Bank Cler offers now a savingsaccount within zak with 1.3%.

10’000 can be pulled without notice.

Notice period is 3 months for >10‘000.

If you want a referalcode, pm me.

Bank Cler offers now a savingsaccount within zak with 1.3%.

10’000 can be pulled without notice.

Notice period is 3 months for >10‘000.

If you want a referalcode, pm me.

I found @kart0ffel’s overview quite handy so I took the liberty to re-create one with the latest numbers I could gather. Hope it helps!

Feel free to let me know in case you notice some evolution or mistake, so I can update it

Cheers

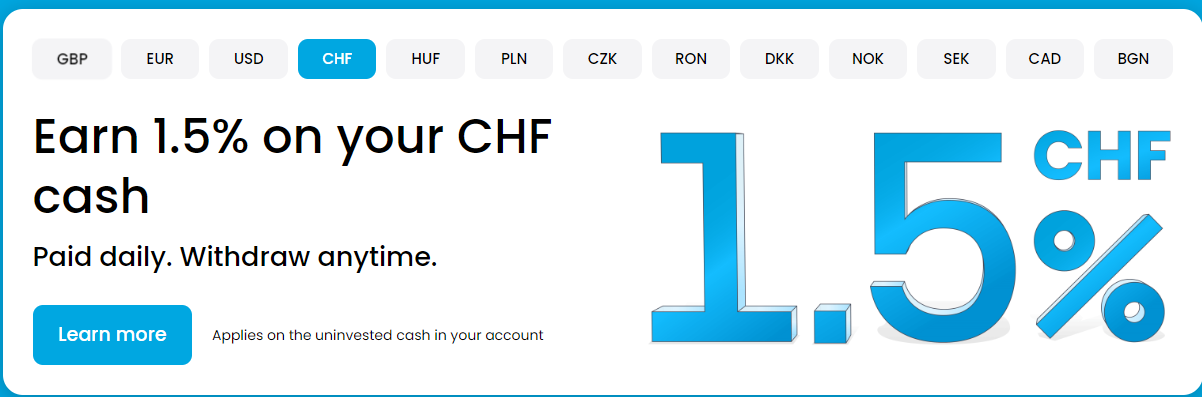

Trading212 (https://www.trading212.com/interest-on-cash) currently offers 1.5% interest on CHF, paid out daily. It seems, that the money is invested in Qualified Money Market Funds. So not actually a savings account.

Thanks for the summary! What do yo mean by “NA” by the way? There is none or the information is not available?

Now if someone can chip in on a concern of mine: I am a little wary of placing my money in these accounts because of how strict the withdrawal can be. As we’ve seen in the past month or so, most banks have lowered the interest rates. What happens if I placed a huge sum at Zak or Cembra for example and then they lower their interest rates even further? That would mean I cannot fully move my money into another place before several years? Is this the risk involved?

Clearly not years, but larger sums might need a few months notice (as listed above).

Yes it is.

Caisse d’épargne d Aubonne offer 2% but the withdrawal notice period is 12m.

As you said,

one must be aware of the withdrawal restrictions and plan accordingly.

Hence, one should distribute his savings among several “high” interest accounts to mitigate the liquidity risk (or trade interest for a higher degree of freedom).

Ah this solution might be interesting. Divide into several accounts.

If you are searching for full flexibility (no notice period, no withdrawal limit) and decent offering, there are basically three options:

My two cents:

When storing emergency fund, I need full and anytime access. This is why I am absolutely willing to take a drawback, when comparing with Caisse d’épargne d’Aubonne or another provider. A notice period of 3m or more is absolutely not suitable for me or an emergency fund.

What’s the general strategy for the cash management by people on this group?

Move cash around different banks to maximise interest rates. This would require multiple Bank accounts

Find reasonable providers and stick to them.

Use money market funds (I personally cannot find good combination of low custody fees, low TER and good Yield)

Looking at posts on this thread, I am getting an impression that there is tendency to shop around continuously….

In addition, I find it a bit confusing. If 100,000 CHF is guaranteed by Esuisse guarantee, they why some providers need to provide much higher interests (like Cembra) to keep deposits in their custody. What is the problem with Cembra that they need to offer higher interests ?

I have 3 Levels for my cash:

33% disponible now

33% disponible in max 3 Months

33% disponible in max 6 Months

Rules:

No more than 100k per Bank

Emergencyfund is separate

No limited promotions → to much hassle for me.

I have Willbe and Cembra on top of PF, IBKR an ZAK which I use anyway.

I can’t answer for others, but for me, it’s not having a lot of cash. Just enough to cover any bills.

The average account balance is for convenience, not an asset I expect returns on.

My house bank has withdrawal limits and penalties on the saving account, but upon asking about that said it won’t be enforced. Yet even the saving account interest will not show up in a list of best interest rates.

NA stands for “Not Applicable”: there are no restriction. I also don’t like being limited, so it’s out of question for me to go with anything that has strong restriction. That’s why I added it and color coded this way; usually, the more interesting rates are coming along significant withdrawal restrictions

I have a low amount on my private account (always ca. CHF 1’000), since I am paying everything with credit cards and therefore do not need a large amount on my private account. Some CHF to twint here and there. This is with ZKB and I do not intent to change the bank, since the e-banking is top notch, never had issues with them and they provide a free banking account incl. free debit card and the shared account with my gf is with ZKB as well.

At Neon I have a very low amount as well (ca. CHF 200-500), only used for FX payments. Prior holidays I transfer some more cash to Neon. Also no intention to change to another provider. Have been at Revolut, but I feel more comfortable with a Swiss bank behind it.

With Interactive Brokers there are only some leftovers from converting money into USD to buy securities. Always < CHF 100. Beside the UK-entity, I have also an US-account with them. No intention to move to another provider, but I can imagine to have a Swiss provider additionally, where I move my assets (e.g. Saxo). So, buying at IB, but transferring all CHF 250k or so to Saxo. Call me paranoid.

My biggest cash amount - my emergency amount - is at WillBe, currently ca. CHF 35k and rising. I am aiming to have a solid amount (ca. CHF 50-100k) always liquid. It may be a lot, but I feel safest and I am willing to take this opportunity costs.

At the moment, WillBe has for me the best conditions to keep my money there. But I am pretty illoyal toward banks and I am ready to move to another bank if there are sustainable better conditions. I am not changing to another bank if I expect them to change the T&C soon.

I follow the identical rules as @Balaclava , emergency fund must be a different and reliable institution.

Also very situation specific, but for what I’m concerned:

Hence I decided to go for one neon account for daily use and one Radicant account for cash. I chose Radicant over WiLLBe because of the Visa card they provide, which I can use in case there is any issue with the Neon Mastercard. I could add another account for better returns on a portion of my money, but I’m too lazy for that (cf. point #3)

EDIT: I’m actually in the process of doing that and get away from PostFinance, so that strategy might still evolve depending on how the conversation go ![]()

For me, cash is high liquidity and low returns. I don’t need a lot of high liquidity (but I do need some) so the amount of interest that could be gained by shopping around is, in my opinion, not worth the time I would spend doing so.

So, option 2: find reasonable providers and stick to them.

I would shop around for medium term notes, which is no liquidity, acceptable risk-free nominal returns in my mindframe.

I tried it, and seems to be authentic

Same for me.

If my 10K emergency cash gets 1 or 1.3% interest a year is in the grand scheme of things pretty meaningless to think about. That‘s 30 bucks a year.

If I spend even half an hour setting up a new account, that‘s already too much cost compared to what my time is worth.

Other than that, Avadis has a solid money market fund option.

0.14% TER. Problem is that you can only get your money once month.

A post was merged into an existing topic: CHF Money market funds [2023]

That was a great hint, thanks a bunch ![]()

We’re currently looking for an additional bank to keep term deposits with. Seems the range will be around 1.2% for 1mo duration (we’d like to roll), have you seen any higher offers recently?