The benefit and a disadvantage of corporate bonds ETFs, I think, is the fact that they don’t mature. With individual bonds or medium term notes I can fix duration and the nominal yield at purchase. What to do with a corporate bonds ETF I don’t know. Rebalance? The correlation with stocks is too high. Accumulate for a long term investments? Stocks have a better return long term.

The fact that they don’t mature is a general feature of bond ETF if I’m not mistaken (except for funds with a fixed maturity date). However, for rebalancing and volatility reduction purposes, I don’t see this as a problem.

I see the benefit of a known maturity date mostly where one has a fixed known date, where a predetermined amount of money has to be in cash. This is not exactly rebalancing and volatility reduction of a fund where the planned withdrawal date is far away, like for most retirement funds. Even here, volatility reduction is mostly done for unforeseen events requiring an early (partial) withdrawal. (or if you can’t mentally hold out too much volatility in your portfolio)

Ben Felix made a video about bonds funds and if I understood it correctly, a bond with fixed maturity is not really better than a bond fund with the same average maturity. It’s merely an accounting trick if one skips the reevaluation of a bond if interest rates change, since this bond couldn’t be sold at this price if required.

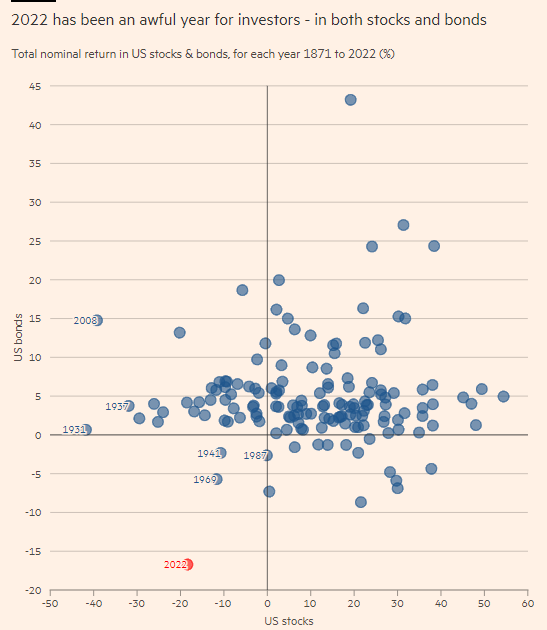

Do you have any further reading material about this and how large the difference in correlation between corporate and government bonds to equity is? I know that gov bonds had negative correlation in the last ~20 years, but this was not a given in the past, especially in inflationary environment, the correlation was positive

It’s not a problem by itself. But corporate bonds ETFs are not effective diversifiers for stocks and you can’t even use them as a replacement of a fixed term deposit. From the portfolio construction point of view, a corporate bonds ETF is more or less equivalent to 30-50% stocks + cash.

Concerning specifically this fund, I do following:

Go to investing.com

Download historical fata for the fund of interest and something for comparison, for example CHSPI (also traded in CHF). Or SIX also provides historical values of indices.

Calculate math characteristics, here is an example:

And if you do it, I would do the same for 3 Swiss governmental bonds ETFs originally in question. Otherwise SIX has also some indices for bonds.

I have forgotten that it is possible to calculate correlation coefficients with TradingView. I don’t understand completely how it is done, but here are some quick results for comparison:

Correlation coefficient over 25 days, long term average,

VT in CHF with

CHCORP 0.05

CSBGC0 -0.08

CSBGC3 -0.13

The fact that they don’t mature isn’t unique to bond ETFs, it’s unique to funds in general. The reason is that you own shares in a fund. You do not own the underlying assets.

The same holds true for ETFs which invest in futures, life settlements, and other investments with limited terms. The underlying assets mature, but the fund keeps right on going.

Personally I don’t see too much point to using bond ETFs. For stocks, ETFs make a lot of sense because stock prices fluctuate so you want a broad diversification to keep things balanced, and the potential upside is high in relation to the cost of using a fund. But with bonds, the yields are fixed and relatively modest, so any TER is just negating from the interest you earn. To me it makes more sense to buy bonds directly.

A possible argument for a bond ETF is if you use an accreting ETF so that you make a (tax-free) capital gain instead of getting (taxable) interest.

If you want corporate (or other non-government) bonds, you definitely want diversification. Buying many CHF bonds directly is likely much more expensive (and cumbersome).

If you’re happy just owning Swiss gov bonds, direct ownership may make sense, especially as it seems there is only roughly one ISIN per maturity year. If you have a broker with reasonable bond transaction fees, this may be cheaper than the typical 0.15% TER + ETF transaction cost.

YTM for ~5 year Swiss gov bonds: 0.93%

YTM for ~3 year SBI AAA-AA: 1.33%

YTM for ~5 year SBI AAA-AA: 1.42%

YTM for ~3 year SBI AAA-BBB: 1.57%

YTM for ~5 year SBI AAA-BBB: 1.57%

I can understand diversification against the risk of a company becoming insolvent (that risk would be identical for the company’s stock). But if you spread your capital over say, 100 different bonds in top-rated companies, that’s a pretty good diversification.

Diversification for the purpose of balancing price fluctuations, which is arguably the main reason for mass diversification in stock investments, doesn’t apply.

I’m sure there are use cases where an ETF can make sense for bond investments, like the tax-related use case I mentioned above. Another use case may be if the brokerage fees for buying 100 bonds would be higher than the cumulative cost of buying ETF shares and paying the TER over your investment term. Another one might be if you want to invest in bonds which you can’t buy directly (in specific markets, for example).

But on the whole, I feel ETFs don’t offer as much added value over direct inverstments in bonds as they do in stocks.

Buying 100 bonds à CHF 1000 at Swissquote would cost CHF 2’500 in fees, i.e. 2.5% (+ buy-sell spread). I don’t know whether there are any fees when a bond matures. On the other hand I can trade a bond index fund for CHF 9 + a load fee of 0.25-0.35% + about 0.15% TER p.a.

At Flowbank it would be even more expensive with a CHF 50 minimum per transaction. At IBKR I don’t see Swiss bond commissions.

However, even if the overall fees were comparable, I’d probably still buy a bond index fund instead of manually buying 100 individual bonds. Don’t forget that you might have to keep track of the credit rating if you don’t want to hold junk bonds. Way too much effort for maybe 0.1% p.a. of the bond part of the portfolio.

I might feel different if it’s just about a few Swiss gov bonds. However, for corporate bonds, I think index funds make more sense for most people.

I chose Swissquote in the end. 0.1% per year on 1 million hurts, but it’s basically the only Swiss broker that accepts corporate clients and where you can trade bonds. Contacted a few of them (cash.ch, PostFinance) and most do not accept corporate clients. Kassenobligationen are also somewhat problematic, Cembra for instance only issues them above 1 million for corporations. This defeats the purpose a bit, as you lose the protection on 90% and can just buy the Cembra bond directly (with a higher YTM) if you want to take on the risk.

In terms of positions, I chose individual bonds in different sectors (banking, insurance, industry) where the duration is suitable for me.

If you can share, curious how many separate corporates you split it across considering credit risk and how far out of a ladder you built etc. Interested to do similar to pre-fund some chunky annuity flows over the next 10 years or so with a reasonable return and without the interest rate risk.

Sure, I can share some of my thoughts and positions here with the caveat that I’m not a fixed income expert:

<2 years: Swiss bonds with a duration of less than 2 years do not make sense in my opinion because the transaction costs are very high (for 100k, 190 Fr. + 75 Fr. = 265 Fr. at SwissQuote, so 0.265%). I am currently considering a money market fund (https://products.swisscanto.com/products/product/LU0141249424) that is tradable on IBKR.

2 and 8 years: I currently hold individual bonds of Raiffeisen, Swiss Life, OC Oerlikon, Pfandbriefe, BLKB, some cities/cantons, Syngenta, Apple, Coop, Kühne & Nagel. I try to distribute the durations pretty well, but they are not perfect. Something I also noticed is that liquidity (on SIX) for many bonds is very low (compared to e.g. when I buy Treasuries on IBKR), so be prepared to spend some time looking at order books, posting bids that may or may not get filled, and looking for “good offers”.

more than 8 years: iShares Core CHF Corporate Bond I understand your concerns regarding the interest rate risk, but for a bond ETF the current YTM is guaranteed (under some assumptions that may not hold 100% in practice) if you hold it for 2 * duration - 1 (see https://www.etf.com/sections/etf-strategist-corner/how-predict-bond-etf-returns). So I treat such a bond ETF (which offers great diversification with a relatively low TER) mentally similarly to a basket of individual bonds with more than 8 years. I also found it interesting to perform a few simulations here: Bond ETF Calculator - Understand Impact Of Rising Interest Rates Even if you simulate extreme changes to the interest rate, it does not take too long for the ETF to recover.

Super useful thanks!

Does SQ allow you to trade bonds online, mine says to call their desk?

I was listening to a super interesting podcast with Blackrock’s head of fixed, Rick Rieder one thing he mentioned was BBB rated companies were often a better risk than single A rated from a risk point of view as they were generally working hard to get A rated versus the A rated who were complacent. Im paraphrasing, but you get the drift.

I’ve been screening bonds for the right mix of duration, yield, risk, liquidity and spread etc and am about to start buying some bonds. Using a combination of the SIX screener and Swissquote.

The Swissquote interface is pretty lame and and unhelpful. Im not sure I understand the order books versus the last traded prices. Firstly, there are the “cheeky” asks and bids waiting for someone to do a naive “at market” trade. Then often there is a last trade price with a recent timestamp consistent with the highest bid price or a few bips cheaper. But then you look at the transactions page and you cant find any trade.

I guess I just need to get stuck in with a couple of limit orders that give me an acceptable YTM at bids that have a chance of being filled.

DEGIRO

this two are the best broker for CHF corporate bonds available in switzerland for more information you search on internet there you will get wide variety of option according to your location

This was all super useful feedback. Over the last week I purchased 8 CHF bonds maturity between 2025 and 2032 and by favouring lower coupons have locked in a net of taxation (5% blended) and fees (0.25% all-in) ytm of 2.4%, duration 5.7 years, BBB+ weighted rating (nothing below BBB). I will buy a further 3 “ladders” of 8 bonds trying to have one maturing per quarter give or take, with a target of net ytm of 2.2% but blended rating closer to A-.

This will mean my “worst case” living expenses during first 10 years of FIRE are locked at above my target return and I should not need to touch any volatile equities, equity or bond ETF during dips for more than 10 years, which is the major risk to any drawdown plan of (hopefully) 40+ years.

I found this site quite useful for CHF domestic issuers ratings, also the default risk attached to their ratings over the last 20 years or so, thought the past is not guide to the future fedafin: fedafin AG

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.