/dach/kosten

Maybe someone else has already calculated the possible costs involved.

1 Like

I guess it really depends what you want. Are you satisfied with a 10k IKEA kitchen or do you want to spend 50k on something pretty decent? What about windows? Velux or something cheap?

Renovating bath rooms, the kitchen, the floor, walls and a couple of other things will be 150-200k easily.

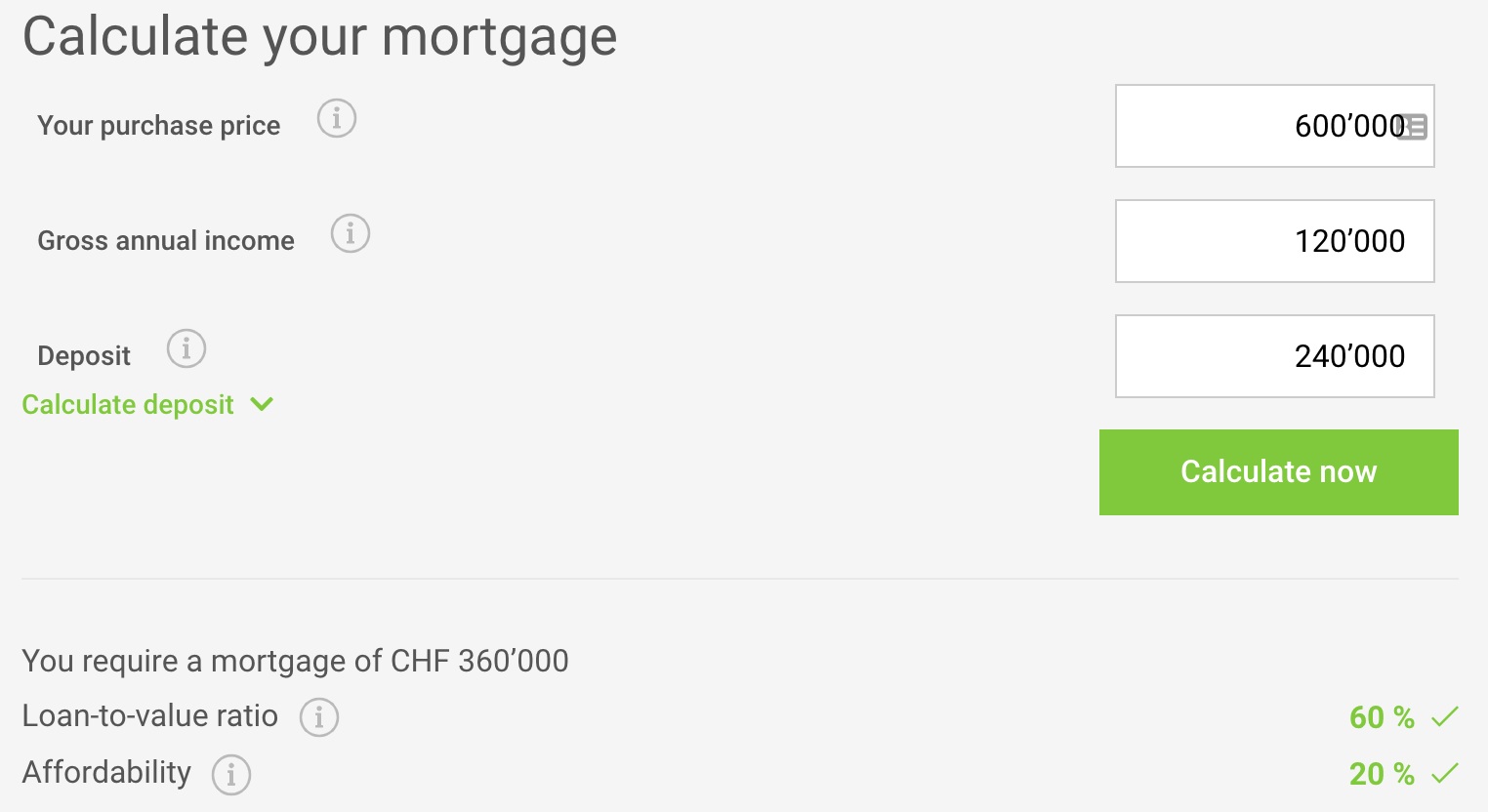

I like how Comparis puts it. So for example, for the following sample input:

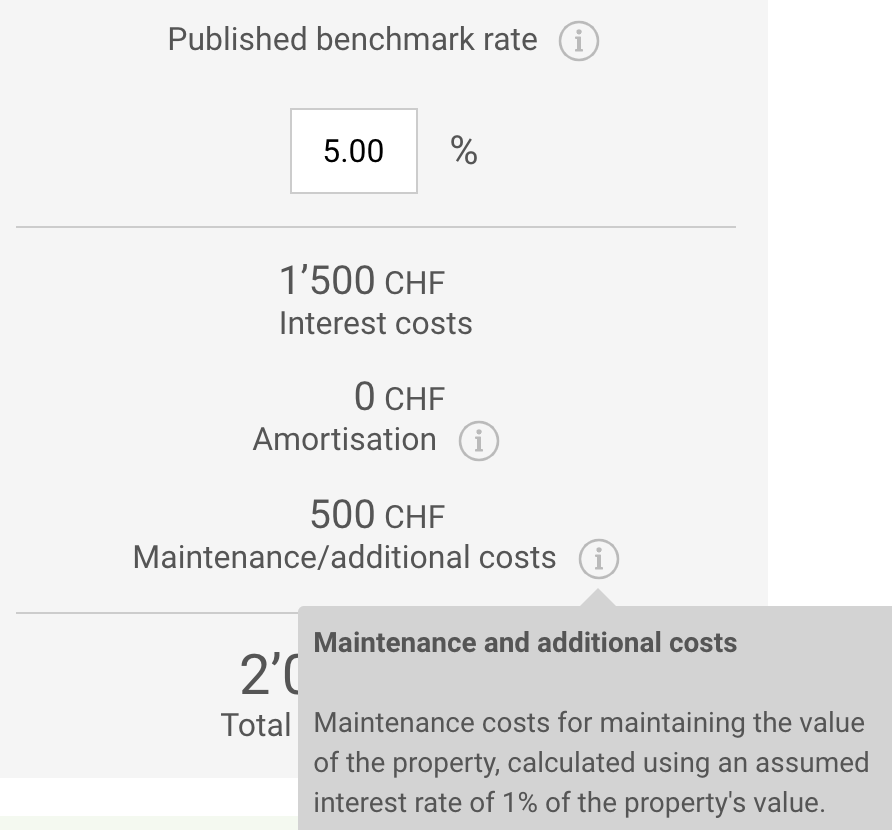

…your affordability (Tragbarkeit) would be 20%. They derive it by dividing interest cost (5% of 360’000), amortisation and maintenance (1% of 600’000) by your income (120’000).

The way they define maintenance (maintain the value) could be also understood as fighting depreciation. That means, it’s not only about keeping the flat usable, but also pricing in that the tastes of people change, and your sexy new flat might not be seen as attractive in 30 years as it is today, unless you renovate it thoroughly, including the exterior.

Most owners scoff at 1% annual cost, but most of them haven’t owned it for 30 years.

4 Likes

I don’t understand why people keep saying this. The fact that you can deduct interest payment from the taxes only means in practice that you get a discount on the interests you pay, but you still pay those interests to the bank! As others have said, is normally better to be paying money to the state than to the banks!

Now, if you don’t want to lock up too much of your net worth in a single property and want to invest the money somewhere else instead to get higher returns, that’s a valuable, but different discussion, and doing so actually means using leverage. But saying that “paying it down makes zero sense in Switzerland” is just misleading and I am amazed how the average person in CH blindly believes this to be true.

4 Likes

Not if you are a frugal mustachian, I guess ![]()

1 Like

Thank you @Cortana, I am not particularly strong in Deutsch so it took me a while ![]() , but yes, very informative, danke viel mal!

, but yes, very informative, danke viel mal!

2 Likes

Just checked the Tagesanzeiger article. What I don’t get is that the renter has to pay 3000 CHF (holy crap, buying at Crédit Suisse or what) for transaction whereas the Homebuyer nothing. But we should all know that buying a home is super expensive.

I would add that buying a home for yourself is actually mostly a consumer product rather than an Investment (if you live yourself in it, renting it out is another story IMO).

For myself I figured out with the 4% rule I should take my rent times 25 (actually more like x20 to account for maintenance cost). A home should be not more expensive that value X (right now about 500’000 CHF). Above that, homeownership is a bad deal since you would need more capital than actually renting. Below, it would be on the other hand a good deal. And actually

However what Cortana avices to keep the mortgage going to invest on the other hand can be done against, but I would advice against it, since it is actually nothing else than leveraging your Investment. However I would like to say it is better for the peace of mind and financial security not to do that. I mean everyone is advising to not invest money which you actually do not own…

Cheers

3 Likes

But you’re still doing it by investing in real estate. You are highly leveraged at the beginning.

To me it seems like a nobrainer. Why pay back the mortgage that will save me 0.8% on interest if I could invest that money with a much higher expected return?

What happens if you can’t work anymore because of illness or something similar. Than suddenly you are there with a big mortgage you have to pay for and have to sell invested capital at loss (as well as the house since suddenly you need money urgently).

As said, I do not consider a house an Investment. It is just a thing I use and have to maintain to - hopefully - maintain it’s value.

My idea is more paying for a house cash, at least at a much higher amount than the min. 20% downpayment.

Somehow I have the feeling that since it is expensive, a house is regarded as an Investment. But for me it is just a dead thing. Does not produce anything, has a high volatility, low liquidity etc. IMO, a house is a consumer object, and that’s it. A rise in house price is actually mostly inflation, since the house next door will also rise in price. Only if you are ready to relocalise to another region you might find something cheaper

5 Likes

Nice discussion guys, and I would add one thing.

That is, we all need a place to live. And unless we’ve got access to free housing, we’re all short housing.

Buying a house should be considered just like any other investment: by the cash flows it generates. So @Patirou: I respectfully disagree.

Say you expect to live in this house for 10 years.

With a leveraged investment such as a house mortgage, you access the full value of use (which can be valued as the expected rent you would have spent for similar service over the next 10 years. I don’t want to split hairs, but don’t necessarily think about the rent you’re currently paying, think about the rent you’ll pay once living with someone, needing a larger place for a starting family etc. But that’s a detail.

But back to the value of the house investment. The discounted cash-flow generated by the house can be valued as the present value of the future rents you won’t have to pay, now that you’re a homeowner, as well as the costs of owning (interest, owning costs, taxes, tax savings). The calculation is anything but trivial.

This calculation need to be benchmarked against the expected return on your alternative form of investment. Since we’re Mustachians, let’s call it VT.

If you expect VT to return 3% p.a. with 0% volatility (let’s make it simple), you compare

- present value of : that 3% annual return of the money you’d invest if you hadn’t a mortgage, minus expected rent

- with the present value of: annual cost of owning the house (1.5% of house price) + annual mortgage cost (1.35%) + resale profit (if any)

Example: if you expect to pay 2000 in rent and make consistent 3% return in VT, 1.37% interest rate for 25y, 4.2% notary and 20% downpayment, 1.35% owning costs, resale in 10 years and 0% appreciation of the house (= depreciation in real terms), and you ignore the value of flexibility provided by renting and the security of a liquid asset, then you are better off buying up to 640 kchf. That’s the right amount of house you need. Beyond that, better invest in VT.

I wouldn’t rely on a rule of thumb that is too simple,… it’s a complicated calculation. I think Excel is better suited for this kind of problem. There also are personal considerations (security, psychology) which are not irrelevant.

2 Likes

We’re also short food then, it doesn’t mean I should buy a farm ![]()

3 Likes

An other advantage of keeping a mortgage on the house is that you deduct its value from your wealth and as a result reduce your wealth tax. If you pay your house entirely, then it increases your wealth. From a purely mathematical point of view you better have the most part of your wealth on assets producing income. A house in a nice thing to have (I made the choice to buy) but it does not produce income when it is not for renting.

I’d rather keep my diet flexible and infinitely more varied than what my poor two hands could produce on a farm. But it’s all down to your personal preference. Nice analogy ![]()

But again: calculate the cash flow of owning a farm and make a case for which is superior. We’re not here to discuss diet preferences.

1 Like

Well if you reimbourse your mortgage you have less cash/other assets, so in fact there is no impact on your net wealth and wealth tax.

I have probably stupid question, but quite important to properly understand financial implications of buying a home. E.g. using UBS mortgage calculator with following (example) parameters:

Purchase price: 1 mCHF

Gross annual income: 200 kCHF

Equity: 200 kCHF

I got:

Interest: CHF 800

Amortization: CHF 741

Maintenance and ancillary costs: CHF 833

Monthly costs: CHF 2’374

Are those numbers solely for affordability calculation or one has really to expect the “Maintenance and ancillary costs” of 833 CHF per month for such property? Am I right that in case we assume this is new construction and we want to sell in 10 years (which means we probably don’t need to put aside any money for renovation works etc.), our TCO will be only Amortization + Interest plus of course yearly insurance and some house taxes?

1 Like

Even if it is new, there will always be some maintenance cost. Of course, it will probably be less than 1% a year in this case.

1 Like

Amortization isn’t really a cost, because it goes into your own pocket.

4 Likes

Hi Bonanza,

thank you for your answer which is thought through. Of course that roule of thumb I gave is super simple and is for me just a first approach while figuring stuff out. If you want, it is like a first screnning tool. If it is close enough on the bad side, I would look at it closer. Don’t get me wrong, I am also looking to buy in a few years, but I see clearly a house as a lifestyle choice rather than an Investment.

I would like to give another example : you could buy a car or longterm rent a car (up to 5y in General) of any type. You would free up cashflow by buying the car, but still you would not look at the car as an Investment. Still with having the car, you would have access to it, also if you take a loan (which I would not recommend to do, and I guess a bunch of other as well).

As you said, we all need a place to live. So when you sell your house and want something equivalent, your resell gains is actually taken away from the higher buy value of the new house. Except if you manage to get a good deals on both sides (means sell higher than market value and buy lower than market value). Another way is to make betterment works on your home and then sell it for higher than the actual works (this I would call an Investment, not actually the home)

What is bothering me is noone would invest into stocks with leverage as a private person (except some super Risk-liking person) as we are all aware of the risks when job loss happens etc. Somehow we hide this risk (the bank actually does not, if you take too low downpayment, bank might be asking for insurances like cosigner or insurances to pay extra for unforeseen events). And a house is a high volatility, low liquidity asset.

Thing is, accidents can happen, and in this case either I would like to have the capital ready to sustain a rent, or a paid off house.

The wole thing about tax saving is kind of a smoke screen : Either Wealth tax on your house or on your liquid capital = same stuff. Deducting interest payment off your income : you pay interest to get maybe 30% back of that ? Not a good calculation in my eyes. Still there is the Eigenmietwert = you also pay tax on the dividents.

Sure, not a good Excel calculation, but I would not be surprised if this is kind of a zero-Zero game.

The only Advantage is you can invest money into stocks which you actually don’t own = higher risk

EDIT: right now I pay 1660 CHF in Winterthur, including outside parking (fuck me is it expensive in CH, good I don’t have a Company car with all Costs covered otherwise), for a 3 room appartment in Winterthur area.I guess it is rather good Price. Of course Nothing luxurious, but it does the trick and allows some Family growth. (Living with my wife at the moment).

BTW Looking for some constructible land to put a somewhat Tiny house on it (not on wheels, but something efficient and adaptable), which allows me to go for more land and other freedoms, like working less.