To sum up, you would probably buy something like:

ISIN: CH0032912732

I was comparing SMIM and SLI and noticed that the valuation differs significantly. SMIM has PE of 31 and SLI 15.

Sure Mid Caps are expected to have higher growth and therefore command a higher valuation, but 2x the valuation of SLI?

Am I missing something?

Morningstar say 16 (slicha) und 19 (smmcha) respectively for me?

Although they use forward p/e

Yahoo that uses trailing p/e, has them at 19 and 20.5

That‘s also not a general statement you can make. In this case it would be purely swiss market specific.

Look for example in the US, where it‘s reversed basically and large caps have higher p/e.

Looked at the data on the ishares ETF site for both. Strange

EDIT: yahoo shows the same values you mentioned for the ishares ETFs. I guess Blackrocks excel formula to display the PE is linked to something else ![]() , pls fix

, pls fix

1 Like

Hi folks,

Long story short: I would like to invest 20% (my home bias) in a Swiss ETF (150k) - I currently have 600k VT and my 3a invested on FP.

In the old time, I was using CHSPI but sold it (with benefice) to focus on VT. Now I am considering SPICHA (which uses basically UBS and not iShare). I’m also interested by SLICHA which seems to yield higher returns but is less diversified.

What would be your recommendation and way of thinking? (bonus point: DCA or lum sum for Swiss market?)

My rational thinking is the following:

- CHSPI vs SPICHA: both have the same TER of 0.1 and have similar returns. A small difference is that CHSPI has 202 holdings and SPICHA has 194, so in terms of diversification nearly the same. However, SPICHA uses UBS which would make me prefer this option to have also the share provider being Swiss.

- SPICHA vs SLICHA: SPICHA has 38% over 3 companies. SPICHA has max 9% companies but “only” 30 holdings and a TER of 0.2%. However, SPICHA seems to yield higher returns but is less diversified.

So I think my hesitation is between SPICHA and SLICHA where one is more diversified, lower TER, and lower returns and the other one has 32 holdings, 0.2 TER, but higher returns.

PS: I don’t know how fees differ on IBKR, maybe this can be taken into consideration.

1 Like

Why not use your 3a (on FP) to invest Swiss funds with a very low TER? (and replicating, for example, the SPI Extra)

What motivates you to have a home bias again after the sale of CHSPI?

1 Like

If CH stocks are 20% of your portfolio. Then even if CHSPI is 38% concentrated in Big 3, the overall weight of Big 3 in your portfolio would be 7.6%. is this an issue?

If not, then why should you over complicate things?

Don’t know how much you have on your 3A but I would put all in on SPI Extra. It’s damn cheap and diversified with mid and small caps.

Then you can do a mix of SPICHA, SMIM or SPMCHA depending on the amount you already have on 3A

1 Like

Thanks for your answer! Before I had CHSPI and also 150k on Swiss bonds, so my allocation was too much into Swiss markets. So I sold initially the CHSPI. Now I sold the Swiss bonds that were pretty positives.

Since I’m currently happy with my 3a, I’d prefer to not touch it ![]()

Thanks for your answer! It feels that 38% concentrated in Big 3 is a lot, especially if 7.6% of my overall portfolio is as well (may sound being partially a stock picker). What are your recommendation in that case?

Thank you for your answer! Do you have experience with spicha + smmcha or spmcha or example of portfolios? I will read the product description and TER and understand how does it compare to CHSPI. This could be an option if TER is not exploding.

I feel SLICHA makes more sense to me, biggest and most liquid stocks, capped at 9%. CH is a small market so it picks winners. It’d be my choice, but currently planning to build up non-equity assets.

1 Like

Just to be clear

80% VT + 20% SPI will mean

8.65% exposure to Apple, NVDA & MSFT

7.68% exposure to Big 3 in CH

Anyhow, if you would like to reduce your exposure to big 3 in Switzerland, you have two options

- use combination of SPI + SMMCHA

- Use SLICHA + SMMCHA

3 Likes

Hi Folks,

Following up on this thread. I am newbie when it comes to Swiss Market ETFs.

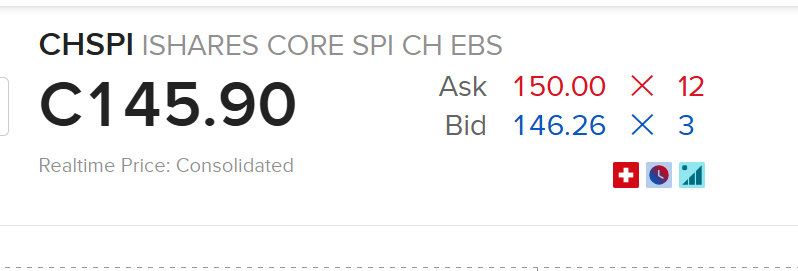

Why is the trading volume of ETFs like CHSPI so low as displayed in IBKR?

Also Bid/Ask spread is pretty wide. What if you need to sell for Ex. 100 Shares or 1000 shares (assuming you accumulate a large position in the Future)

Wow, never seen such a big spread! I guess it may be a lot more liquid on Swiss brokers? On Swissquote it’s at 146.26/146.30 right now, volume 6,329.

Exactly, I am curious why IBKR shows this different view compared to Swissquote.

It seems that Swissquote is better for investing in these Swiss ETFs?

It’s very well possible that the actual trades will be fine at IBKR and this is just some issue with market info. However, the SIX market data provided by Swissquote is certainly better than IBKR (at least without any market data subscriptions).

As I have both, IBKR and Swissquote, I normally use Swissquote’s market data if I trade at SIX, even when I trade at IBKR. Never had an issue with actual trades on IBKR that way.

4 Likes

I don’t know when or where you took this screenshot. I trade and own CHSPI on IBKR and the spread now is 146.30/146.28.

Interesting. I’m seeing the terrible 150.00/146.26 at IBKR right now. I don’t hold CHSPI at IBKR, though.

Do you have any market data subscriptions at IBKR?

1 Like

The screenshot was taken today at 13:38 from the IBKR Website. Perhaps I am missing the proper market data subscription