Ah, but no -

“Selling now would be evil and counterproductive market timinig. I have the emotional fortitude to be above that ![]() . Unless temptation becomes too strong

. Unless temptation becomes too strong ![]() .”.

.”.

Ah, but no -

“Selling now would be evil and counterproductive market timinig. I have the emotional fortitude to be above that ![]() . Unless temptation becomes too strong

. Unless temptation becomes too strong ![]() .”.

.”.

I was tempted to sell, but I found it hard to do so as I am now mostly happy with my portfolio.

I might take one more critical look to see if some positions are over-valued or too long duration to maybe cut back.

I still have about 10% margin debt and ideally, I’d like to have 10% dry powder.

I’m fairly new to investing. I’ve seen it everywhere, including here, that you should just put money into a World ETF every month and forget about it until retirement, ignoring all the noise. ‘Time in the market > Timing the market.’

This seems to be the standard advice on forums, Reddit, and YouTube for clean, hassle-free investing. However, the more I research and hang out on these platforms, the more I see people choosing active ETFs and trying to optimize every possible percentage point. I see people talking about selling, and so on.

Are you doing this because your own advice doesn’t apply to your style, or is it just harder to ignore the noise than expected? It’s a genuine question since I’ve only been investing for a year, I’m still figuring out how reality differs from the theory I read everywhere.

PS : My english is not good enough to write all that in a comprehensive manner by myself so i used AI to correct my text

Really? I saw that you had to YOLO everything on 0DTC options.

It can be several things. It can be fear. It can be greed. It can be something else.

Speaking for myself, I think it’s hubris. The market reactions seem so blind that I can’t help thinking “surely it can’t be that hard to beat that.” So I fiddle with predictions though, sometimes, I remember that the market can stay irrational longer than I can stay solvent and that it can wander in all sorts of directions on a relatively long term.

I think one of the keys is minimizing regrets. If you are fine enough with what you have done so far, the temptation to try something else becomes lesser. It’s a simple concept but hard to live by day after day.

Thanks for the honest answer.

Do you find that the more you learn about investing, the more you think you can beat the market or make ‘good’ trades?

Since I don’t know much, every time I see the market go red, I want to do something. But then I think to myself: I don’t know enough to deviate from the basics that people recommend, and I’ll probably just end up in a worse position.

Is ignorance bliss, in a way? (Not too much, obviously, because the basics are necessary.)

Yes, absolutely.

No. The material I’ve read is all about finding a strategy you can follow and sticking with that. It makes a lot of sense to me and I don’t feel a need to study trading tactics in depth. In my opinion, part of the stock premium you get by being average and getting the market returns comes from the people who enter and exit at the wrong time.

I would differenciate learning through reading, learning through watching and actual market experience, though. To note, I have not yet had the opportunity to have a sizeable amount of assets invested so I lean on the more theoretical side. My feeling about myself is that I am strongly driven by inertia so my bet is that once I’ve got a sizeable amount of money invested, I would lean toward following my strategy and riding the crashes all the way down and all the way up rather than tinkering. That’s non battle-tested and takes into account my assessment of my own personal psychology, which isn’t everybody’s.

Also to take into account that life doesn’t often let you choose when it throws a curve at you. Money that is invested can become useful for other things at various points without warnings. Those would also be situations where one might change their allocation at the wrong time. I’m probably more exposed to that than the average person.

That’s just a form of availablity bias.

A degenerate gambler will have a new story every week. They won big in semiconductor options, sold their oil too early just before the price spiked, and they’re analyzing an exciting opportunity in Asian real-estate or whatever. They will be making a thousand transactions a year, and each one will feel worth talking about.

Somebody investing regularly in highly diversified ETFs has very little to say. It’s the same thing every month. You put your 2k CHF into VT, and it is doing just as well for you as for the 100 other forum members doing the same thing.

The few discussions you can have tend to have crisp and conclusive outcomes. They’re had once or twice, and then the answers don’t change.

So you’ll see a lot more discussion of the former than latter, and it is giving you a biased view about everyone actually being into stock-picking and market-timing.

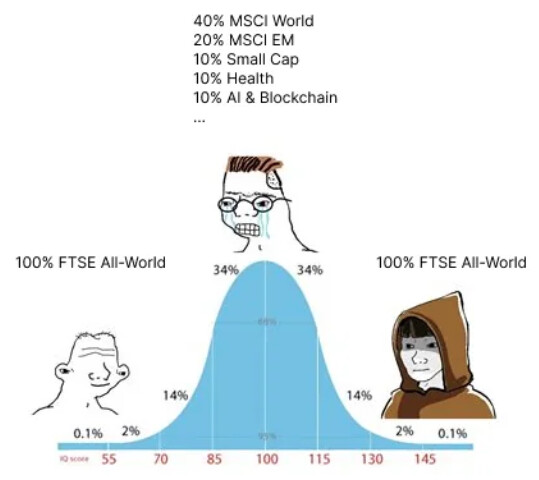

I love this meme:

The middle one gives more to discuss, that’s why every forum revolves around the middle one.

I think everyone here is different, everyone can only speak for her-/himself.

As for myself: yes, I see a difference between giving advice and acting on my own behalf. Acting on my own behalf is much more active, trying out new things, questioning the existing (VT-and-chill). This is all good for someone like me who is interested in this topic and has fun spending time on it. But for friends and family who want to spend as little time as possible on financial topics, I currently recommend VT-and-chill in slight variations adapted to their specific situation.

I think there are many ways to invest. The VT and chill is simple and suits a lot of young people with a long investment horizon.

However, not everybody wants to take 100% stock market risk, esp. as they approach retirement age.

I have broadly 60/40 risk and even in the stock component, I prefer steady, profitable boring companies, in general. On the one hand, this means I will not be getting 20% annual returns from NVDA going to the moon, but likewise, the downside is also reined in.

Buy low, sell high.

Sometimes people confuse this with buy red, sell green.

Sometimes red can be low, but not always.

@dbu unleash the “here we go”?

Its because most people believe that investing in stocks is like buying a fixed deposit with higher interest rate. They don’t pay attention to volatility that comes with it and what impact it might have on their psychological well being.

in addition, unless you are invested for 5-7 years, there is a high chance that bear market will bring the whole portfolio under water (meaning the value will go below the invested capital) and this is a tough pill to swallow for post even though in theory that’s how equity investment works

Lower than yesterday.

Selling at any stage (that is not rebalancing towards target weights/glidepath to retirement or using it to fund your life) to me is admitting you are not comfortable with your asset allocation (or weren’t informed enough on what you are getting into) and you should re-assess your risk tolerance and said allocation.

while this is a common quote and intuitively correct. In practise, it only really works with hindsight (after the fact). And is, in my opinion, a dangerous paradigm for practical portfolio management particularly for beginners.

For most investors wrong behaviour during market stress is the biggest risk of all. Any strategy that requires constant decision making (e.g. sell/buy) based on market situations - beyond balancing - is particularly prone to behavioural risks.

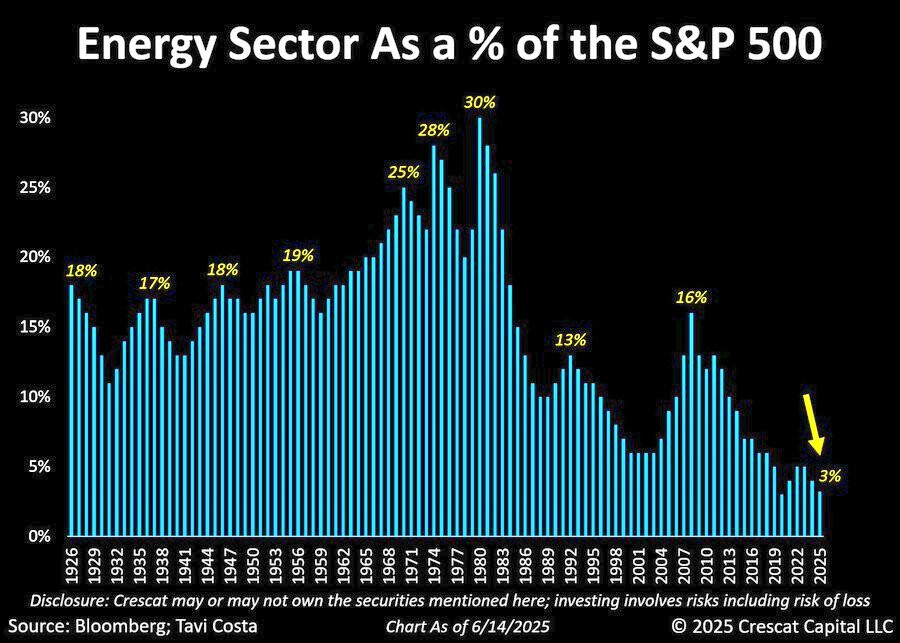

Let’s check:

And my strategy for 2026 was energy, which has already gained a lot.

What is still undervalued? Various SaaS companies: CRM (new position and now 6th biggest in portfolio, currently 10% down), MORN, DOCU, etc. CHTR is more risky/uncertain but risk/reward is good enoug to go on at 11th biggest position (currently 11% down). Let’s check back on 24 months if these pan out (or maybe longer if Iran tips the world into a stagflationary recession).

My current portfolio breakdown:

| Classification | Yield | MV% |

|---|---|---|

| + Oil&Gas Midstream | 6.8% | 8.5% |

| + Oil | 2.6% | 8.4% |

| + Tobacco | 5.6% | 8.2% |

| + Gold miners | 1.9% | 7.8% |

| + Commodities | 2.4% | 7.2% |

| + Natural Gas | 3.1% | 6.7% |

| + SaaS Plus | 1.6% | 6.4% |

| + SaaS | 0.6% | 5.7% |

| + Uranium | 3.8% | 5.6% |

| + Turnaround | 2.6% | 5.2% |

| + REIT | 6.1% | 5.1% |

| + Oil Refiners | 2.3% | 4.4% |

| + Insurance | 4.7% | 4.4% |

| + Consumer Staples | 5.6% | 4.4% |

| + Healthcare | 5.7% | 3.7% |

| + Health Insurance | 1.2% | 1.9% |

| + Tailrisk Hedge | 1.8% | |

| + Software Infra | 1.6% | |

| + Silver Miners | 1.0% | 1.1% |

| + Dividends | 5.0% | 0.8% |

| + Swiss | 1.3% | 0.6% |

| + Oil Services | 0.1% | 0.5% |

| Total | 3.4% | 100.0% |

As you can see, it is heavily tilted towards energy and real assets and is designed to be more resistant to a stagflationary environment than S&P 500.

Gold was out of favour when I weighted it. Same with energy (even now is still out of favour after gains post-Iran). Saas I started buying this year as people panic-sold due to AI fears (these are still risky as many are long duration and will be vulnerable to an economic downturn and increased interest rates that could be triggered by an oil shock). Tobacco and commodities have been out of favour for a while. Uranium is niche and may be making a comeback.