Huh. Interest rates are going up, neobanks start to reinvent traditional banking…

1 Like

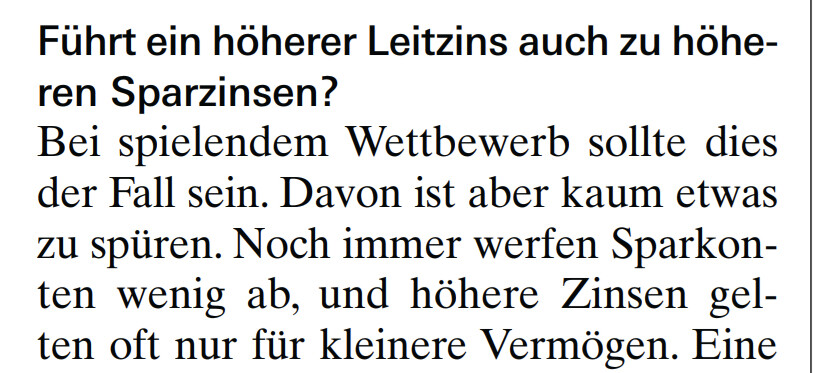

My Mac translated it for us non German speaking mustachians ![]()

Now we are considering giving you the opportunity to receive even more interest in the neon app.

We imagine this as follows: You could move as much money as you want to a special space. There, your money would then be blocked for a certain period of time, during which you could not use it. As soon as the time period is over, you could use your money again including the earned interest or invest again in the special space and earn even more interest.

In order to find out whether such an offer is of interest to our customers, we would therefore like to ask you:

Would you be interested in an offer in which you would invest your money for 1 month and get 1.1% interest for the year?

You could invest as much money as you want - there would be no upper limit. Your money would be blocked for 1 month at a time. After that, you could use it again including proportional interest (or leave it in the special space for another month, and so on…).

1 Like

It’s beautiful to look at. All power to the people ![]()

I didn’t get this email. Is it limited to users who have been with neon for longer?

2 Likes

I don‘t know. So far it was just a survey. I signaled them my interest. Let‘s see, maybe they will indeed implement it, fingers crossed.

Even the most generous banks are still stingy compared to the SNB, when it comes to savings accounts.

The SNB key interest rate is now going up to 1.75% p.a.

1 Like

We need to start a petition so that people can open savings accounts directly at the SNB. What “service” are banks charging 1% plus deposit fees for?

1 Like

Nothing out of the ordinary IMHO. Or did banks start charging negative interest immediately when interest went negative? I don’t think so.

This is not SNBs job and should never be.

2 Likes

To be fair there’s some debate over narrow banking and splitting lending to different actors. Things would look fairly different though ![]()

2 Likes

Hi all, since the EURO is very attractive against the CHF and I know my longer term needs will be in EUROS, I have converted a big chunk of my savings to EUROs and put them in IBKR MMF at a 2.63% interest rate. In case this helps you!

2 Likes

No surprise, from 1.07 YUH increases their interest rate to 1% on the account balance up to 25k. And 0.75% for 25-100k.

2 Likes

Savings accounts generally take time to adjust. That makes sense because banks must balance out old low-interest business (e.g. negative interest).

Medium-term notes and fixed deposit accounts react more quickly. Currently, the highest-yield 10-year medium-term notes yield 1.85% p.a. So just over the key interest rate.

100% agree. Why do I have to pay a bank intermediary? Where’s the law that says the people are obliged to subsidize the banking industry? An industry where there’s hardly any competition? This is from an NZZ article:

If people were able to deposit directly at the National Bank, there would not be any other banks. A bank that prints its own money and can’t go bankrupt would kill the market. Welcome to Communism.

Also, savings accounts hardly ever paid real positive rates historically, and after tax it was almost always a losing game.

There is competition, we have almost 300 banks in Switzerland, and a sizeable chunk of these are retail banks.

But as long as not enough people are shopping for better offers, there is little incentive to offer better rates. Lazy consumers mean high prices.

So, if you want a better rate, go shopping for it. It’s a market, they won’t give it to you for free.

Narrow banking doesn’t necessarily mean depositing directly. A narrow bank would have ~all its assets at the central bank, but they might still “skim” something.

And bank would still compete on which additional services they provide (e-banking, investment advice, cards, etc.) as well as how much they skim from the central bank rate.

But it removes the time component of the historical banking business (borrow short and lend long) to become a borrow short and lend short. Different actors would have to deal with the lend long part (i.e. banks wouldn’t really issue mortgages).

Some people think this could be “credit institutions” and the capital for those would be provided by investors rather than bank deposits. It’s unclear how stable that would be (will the investor flee as soon as it looks a bit risky?), or whether enough capital will be provided for having a healthy economy (e.g. need to ensure that someone will fund SME, etc.).

2 Likes

To be fair, banking is super sticky (the barrier to switch is pretty high, nobody wants to deal with opening an account every year).

Maybe there should be regulated MMFs with similar deposit protection as banks, that would solve the problem.

2 Likes

True. Also, from a bank’s perspective it may not make much sense to tease fickle customers with a high rate only to see them jump ship at a slightly better offer elsewhere.

From a regulatory perspective, the thing that would significantly improve competition is if there were a portability of bank accounts like there is for mobile phone numbers.

My idea would be to switch the account, but all your standing orders etc and incoming payments stay the same. I think they have or plan something like that in the UK and EU.

3 Likes

With ebill you solve part of that problem

4 Likes

This exactly. Having a bank account is a basic need to be a functional member of society, but the banks are ripping off the customers left and right. No, you can’t “shop around”, if all your salary payments, bills, tax refunds, credit cards etc etc. are linked to one account. A 1% margin of profit while we still have negative real interest and you need to pay taxes on the interest anyways means that the “little man” is getting slowly expropriated.

It’s almost as bad as the 2nd pillar PK situation. Havingcompletely powerless customers is never a good thing.

1 Like

How much did you complain when the banks didn’t apply negative interests rate for years? They have more inertia at least partly for good reason (balance sheet, which does provide a service to society by allowing more ventures to be started with their lending business).

There’s not much forcing you to keep the minimum at the bank and putting the rest in timed deposit or MMFs (which aren’t that far from the risk free rate, though MMFs aren’t as risk free).