Mustachian Post Community

CHF short term deposits

Investing / Portfolios

ma0

March 22, 2023, 12:44pm

6

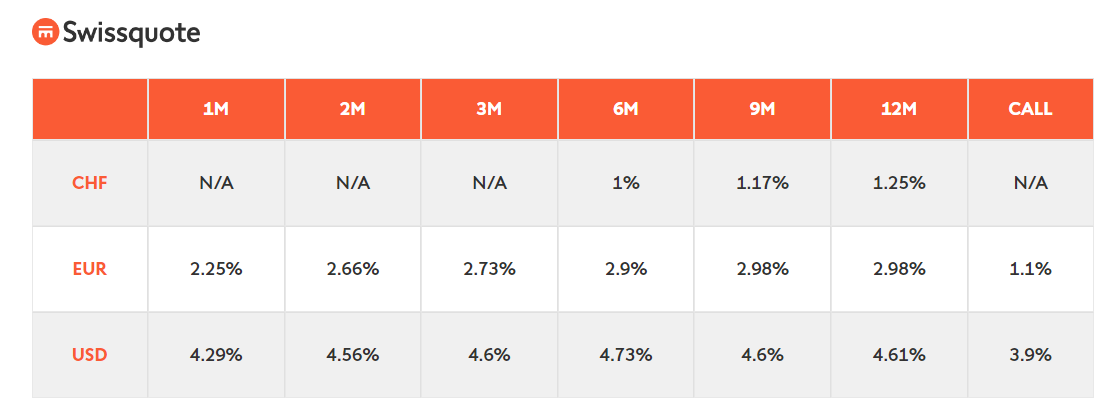

image

1096×405 17.6 KB

show post in topic

By reading and partipating to this forum, you confirm you have read and agree with

the forum guidelines

and the disclaimer presented on

http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec

les guidelines du forum

et l'avis de dégagement de responsabilité présenté sur

http://www.mustachianpost.com/fr/

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die

Forum-Richtlinien

gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf

http://www.mustachianpost.com/de/

akzeptierst.