Ben Felix had some data showing that we were very far from passive investing introducing inefficiencies to the market, and also said that if that became the case then active traders would exploit them fast enough to eliminate them.

Broadly, the cancer that is media nowadays means there has to be a click-generating narrative 24/7.

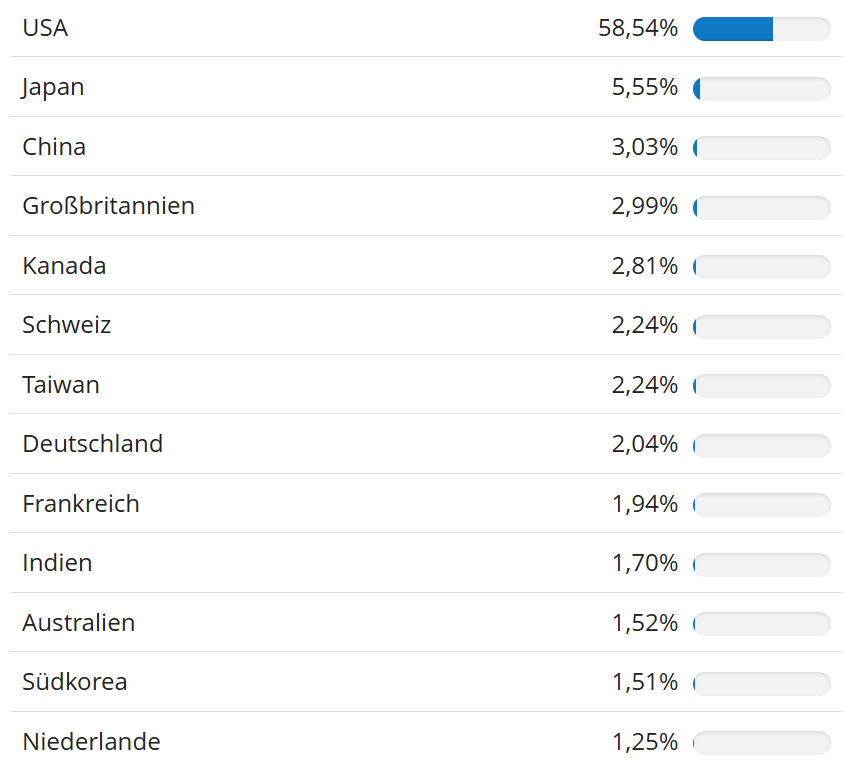

While my personal strategy is to “VT and chill”, Modern Portfolio Theory actually shows that you only need about 20 to 30 uncorrelated stocks (across various sectors and regions) to eliminate most unsystematic risk. Beyond 30, the marginal benefit of adding more stocks drops off significantly.

With 30 stocks and the IBKR TWS rebalancing tool, I think it would be rather easy to implement.

Well stockpicking still need someone to buy all the stocks in particular ratio. If an ETF existed which allowed selection of N number of stocks where new contributions are invested proportionately, then it would be easier than stockpicking.

I personally don’t care because for me Large and mid cap ETFs are fine. I can play around country weights using different ETFs.

Fair point! My 20-30 number was definitely based on an outdated memory, and I should have double-checked the current science. You’re completely right that modern data (and Ben Felix) points to needing 50-100+ stocks to actually diversify in today’s market.

Utmost care and consideration must have gone into that overnight hike.

Now, this new ‘tested and lawful legal basis’ seems unlikely to survive legal challenge, too:

… But the actual language of the Trade Act lists requirements that don’t exist today, including a “large and serious” balance-of-payments deficit. While the U.S. has run a trade deficit for decades, it’s been offset by capital inflows as foreign investors pour billions into financial markets, resulting in a net balance of zero. “Section 122 of the 1974 Trade Act, on which Trump’s 10% tariff is based, does not apply in the current macro environment,” said Peter Berezin, chief global strategist at BCA Research, in post on X on Friday. “A balance of payments deficit is not the same thing as a trade deficit. You cannot have a balance of payments [deficit] if you have a flexible exchange rate, as the US currently does.”

Similarly, economist Alan Reynolds, a senior fellow at the Cato Institute, pointed out that the trade deficit is fully funded by the capital account surplus, adding that there is no overall balance-of-payments deficit to justify Trump’s newest tax on imports. Bryan Riley, director of the National Taxpayers Union’s Free Trade Initiative, wrote in a blog post last month that Section 122 only makes sense under a fixed exchange rate, which hasn’t existed in the U.S. in more than 50 years. Back then, when the dollar was pegged to gold, there was still a risk that the U.S. could suffer from shortages of reserves needed to cover international obligations.

Well it will be interesting for the administration to argue that the US is likely to run out of dollars, the way it may have run out of gold bars in the gold standard era - which incidentally was ended in 1971 with that law being written shortly after, to avoid relying on the illegitimate emergency measure invoked by Nixon…

I’m not sure a court would care tho, the law doesn’t mention anything about gold standard, only balance of payment account.

The reporting I’ve seen on financial newspapers seem to think section 122 will stick.

The main issue for the administration is that they can’t play with it like they did with tariffs in the past year:

only one global rate, limited exemptions

time bounded

Where it might hit the courts is if the administration tries to let it laps and immediately renew it (but even then, it’s unclear it would be an issue, the balance of payment would not have been fixed in the meantime, so they have a decent claim)

Also this time, reading the WH official justifications, it seems like they took some care to keep it tight.

I think a lot of it is going to come down to if whether there is a balance or payments issue or not is justiciable by the courts, or if any such declaration is non-justiciable, i.e. the courts won’t second guess it.

They can’t say do this and tariffs will be removed. Do that and tariffs would be placed on a specific country.

Now it’s basically 15% for all for everything. So no one needs to negotiate anything because no one can get a relief. Not sure how UK thinks about it because they had a 10% deal.

The key question would be how other countries react to tariffs on US products. Would they be reinstated or they will stay zero. Reality is that since 15% is applied to everything , the effective tariff might be higher than before for countries with trade deals which means US is not holding up to their end of bargain.

Exemptions for certain sectors are also a feature some countries may have cared for in their deal with the US. That might be gone too even if they had a rate equal or higher than 15%, which would be another way in which the US would have renegued on their commitments, justifying dropping the deal or alterating it.

That being said, I doubt most countries are eager to go through another round of negociations. If a flat 15% on everything, affecting every country equally, is good enough for them, I doubt they’ll do much of a fuss. They’ll react when/if they need to exert pressure on the US for geopolitical/economical reasons. Some countries more willing to challenge the US position as world leader might do it without waiting.

42% Japan

35% Switzerland

10.5% US

6.5% EM

3% EU

3% Crypto

Decided to take a bet on Japan end of last year after monitoring the market for a while. It’s only temporary, and I plan to DCA the whole year into mainly VT and BTC.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

Stocks")