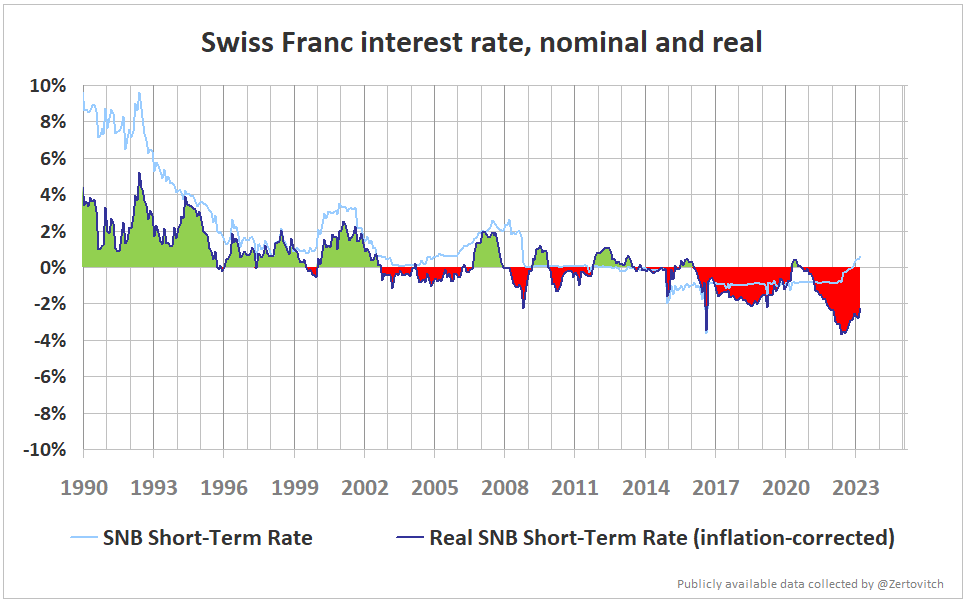

Yes, and in the long run, holding cash is a loser’s game. It’ll bleed value constantly, no matter the nominal interest rate. Just compare what a Swiss Frank got you 50 years ago, and what it gets you now. Also, we only get the shitty interest deals banks are willing to offer us, while they have access to higher rates.

Gold’s actually held up far better with inflation, but I guess it’s too volatile to hold as an emergency fund instead of cash

The fact that the inflation measure is backwards-looking is a very interesting point.

Let’s see how it looks like when you compensate for that by shifting the CPI data one year back:

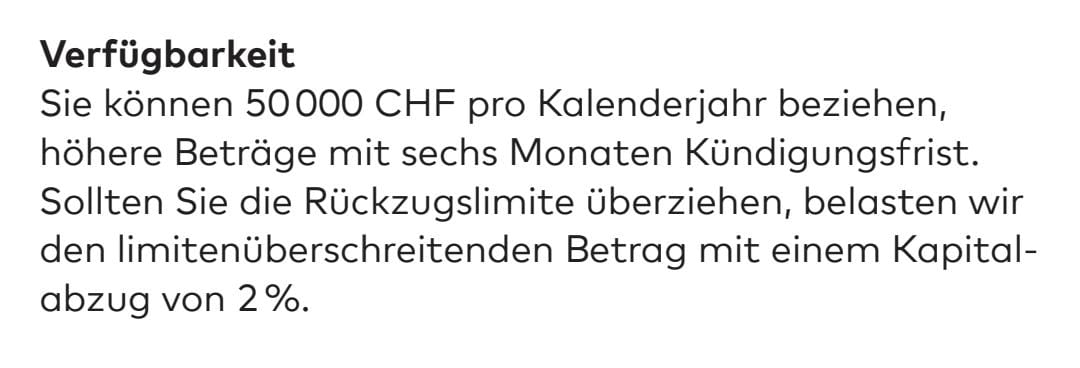

“Rückzüge: CHF 10 000.00 pro Jahr frei, darüber frühestens kündbar auf 1. März 2024 mit einer Kündigungsfrist von sechs Monaten.” The way I understand it is that is only for amounts above CHF 10’000.00. For amounts below there is no restrictions. This is at least how I understand this sentence.

I am still not sure I fully understand, my German seems not to be up to par (Vorzugsgebuhr of 2% is confusing me, in combination with withdrawal limits they mention)

If I pay in 20k

And want to withdraw e.g. 10k after 3-6 months

It’s still within the limit which doesn’t need a notice period (up to 20k with WIR)

Do I still need to pay any “early withdrawal” fees?

But if I want to withdraw 10k - which is within/below their “no X month notice required” limit (20k WIR / 50k Cler) - I don’t read it that the penalty fee applies.

I interpret the wording that the 2% penalty is only applied to amounts over the allowed limit (Rückzugslimite).

E.g. (for Cler) If I pull out 60k without notice - I pay 2% fee on the 10k which are above 50k (allowed without 6m notice).

If I pull out only 20k - no fee.

Hello guys, for your information, moneyland has recently published, with the latest news available online which is the best saving account to park some cash: Compte d'épargne: comparatif - moneyland.ch

I’ve discovered a lot of new bank account with this saving account comparison.

The Bank Cler Savings Account Plus is integrated into the comparison. The bonus 1% is calculated based on projected deposits.

The WIR Bank’s Savings Account Plus is a temporary promotion (valid till next March), which is converted into a regular savings account after that. So not really a stand-alone product. It’s an excellent offer for the moment, in any case.

What is interesting with the WIR bank are their general terms and conditions. Among other things A1.3 says: ‘Der Kunde verzichtet in vollem Umfang auf den Schutz des Bankkundengeheimnisses’. This means literally that Wir Bank doesn’t follow the Bankkundengeheimnis.

It’s not that I want to hide something, but just interesting point in their terms and condition…

The WIR Bank was one of the first Swiss banks to contractually bypass bank customer secrecy laws. Several more have done so in the meantime.

It’s worth noting though, that similar clauses are found in the online banking and mobile banking contracts of many/most banks, and apply when you agree to use those services. What’s possibly more concerning though, are the clauses in online and mobile banking contracts by which you waive the bank’s liability for losses. But that too is pretty much standard.

Yeah, Bank-client confidentiality is more and more being waived through contractual clauses in the AGB (Allgemeine Geschaeftsbedingungen, “fineprint”). To my knowledge there is however no confirmation through civil court proceedings/judgments whether this practice is (removing bank-client confidentiality through means of AGB) is legal or would be upheld by courts. It’s important to read the fineprint .

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.