So I went and checked for some of them in the above list. Beware of entry and exit fees. For example LU0120694640 (Vontobel Fund - Swiss Money) has an entry fee of 5.00% and an exit fee of 0.30%. It would take years to even get back to were you were.

If you don’t have multiple millions of net worth, paying around 2.00% for premature termination on a savings account, would probably be cheaper, and give higher returns for comparable availability.

Isn’t that up-to 5%? (it will heavily depend on your bank/broker, with Swiss ones being fairly expensive so that it likely doesn’t make sense for short term holding).

Wow, this is wild. Why doesn’t the national bank give us access to something like T-Bills in the US? At least Swiss residents should be allowed to access them directly, imo.

On a second glance, yes. And there is also some stipulation in their KID about up to 500 CHF entry fee if you exit after 1 year (I don’t get what that’s supposed to mean).

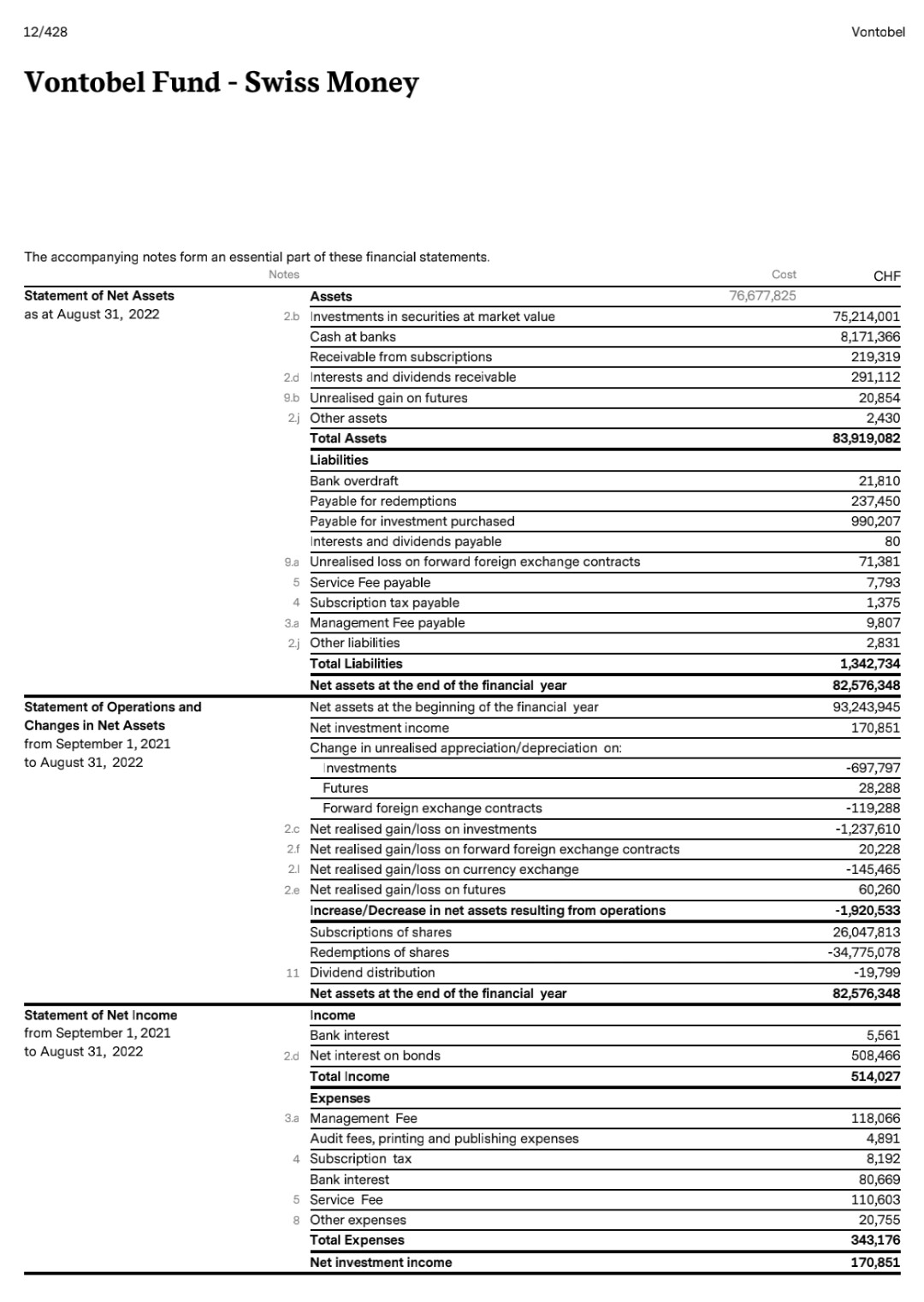

It seems cost isn’t transparent. I didn’t find the actual rates and I can’t read their annual report well enough to calculate it. Not understanding a product is a good reason to keep your hands of.

The annual report in 2022, if someone wants to try:

Thank you so so much for the reply. Regarding this paragraph particularly, I am still quite confused. If the performance 0.2% for four months continues in the rest of the year, the whole year performance is gonna be like 0.6%. This is still very far from number of YTM, like 1.5% - 1.9%. So apparently there is some basic fix-income knowledge I don’t get.

Seeing YTD performance 0.6% and YTM 1.5%, If I invest 100k and expect to exit after a year, should I expect 101.5k or 100.6k? I know in a savings account, I can expect 101.5k. Essentially I am looking for a savings account alternative, hopefully getting similar rates locked for as long as possible (1 year) by doing it myself. Is the thought too naive?

Don’t think you should expect anything, all the yields are moving which makes it hard to predict (and might not be held to maturity). If you have a specific horizon and want to lock-in some rate, check fixed term deposit, bonds or notes.

What I don’t get is how a fund-side entry fee can be dependent on the broker. If my money reaches the mutual fund, they need to buy more securities, regardless where it came from. Or is there some broker-side pooling and netting going on?

At the moment, I just want to know if it’s possible to do so, satisfying my curiosity. Learning some instruments. If the answer is yes, I will then start thinking about when and why and why not to do it

Thank you for the reply. I guess the money market fund is not a good alternative to savings account then? I thought the money market fund generates similar yield to a saving account, trading locked interest for a fixed period to flexibility. Is that wrong?

I am not even thinking about fees yet. Just the performance, should I be happy about the one with YTD performance of 0.2%? It’s the best one I found in the list. Or maybe this is a very bad metrics for money market fund as the policy rates are changing? Should I look at annualized last month return? last week return? Is YTM a good metrics evaluating the money market fund?

FYI I’ve ended up using the Pictet LU short term MMF. Mostly because of if its size (billions).

I think it currently yields >1% net of fees while being liquid (can get access to money in a few days). Tho compared to fixed term deposit accounts and similar, this isn’t insured.

It’s a fund, so it is not insured but regulated and, unlike bank accounts and short/medium term notes, the fund’s assets must be segregated from the managing company’s funds. I mean, I don’t think it is more “risky” than a savings account, the “insurance” is just done differently.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.