My wife and I are considering purchasing a house in the Basel region (BS, BL) this summer. We plan to use our 3a pillars, and I also intend to utilize my 2a pillar for this purpose.

Currently, I don’t have a 3a pillar account, but I’m planning to open one shortly. However, I have some concerns regarding the mortgage, especially after speaking with someone at VIAC. They mentioned that banks might not accept a 3a account if it’s held with a finance company like VIAC, rather than a bank.

This is a significant issue for us. I’ve been thinking about using HypoPlus, as I’ve read many positive reviews about their ability to find competitive interest rates. Yet, I’m uncertain which bank would offer the best rate and whether they would accept our 3a account, especially if it’s with VIAC.

From what I understand, VIAC works with WIR Bank, which accepts VIAC 3A. However, there might be better rates available through HypoPlus, but they might not accept VIAC.

The extent of my knowledge on this topic is as described above, and I’m unsure if my understanding is entirely accurate.

My question is, how should I decide on a 3a pillar for both myself and my wife, considering we might need to transfer it to another company for mortgage purposes?

I assume you want to pledge your (future) 3a and probably use indirect amortization.

More precisely, most if not all lender banks want the pillar 3a to be held at the same bank. E.g., I also don’t expect ZKB accepting the pledge of a UBS 3a account.

If you want to pledge your 3a, you likely have to consider the mortgage and pillar 3a as a package deal. If reasonable 3a fees are your priority, your best bets are one of the combinations frankly+ZKB or VIAC+WIR.

As a side-note, if you can afford both, pay the full amount into pillar 3a and direct amortization of your mortgage, I would do that instead of indirect amortization. See https://finpension.ch/en/indirect-amortization/

@PhilMongoose Thank you for your response. I wasn’t aware that it’s common for lenders to not accept pledges.

@jay, Thank you for the reply. I believe the most sensible step is to consult with HypoPlus before investing in a 3a account. If they are confident about securing a better rate than WIR or ZKB, then investing in a 3a might not be the best option for a mortgage, if my understanding is correct.

Here’s my question: Would it be wise to open a 3a account, say with VIAC, this year and add the maximum allowable amount also next year, then withdraw it for the mortgage in the summer, instead of using it as a pledge? As I remember that finpension charges around 200/250 CHF fee for withdrawals.

I find myself quite confused about the best course of action. The process seems complicated, with many different approaches, and I’m struggling to determine the most advantageous one.

My experience is that some lenders ( eg. Migros Bank) require a pledged 3a from an insurance company, this way they are protected in case you stop paying… Unfortunately such products have known issues with transparency and costs

I would focus on “good enough” and not strive for the most advantageous course of action: my time and mental energy have value too.

In that prospect, I would want the entity holding my mortgage:

to be a partner I trust.

to offer a decently low rate. I’m using VIAC’s displayed rates as a quick gauge but @Cortana has been seen providing current data (because he’s a great guy ).

to offer the way of financing/amortization I am searching for (pleged 3a assets counting as downpayment and/or indirect amortization).

If you want to pledge your 3a assets or use indirect amortization, it is worth it to check if the institutions you are targetting do offer interesting options beforehand. For example, I wanted to work with my local Raiffeisen for personal reasons (I like the people there and don’t mind paying a premium to support them) but was disappointed when I discovered without having done enough due dilligence that getting 3a assets to be pledged and counted as downpayment will require tough negociations, if it will be possible at all (signs point to no).

My prefered ways of financing would be, in that order:

not using 3a assets at all.

Pleging 3 a assets, keeping maximizing 3a contributions in another account, using direct amortization, freeing the pledged 3a assets as soon as possible.

Same but with indirect amortization if I can’t both max new 3a contributions and meet the direct amortization amount.

Withdrawing 3a assets, keeping maximizing 3a contributions and using direct amortization.

Withdrawing 3a assets and using indirect amortization if I can’t both max new 3a contributions and meet the direct amortization amount (at which point, I would ask myself if I shouldn’t save up more/reduce the amount of house I’m trying to buy/reduce my expenses and/or find a way to increase my income).

Unless I’m going for indirect amortization, I wouldn’t care much for having a good investment possibillity for my 3a pledged assets: I’d just keep them in a 3a bank account and focus on freeing those assets as soon as possible, then invest them with my provider of choice.

The first step is to find the cheapest mortgage you can get. Once you do, then check with that lender about their requirements for pledging and/or indirect amortization. There is no point in choosing a pillar 3a solution before you know the mortgage lender’s requirements.

If the mortgage lender only accepts a very unfavorable pillar 3a solution (e.g. a pillar 3a account with very low interest), then you can look at mortgage lenders that are slightly more expensive, but offer or accept more profitable pillar 3a solutions. You can then compare the additional cost for the mortgage to the opportunity cost for your pillar 3a. The results will show you whether using the mortgage that’s more expensive but has better pillar 3a options is more profitable.

It’s also important to differentiate between pillar 3a pledges (towards your down payment), and indirect amortization using the pillar 3a (amortizing your secondary mortgage). The same mortgage lender may accept pillar 3a pledges from other retirement foundations, but require that you use their in-house pillar 3a solutions for indirect amortization.

Remember the saying “Penny wise, pound foolish”. The lowest mortgage rate you may save 0.5% vs. WIR but does it make sense if you miss out on higher probable growth in the long term?

This is not advice, do your own research - you need to consider your risk profile and your capacity to cover debts, stock markets can also crash 50% or more

Well since the deposit is 20% and the mortgage 80%, every saving of 1% in the mortgage would have to be matched by the equivalent of a 4% increase in bondlike return in the 3a to be at parity.

I recently reached out to a senior consultant at HypoPlus. He informed me that they partner with institutions that accept 3a pillars, so I should proceed with my plan to open 3a accounts for pledging purposes. He also advised that once I find a suitable property, I should contact him directly.

It seems that this will not pose a problem.

Although I haven’t yet utilized HypoPlus’s services, the Google reviews I’ve read are very positive. Many people mention that HypoPlus secured better rates than they could find on their own, and that the company provides guidance at every step. The service fee of 250 CHF seems quite reasonable to me, especially considering that they have been helpful even though I haven’t made any payment yet.

Just a word of warning: I also used a mortgage agent and they make you sign something which says you have to take the mortgage they offer or pay a fine.

The mortgages they offered were no better than what I found on my own.

I’d also check the insurers such as BVK.CH as they have (had?) a structural funding advantage over banks and so should be able to offer better rates.

I did go with BVK in the end and liked that they published their rates on the website. I got 0.75% fixed 10 years (public rate) which was almost half of what the mortgage broker was able to find and I got better conditions too.

@PhilMongoose, I truly appreciate your crucial insight. You’re a lifesaver!

“In the event of successful mediation of an offer from a provider approved by the applicant, the applicant agrees to either accept the offer or otherwise to pay administrative fees of CHF 2,000 (excl. VAT). These administrative fees cover costs related to providing the services promised, including third-party fees such as land register and/or debt collection statements. This also applies in the event of a revocation of this authorization for the administrative fee and for the consultation fee. There is no guarantee of the comprehensiveness of the scope of services.”

As you mentioned, if I decline the given offer, I’ll be facing a charge of 2000 francs + VAT. Wow, that’s astonishingly high.

Perhaps my initial approach will be to negotiate directly with banks to secure a rate. Afterward, I can approach HypoPlus and propose a condition in the contract stating that if they can’t find a rate better than the one I’ve secured, I won’t be liable for any fee. If they agree to this term, I’ll proceed with them; if not, then I won’t.

This is a really important consideration, one I hadn’t thought of before.

Regarding fixed or SARON interest rates, I’m still undecided. My current plan is to opt for SARON, and then switch to a fixed rate when the interest rates lower. However, I’m open to suggestions and would appreciate any alternative ideas.

I’ve learned so much from this forum. Thanks to everyone once again!

I would try to have that in parallel, because time for financing might be essential (meaning, you will only take their offer up, if it is the best one). However, how do you define best one ? Since the rate is not the only condition (other contractual terms like direct/indirect amortization, the possibility to make an extra payment to the mortgage, the possibility to refinance before the end etc.).

Your question is insightful, and I must admit that I don’t have a comprehensive answer as I am still in the learning phase.

Could you please provide your perspective on the best option? What factors should I consider? Your insights would be immensely helpful for me to understand and adapt to these conditions

Unfortunately my knowledge would end with what I said for the Swiss market. My experience is limited in Switzerland since it is so different (the goal is not to fully own the house, but to own only 33% of it - which for me is kind of weird), and I am not aiming to buy in Switzerland for now.

What is really relevant or not or even negotiable is kind of different between Switzerland and the rest of the world (for instance, an extra payment to your mortgage is less relevant here than somewhere else - since you do not pay back the house completely anyway - at least in todays conditions).

Also, I could not find any Swiss specific literature for that topic (except stuff from banks/insurances etc. where a risk for bias would be heavy).

Maybe @Cortana or someone else from the finance industries can give better insight for what is relevant, even negotiable etc…

I‘m heavily occupied these days, but would like to share some insights. Just don’t have the time to read the whole thread. Could someone specify the question?

I’m in the process of planning for a mortgage and am considering the option of opening multiple 3a accounts with VIAC and/or Finpension. The plan is to pledge these accounts for the mortgage, allowing me to continue contributing to my 3a. However, I’ve learned that many banks might not accept such accounts for pledging but only for withdrawal.

I’m trying to figure out the best approach for my situation. What should I be considering in this context? Additionally, I’m thinking of working with HypoPlus to find a better mortgage deal. But I’ve also learned from this forum that if I don’t accept their offer, I might have to pay a fee of 2000 CHF plus VAT.

Shortly:

Any advice or insights, especially regarding the use of 3a accounts as pledges and working with mortgage brokers like HypoPlus, would be appreciated. Thank you for your time and help

Indirect amortization is the way to go in my opinion. Why save 2% in interest if you could gain 4-6% with an invested 3rd pillar instead. The limitation is that you can only do this with the bank where the mortgage is. The only exception is a 3rd pillar life insurance, which sucks anyway (see all the threads about people trying to get out). Still, even with a 1% TER it‘s a much better deal than direct amortization. Cover what‘s required with the mortgage bank and pay/invest the rest (if there is one) with Viac or Finpension.

UBS has Vitainvest Passive 100 by Key4 with 0.75% TER. It‘s still 0.35% above the best Fintech offers, but still better than an actively managed fund. Some banks like PostFinance offer only actively managed 3rd pillar funds. So take this into account when comparing interest rates (including the compounding effect).

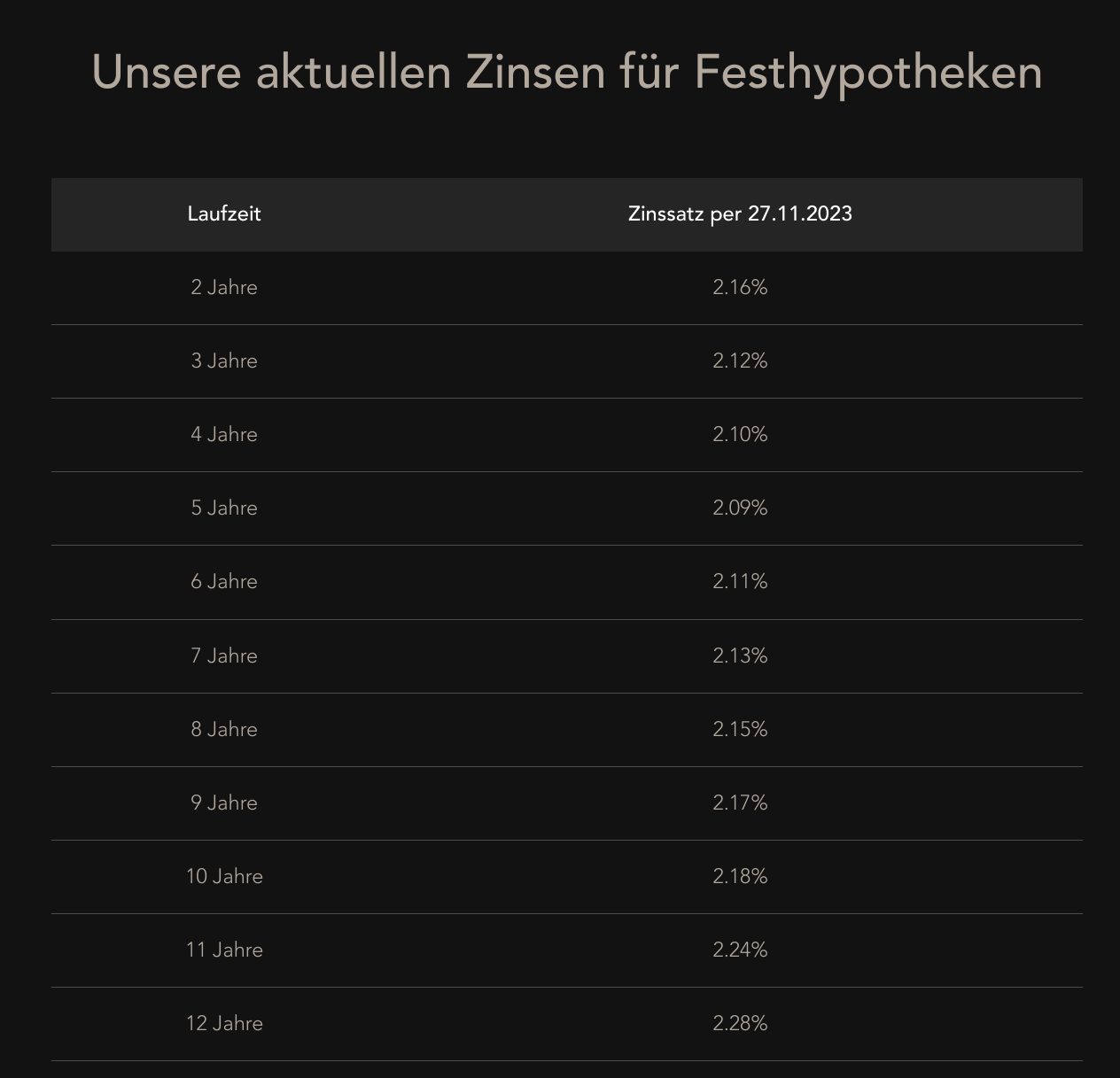

VIACs offer is decent, but it can go lower. You should be able to get 0.60-0.65% margin on Saron, ~1.8% 5 years and ~1.9% 10 years if you look hard enough (as per 29.11.2023). I would advise against HypoPlus, MoneyPark and the others. You usually have to pay 2-3k if you don‘t accept their offer and can‘t show any evidence of a better offer. Just contact 3-5 banks and be open about your „shopping“ of mortgage rates. Once you have the best offer, show it the the other banks and try again for a new final offer. Then pull the trigger.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.