I’m in pursuit of a nice bond. I just can’t believe yet, that there aren’t any solutions to the problem except having plain old cash?

Hedghog’s comment is all I found concerning this topic.

Hedgehog:

Yeah, fixed income options aren’t looking any good these days. Any CHF denominated or CHF hedged especially, all yield negative or far below 1%, which just isn’t enough for me to bother.

I’d like to open a discussion and learn some more about CHF hedged bonds.

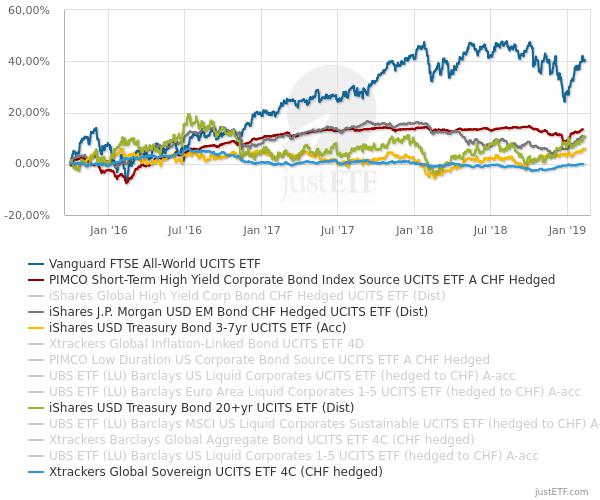

My bank gives me 0.05% interest. So anything above that, will win compared to cash :-). Here’s a comparison between VWRL (for reference), US treasury bonds and some CHF hedged bonds.

Let’s think differently.

Why would you like to invest in bonds? What is your investment horizon?

Is it not to lost money? Is it to reduce volatility? Reduce risk?

With the current central bank policy these are completely pointless for retail investors.

Interactive Brokers currently pays 1,9% on cash balances in USD. USD is almost pegged to CHF thanks to the SNB manipulating the price. They do not want you to keep your money in CHF bonds so don’t do it

I would simply put my spare cash in USD in my broker account and let it sit there

I have a DEGIRO account. You’re proposition isn’t bad, but I’d still find it a bit speculative to buy USD even with 1.9% on it. I don’t know, what might happen to these dollars in the future.

Do you think all bonds are pointless?

In this thread I’m not talking about Swiss bonds, but about CHF hedged(!) bonds. It’s not the same and I won’t be buying swiss bonds anytime with the current interest rates .

The central bank fund rate of Switzerland is currently -0.75%, so basically all CHF denominated bonds should be having a negative return. Now of course there are “risikier” bonds which have higher returns but those are probably too low because the base rate is manipulated by the SNB

The USD fed fund rate is currently 2.25% so there is a sizable gap between CH and US. Meanwhile the USD:CHF exchange rate has been pretty much the same for the past 5 years

Could it change tomorrow? Could the CHF gain compared to the USD?

Possibly, but I find it unlikely, mostly because the SNB is set on manipulating the swiss currency downwards and I do not see this policy change in the future.

Were you invested around 15 January 2015? The whole world bid CHF because the SNB would buy any amount of currency to keep the Euro peg … until it no longer did.

Do you really see bonds as less risky than stocks currently? (not saying that stock are not risky of course). With global interest rates that low, I am curious to see how bonds will tank once central banks will start raising them again…

I found the answer to a question of mine.

From the Vanguard analysis:

“The end result of the global bond and currency returns is a total-return profile that is similar to what an investor would achieve in her local bond market.”

…

“This also applies during periods of negative interest rates and bond yields. For example, consider short-term euro area bonds that had negative yields for each month of the year ended June 30, 2017: A euro area investor would have earned a total return of –0.07% over that period, while a U.S. investor holding the same portfolio hedged back to the U.S. dollar would have realized a total return of 1.63%”

It’s a zero-sum game. → Concluding not to buy chf-hedged global bonds.

Well, wether bonds in itself are more or less risky compared to stocks (which I think they are definitely less risky) is one thing. And it’s is not the point.

The point is to have less risk across my entire investment! That means not to have all eggs in the same nest! If stocks fall, bonds may stay stable and vice versa!

Having both bonds and stocks will certainly reduce risk.

If that were true about the constant USD:CHF rate, then it would make sense to purchase us treasury bonds since there wouldn’t be any currency risk, right?

Yes but since the Fed is currently raising rates medium term this is a bit risky as interest rates tend to rise and bonds fall. If they would reverse course this could potentially be a good investment. However in this case I think stocks will perform better for sure.

Another thought: When you have CHF income, you always have the possibility to invest more. However if you have income and all assets in CHF you carry a bigger currency risk than if you were to invest parts of it in USD. If Switzerland goes under you would at least have that

Not all my assets are in CHF. Bonds are only one part of the portfolio. Most ETFs have large amounts in USD anyway. So I’m already exposed to currency risk there. If Switzerland goes under, I’ll have that . This is the reason, why I’m searching for a less “currency risky” investment

From what I understand, you tend to think that when stocks go down, bonds go up and vice-versa.

That may be, or not, depending on where interest rates are standing.

Bonds return essentially come from three sources:

coupon paid

interest rates movements (when rates go up, bond goes down and when rates go down, bonds go up)

if held to maturity, the difference between the price paid and the reimbursed principal (example: you buy a bond for 80 and at maturity, it reimburse a principal of 100)

If tomorrow there is a crisis, i know only one thing: rates don’t have that much margin to go much lower, so in the best case they will stay the same. Unless the next crisis is a credit crisis and in that case, well, too bad for bonds.

The decorrelation between bonds and stocks might very well prove to be a myth. it’s not because it worked in 2008 (when rates were much higher) that it will work again.

By the way, what kind of bonds? Corporate? Government?

Just put the money on a bank account. So instead of having 80% stocks et 20% bonds, you can have 90% stocks and 10% cash. The risk return would be the same. (I have made up the numbers)

Timing the market is never a good idea

If you invest in stocks, you won’t lose money due to inflation.

For the core portfolio, so a mid-long term investment, I always think the currency contribution should be minimized, I just dont like currency fluctations to affect the investment. There is also another, a bit older I think, Vanguard paper that says the fixed-income/bond allocation should be hedged, whereas the equity allocation can be left unhedged.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.