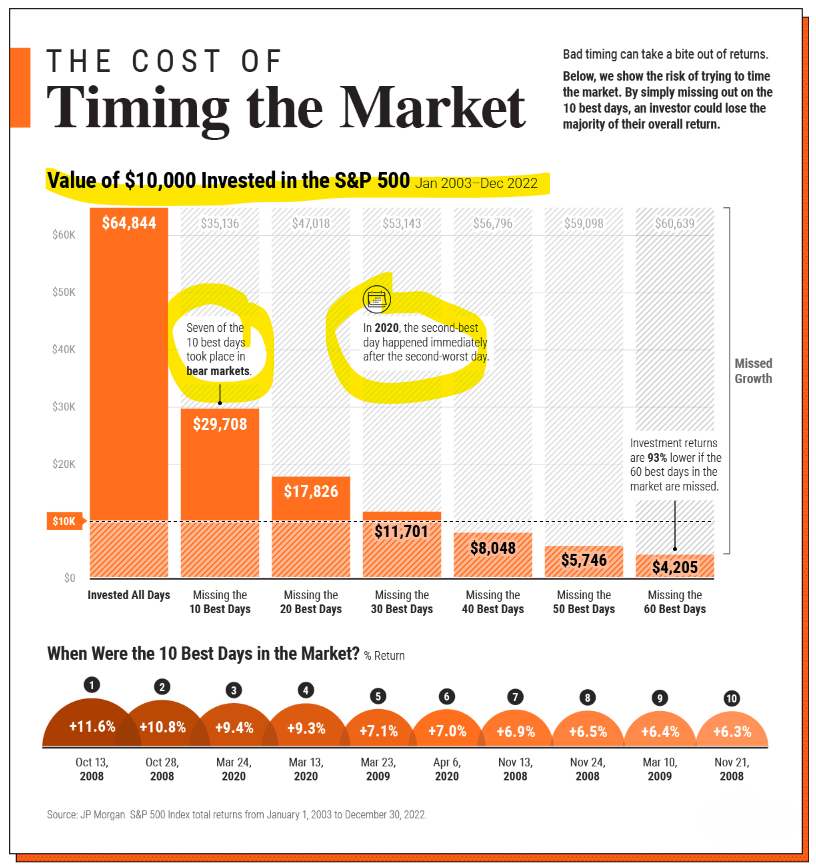

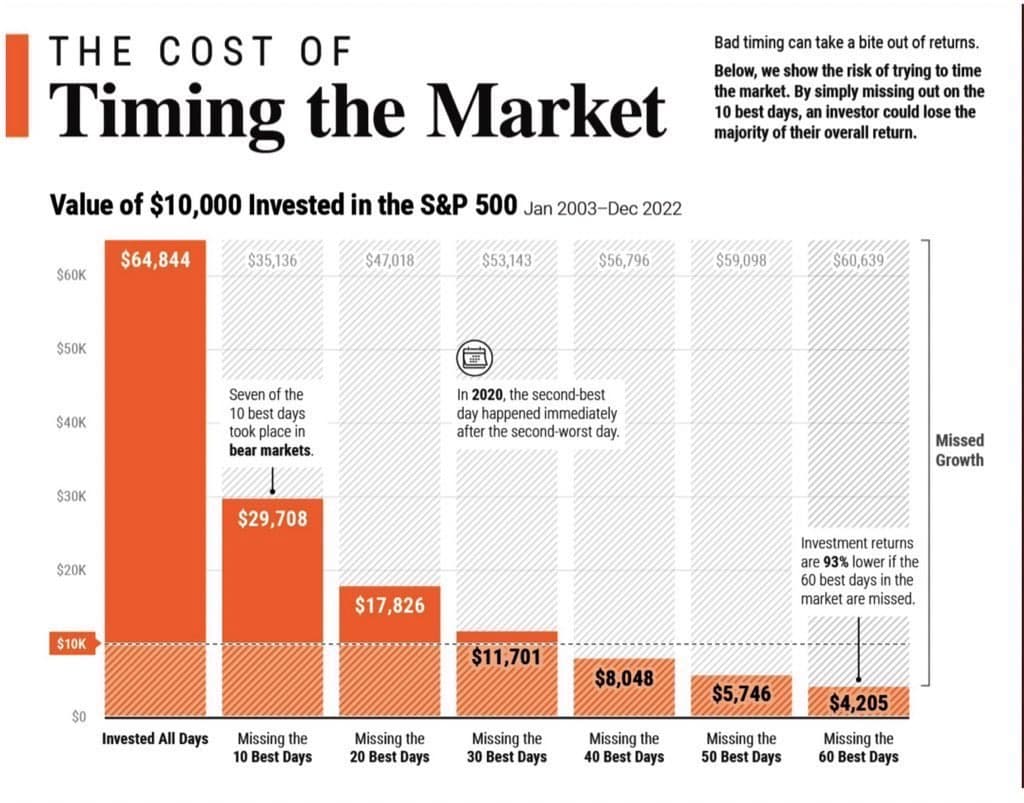

I think you are talking about this chart.

10 best days in history were very high moves. Some of them almost 9-10%. If you miss 10 of them then returns would be reduced drastically

But this calculation is not about investing at different point of times. It’s referring to folks who pull the capital out when market is shaky and try to time the move back in. The calculations are about lump sum investments.

Regarding your question -; let’s say you invest on Monday and post that market only goes up , then you will have a -2% versus someone who invested today. Over time such things do add up if investor keeps moving in & out.

I am one of those awful market timers. But I don’t even start to look at timing before the SP500 is at less than 80% of its last high. It is actually at 91.73% with a low of 89.54% reached yesterday.

I call my market timing “crash recovery plan”. It is based entirely on credit because I will never ever be invested less than 100%… cash is trash and probably the only investment with a state guarantee to lose value.

Made quiet some money the last 3 bear markets, even my timing was very bad the last time. That was a lot of suffering but then also a lot of money.

I like this forum, so I will publish next time I start my crash recovery plan. But we are far away from that as I (and most of the world) only declare a bear market when the SP500 is under 80% of its last high.

Pretty crazy the S&P500 did 22% in 15 days in 2008. In reality it’s irrelevant to any long-term investor who doesn’t sell when red (why would anyone do that unless they can’t keep the lights on otherwise).

People sell when markets go down because it feels like there is no end & everything will collapse. Specially the folks who have 100% equity allocation because volatility is not everyone`s cup of tea.

But yeah, if someone doesn’t sell for 20 years, they wouldnt get impacted by such moves.

I notice that I’m less serene with the current market than I was in 2022 with the war between Russia and Ukraine. One of the reasons is probably that in 2022 I couldn’t invest (no money to spare every month). Whereas right now I’m sticking to my plan of investing every month according to my allocation between VT and SLICHA. But I’m thinking about the choices I’ve made with my VIAC strategy, wondering if I shouldn’t simply go back to the Global 100 strategy rather than my personal strategy (70% world / 30% SPI).

And then, on the other hand, I say to myself: whatever happens, in reality, you’re buying a cheaper position right now, so it’s all for the good in the long term.

I think it’s a good experience to challenge my nerves and stay focused on my strategy: investing every month without listening to the market, rumors and so on.

All in all, I laugh a little at what Trump and Elon are doing… But especially the MAGA who don’t understand much and drink their idol’s words like a god.

Getting back in the market at the right timing is really hard.

During Covid crisis on March 20th, we were at -33% and based on the news flow, I was expecting to go worse in the next few months so I was holing my horses. I invested only 10% of what I could have unblock.

But the market went back up so quickly that I didn’t have time to bought more VT.

I was expecting a slow plunge and slow recovery like in 2008-2009.

For next bear market, I’ll apply similar ranges -20%, -30%, -40% to unleash bond/cash allocations and take short term debt at a local bank. At Credit Agricole, you could have a mortgage of 50k euros for 5 years without justification.

I’ve never took margin on IBKR. Is there any procedure to do in anticipation to be more reactive ? what will be a risky but kind of safe margin oyour VT position in a bear market ? 10% ?

I believe that making a plan and bands/rebalancing targets takes away the guesswork/luck.

My own targets are -10/20/30% of the ATH for dropping 30/30/40% of any liquidity, if it goes lower (which is actually pretty rare) then so be it.

The priority to be honest is not selling a single share at a downturn, then the larger the portfolio gets the less meaningful any buying the dip becomes.

Personally my threshold is a portfolio of 250k, holding 25k of liquidity begins being silly (for me), meaning when my portfolio crosses 250k I won’t be bothering stressing about any dip buying, just buying regularly.

Two simple points to help you get a better night’s sleep:

Delete all trading applications on your PC or smartphone. Only use the WebUI to trade once a month. If you are investing for the long term, there is no need to look at the numbers at all (with a set and forget strategy like VT/VWRL/WEBG etc).

Only read credible news sources (or only your local news paper if you want to be really restrictive)

Just to make it clear, you are out of the stock market - holding cash (or something similar) - till the market drops 10/20/30%?

How do you decide when to stop investing? Too many years of high returns? Valuations?

The message is clear and super useful, but the concept is a little bit misleading

Missing 10-60 best days without missing a single of the 10-60 worst days of the same period? I think the chances for these scenarios to happen are practically zero.

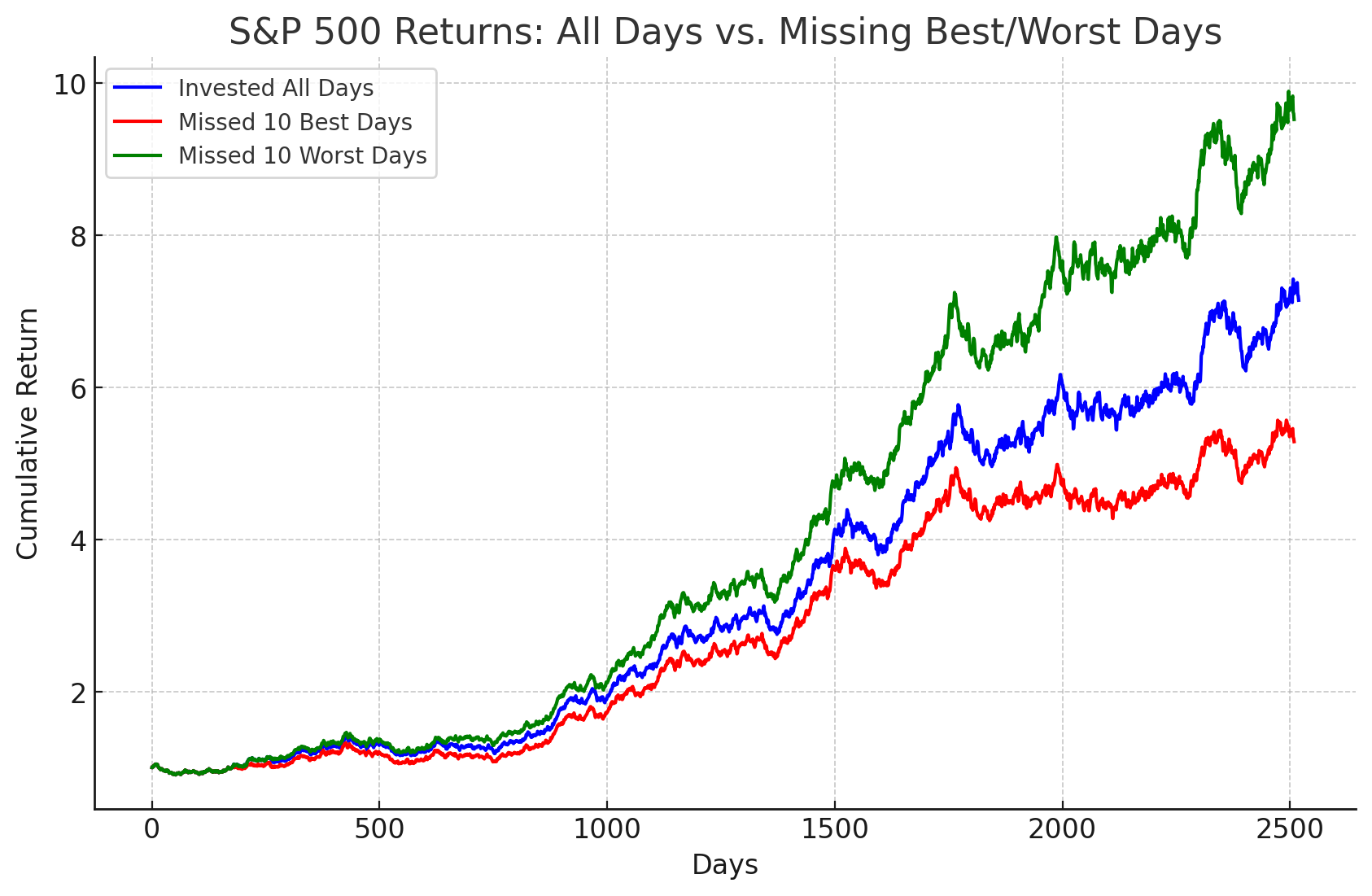

Out of curiosity, is there chart where - by using your super powers - you manage to miss the 10,20-60 worst days (and got all the rest - bad and good)?

Q: give me a chart where you’re invested at all days in the S&P 500, one where you’re not invested on the 10 best days (but invested on all other days) and one where you’re not invested on the 10 worst days (but invested on all other days)

A: Here’s a chart showing the impact of missing the 10 best and 10 worst days on S&P 500 returns. You can see that missing the best days significantly lowers returns, while missing the worst days boosts performance. Let me know if you want to refine the data or analysis!

No not at all, I am just talking about extra liquidity I was building for 8 months (now into gold for a month) which if we see 10/20/30% drops I’ll put into my usual stock buying. Not planning to ever be out of the market.

The more I’ve looked at this chart the more unrealistic it seems, as you and others pointed out. The message is clear: don’t try to time. The how is…“don’t try to time because in reality jumping in and out at the precisely right moment is practically impossible”. The chart is irrelevant to anyone never intending to exit the market.

Maybe I’ve missed some satire signal, but isn’t this chart a total bullshit? It implies you could 7x your investment over 2500 trading days (which is ~10 years). You need to compound at 22% annually or so to get that.

Initially it was realising I went so pedal to the metal in 2023-2024 that I had a paltry emergency fund that would cut it very fine if I lost my job and before benefits. Then gradually, after building the emergency fund to where I wanted it to be, we came to ~November where I felt volatility was coming (for real this time!) so I kept on saving cash. As you know from our convos I was looking for something to do with this cash for a while, and I settled for gold, part due to FOMO, part due to studying its impact in long-term portfolio building, partly because I simply disliked holding cash (so I chose to pay for a metal I can’t even fondle being stored in a Zurich vault!).

I have set targets for both deploying the liquidity (the -10/20/30% drops and restarting putting new money in: 1 year after stopping (ie this July). It’ll just be VWRL, not 3A for reasons we’ve discussed in detail!

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.