Hi there!

I was wondering what you guys use for cash deposits, preferrably in CHF.

As far as I can see, the options are still very limited.

Did you find any new offer on the market which is slightly more appealing?

What are your thoughts?

Cheers

Hi there!

I was wondering what you guys use for cash deposits, preferrably in CHF.

As far as I can see, the options are still very limited.

Did you find any new offer on the market which is slightly more appealing?

What are your thoughts?

Cheers

If you refer to interest rates, they cannot deviate much from the central bank’s interest rate (a banker will better explain to you by how much). Apart for a few basis points, it is not a free market.

Retail interest rates are so far disappointing, and I believe Yuh is the only one offering at least the CHF reference rate. I would expect this to improve only slowly, as no established player wants to give up margin.

You could buy short-term Swiss state bonds and hold to maturity with virtually no risk (e.g. this one if you are willing to bear the comparatively heavy tax on a 4% nominal yield).

Everything above that is reflecting of the also higher risk you would have to accept,

semi-interested in diversifying from cash in bank accounts to (short-term-)bonds (say max. 1 year) for my cash allocation.

do I understand correctly that:

pay Fr 101 now

hold till 11.2.2023 (3M)

get 100 + 4 back?

that’s a gain of 3, assuming a relatively high 33% tax rate on my income (for simplicity’s sake), the gain is 2, so my return is 2% for 3M, or 8% p.a. (after tax).

Why would such a low-risk investment pay such a high return?

and where could i actually buy these Obligationen?

are they available on Swissquote, for example?

seems yes. does anybody own anything like this? experiences?

does it cost Fr 9 (“flat rate”) to buy, at Swissquote, for example?

does selling at maturity cost anything, since that kind of transaction is often covered by the other party?

other costs would be the 0.1% Verwahrung?

anything else?

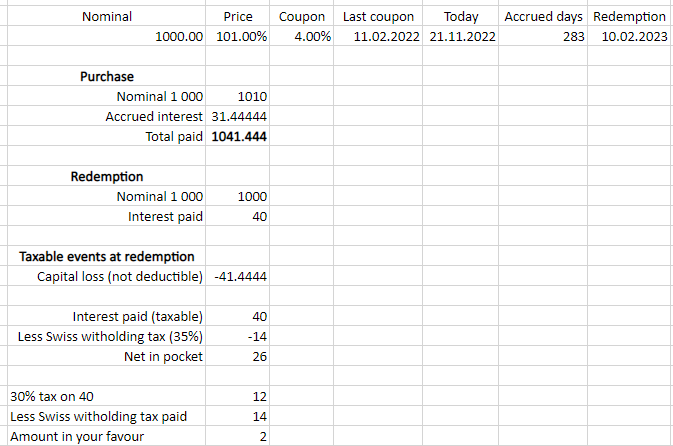

You will pay 33% taxes on 4 (the total interest) not 3.

A bond price is usually dirty, which means if you buy at a price of 101 you pay 101% of the nominal value + 101% of accrued interest.

So a you will pay 101% * (1000+ ~0.75*40) = 1040.30 CHF

You will get 1040 CHF in 3 months and pay 13.2 CHF in taxes.

I sometimes buy Bonds through Swissquote, but usually High Yield. The 9 CHF is a poster rate, effectively I calculate with 0.3% for 100k (and you’ll pay probably 0.6% or so for 10k). You don’t sell at maturity, it will be automatically settled without additional fees.

For the example Bond I linked if you pay 101% and have a 33% tax rate you’d be near to a 8% annual loss, not a 8% gain. For this to return 0.5% annualized you’d want to pay 99.50 CHF with a 25% tax rate. These extremely short durations typically don’t work retail because of the trading fees, but one or two years might work (or again, you slightly increase the risk, there is plenty between a Swiss state bond and the HY sector).

Spent half an hour looking into bonds, here are two examples with close to a one year maturity:

AMAG (CH0506071379) annualized return (to Oct 27, 2023) is 1.42%

JPM (CH0272024669) annualized return (to Dec 4, 2023) is 0.97%

This is assuming 0.3% trading cost and a 33% marginal tax rate, calculated at the most recent ask price.

Obviously this is no advice, and you should check and assess the associated risk / credit rating on those before investing.

All I am saying is that thanks to the recent interest rate increases, we have finally reached a market normalization again where there is an actual risk premium paid, and acceptable risk weighted returns above the reference rate are possible. This wasn’t the case for a very long time.

Well, that’s a bum deal. I’ll just leave the Nötli under my pillow then.

Thanks for your explanation though!

Thank you. ok, so similar to the trading fees for stocks, which are also in that range.

good to know, what to avoid and what to look out for. i had googled a bit,but strangely there is very little literature abour bonds/Obligationen. Most banks have only very general info to the topic IMO.

2y I could live with for a certain amount.

Ja well, that (the 1.42%) feels too little for the effort and higer risk. I appreciate you looking them up but will leave bonds until…

…yeah, waiting in that case, for better days.

In nominal terms it looks like a normalization, but in real terms, those yields are in the negative zone, even with a risk premium.

Yeap, I have a message to everyone who is glad to have some interest on your cash deposit: before SNB started to increase the interest rate, your 0 interest rate account was yielding 0.75% p.a. above the risk free rate for CHF. Now you have to try hard to get the risk free rate for CHF on a cash deposit.

Yes.

No, the interest is accrued on the value of principal, not on the traded value. Wouldn’t have much sense otherwise.

101% * 1000+ ~0.75 * 40 = 1040 ![]()

An interesting new place where to put your cash are credit unions (darlehenskasse). I’ve seen a couple of Building cooperatives offering 1% or more. The problem is that most of them offers it only for members. There is some exception I’ve heard, but atm I’ve found just one and it offers 0.5%

https://www.bg-gisa.ch/dienstleistungen#darlehenskasse

I am not saying the interest is calculated on the price of the bond, I am saying you pay 101% of the bond value. The bond value is 1030 with accrued interest, so you pay 101% of 1030 if I am not mistaken

101% of nominal value/par/principal + accrued interest = nominal value * coupon rate * days since the last payment / 360 or whatever

A post was merged into an existing topic: How to buy CHF bonds