when u have C permit you can’t be out of CH longer than 6 months without losing your permit.

but once u get the Swiss citizenship, how many months should u be in CH for keeping your tax resident in CH?

I thought it was 6 months, but i don’t remember where I read time ago it was just 3 month the time requirement for being a CH tax resident. So u might split a year like 4.5 months in one country, 4.5 month in another country and 3 months in CH, then you would be CH tax resident.

I know the are not the same, but how many months do u need to be living in CH in a year to be consider tax resident in CH? just 3 months? or 6 months? like in other many countries

so confusing, i guess most of the countries is 6 months

so if u work just one month (30 days), let say January, in CH and move away to another country you will be for that year tax resident in CH and in the other country. Prob you are gonna need to deal with double taxation agreements. So prob the best time to leave CH is end of year, and less hassle.

without Swiss citizenship u can’t get in and out of the country so easily

so lets assume u have the CH citizenship so u can get in CH without dealing with permits

and assuming country A and country B have 6 month as minimal period for being consider tax resident there

also assuming u can show that your center of live is not in country A nor in B,

and assuming u are already FIREd

could u stay 5 months in country A, 4 months in country B and 3 months in CH and you would be tax resident just in CH?

also u would have to pay the health insurance just for this 3 months, right?

That sounds risky, there’s been cases where the tax office would decide that you’re only temporarily outside and that you were a tax resident the whole time.

(edit: actually it sounds like you describe, if you don’t intend to permanently settle elsewhere, CH is likely to consider you a tax resident, but that doesn’t really mean that the country A and B would treat you this way )

It depends. If you spend the longest part of the year in another country, that country may consider you a tax resident - even when it’s less than half a year.

No. „Der einmal begründete Wohnsitz einer Person bleibt bestehen bis zum Erwerbe eines neuen Wohnsitzes“ (Art. 23 ZGB) - both of which, if I understood you correctly, you want to avoid.

I have a hunch that this thread may rather sooner than later come down to the oh-so-popular question of theory vs. enforcement and practice („But how are they going to know/verify…?“)

if u have the Swiss citizenship, and u are FIREd living in another EU country

u could come to CH every few years just 3 months, stay in a kind of AirBnb, rebalance your portfolio, you will not pay capital-gain taxes as usual in CH. Then that year u could travel a bit more, so u don’t need to spend most of the months in that EU country that year, and afterwards keep your live in that EU country.

The risk is you trigger the residency criteria in both countries and you end up being asked to pay tax in each which is something you generally want to avoid, and then trying to claim back via Dual Tax Agreements.

In your example. I doubt it will fly you tell the EU country you are not a resident there because you rented an Airbnb for Switzerland for 3 months

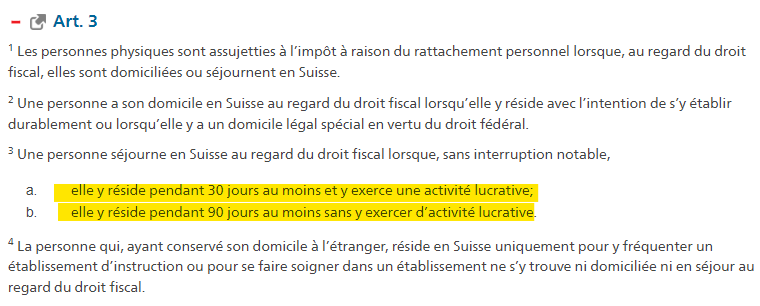

Tax residence is not based solely on the number of days spent in the country in question. This is one of the conditions for being taxable in Switzerland.

An individual’s tax domicile is not based solely on the number of days spent there. There are much broader and more complex conditions, precisely in order to prevent ill-intentioned people from taking advantage of the famous “number of days of residence”.

The conditions that come into play are as follows:

The place where the person resides with the intention of settling there permanently

If the person lives alternately in two or more places, in the place with which he has the strongest ties (place of the centre of vital interests).

The centre of vital interests is determined on the basis of all the objective circumstances and realities that make it possible to establish the taxpayer’s personal and economic interests. The wishes expressed by the taxpayer or his emotional preferences are not taken into account. Nor does the centre of vital interests depend on formal indications such as the filing of papers, registration in a municipality or notification of departure; to this extent, it is not possible to freely choose one’s tax domicile.

Unlike civil law, tax law distinguishes between several types of domicile.

For tax purposes, a person may have several domiciles:

A principal place of residence, which is the place where the taxpayer’s vital interests are centred and which is the basis of the taxpayer’s personal connection with that place, i.e. unlimited tax liability ;

A secondary or special domicile, which is based on an economic connection of the taxpayer in a place that is not his main domicile and thus creates limited tax liability in that other place;

And, exceptionally, an alternating domicile, i.e. a main tax domicile allocated to two municipalities for taxation purposes.

I would recommend you to look about your tax residence with a lawyer or a tax adviser in order to know where you have to pay your taxes. Moreover, and this is my point of view, it is better not to try to have a sophiscated plan in this matter, you will end up paying your tax two, three times and struggle with different tax procedure. But if you have the money and the time to do so…

There you go, You’re „living in another EU country“, while going on holidays to Switzerland for tax evasion purposes. You said it yourself. If you spend the longest part of the year in that country you „live“ in, you will probably be tax resident. At least no one here will (or should) be telling you, you’re not.

Well, u mentioned just 1st part of my paragraph. Later I wrote going rest of the year to other countries to avoid spend the longest part of the year in that EU country.

Then that year u could travel a bit more, so u don’t need to spend most of the months in that EU country that year, and afterwards keep your live in that EU country.

In that scenario I would not like to pay taxes in 2, 3… countries, and have a lot of paperwork with tax authorities.

But if u don’t have family, you do not own a house and u are FIREd (it is not my case now) your ties with the countries are very weak.

I think once u are FIREd make sense to every let’s say 5 years move to no capital-gain tax country (as CH) and sell/rebuy your ETFs to reduce taxes.

Is there a way to do that legally? maybe move into that country for a while, but how long means that? Maybe CH is not the best country to achieve that.

I learnt about this a few weeks ago. The country I checked had an exit tax when your wealth is over 4M EUR, but it was a surprised I didn’t know that exists. 4M is quite high anyway for me, at that level of wealth prob there are other solutions more sophisticate as Trust…

In long term the impact of reducing your fund manage fee from 2% to 0.2% is huge. The impact of 20% or so of capital gain tax should be giant.

Of course - it‘s the one that feeds my argument. The question is: will a taxman think any different? Especially if you (re)turn up again in that country a few months later. With a drastically changed investment portfolio.

I think this can go multiple ways in practice. And I really do believe you can‘t and shouldn’t (legally) rely on and determine your tax obligations solely by the amount you spend anywhere.

Best case: you’re spending less than half a year in any given country - you may register with the authorities, deregister and just move on and nobody‘ll blink an eye. Congratulations! You may have attained perpetual traveller status and be considered tax-resident nowhere.

But wait! Your broker isn’t going to enter „resident nowhere“ in their systems. They‘ll ask you, they may ask for proof - they may have to, in case of doubt. And they will report to your purported country of residence. And you do have to keep them about any changes of residence

Side note: can you forget or lie to your broker? Of course. But that would the first small crack in your system if you want to play it legal.

With or without a CRS reporting to your country of residence, the Spanish taxman may or may not notice something untoward in your behaviour. He may ask himself: „Well, that person‘s lived here for five months - quite close to the duration we have to consider her/him tax-resident. Yet claims he/she is not. But turns up again a year later?“

At that point, you may attract closer scrutiny. While Spain seems to charge exit tax for holders of €4 million or more portfolio investments, there seems to be a lower threshold of only €1…million for company owners - this should be closer or below you net worth if you’re „FIREd“ - and suggest that they may in fact care about it and delve deeper even in your case.

Having realised a large capital gain abroad, let alone telling them “oh, but I’m Swiss and was in Switzerland for three months and realised my capital gains there”, I wouldn’t be surprised if it paints a clear target on your back at this point.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.