I recently read this article on earlyretirementnow.com about the safe withdrawal rate once one reaches FIRE. They run numerous simulations and compare the rate of success based on safe withdrawal rate, time horizon and capital preservation/depletion.

From the article, here is how they define the last parameter:

capital preservation: target a certain minimum asset level (as % of the initial value) at the end of the retirement horizon. Under full capital preservation we’d aim to keep the real, inflation-adjusted value constant, by consuming “only” the capital gains, dividends, and interest over time, while keeping the principal (plus inflation-adjustment!) in place.

capital depletion: target a zero (or at least positive) final portfolio value, by consuming gains as well as principal over time

I wanted to know which approach on the forum were taking.

Capital Preservation - For my children

Capital Preservation - For other reason(s) than children

I voted for capital preservation, however found that there is a bit more depth between choosing simply preservation vs. depletion. So, if you allow me to add some unnecessary complexity to your simple question, this is how I approach it:

First, since the future market performance is unknowable it is not a given that there is such a thing as a safe withdrawal rate. Who knows, maybe we should store our wealth in gold bars under the mattress… We can however make a probabilistic argument based on past performance and maybe some best-guess predictions.

For my layman analysis, I attempted to calculate SWRs that will succeed at a certain probability based on past market performance. As success criteria I arbitrarily set a minimum capital of 250k CHF at age 90 (in real terms), and compute the number of historic months where retirement would meet this criteria. Being somewhat risk adverse I computed two SWRs that yield 95% & 99% probability of meeting this success criteria, again based on past performance and for my specific circumstances.

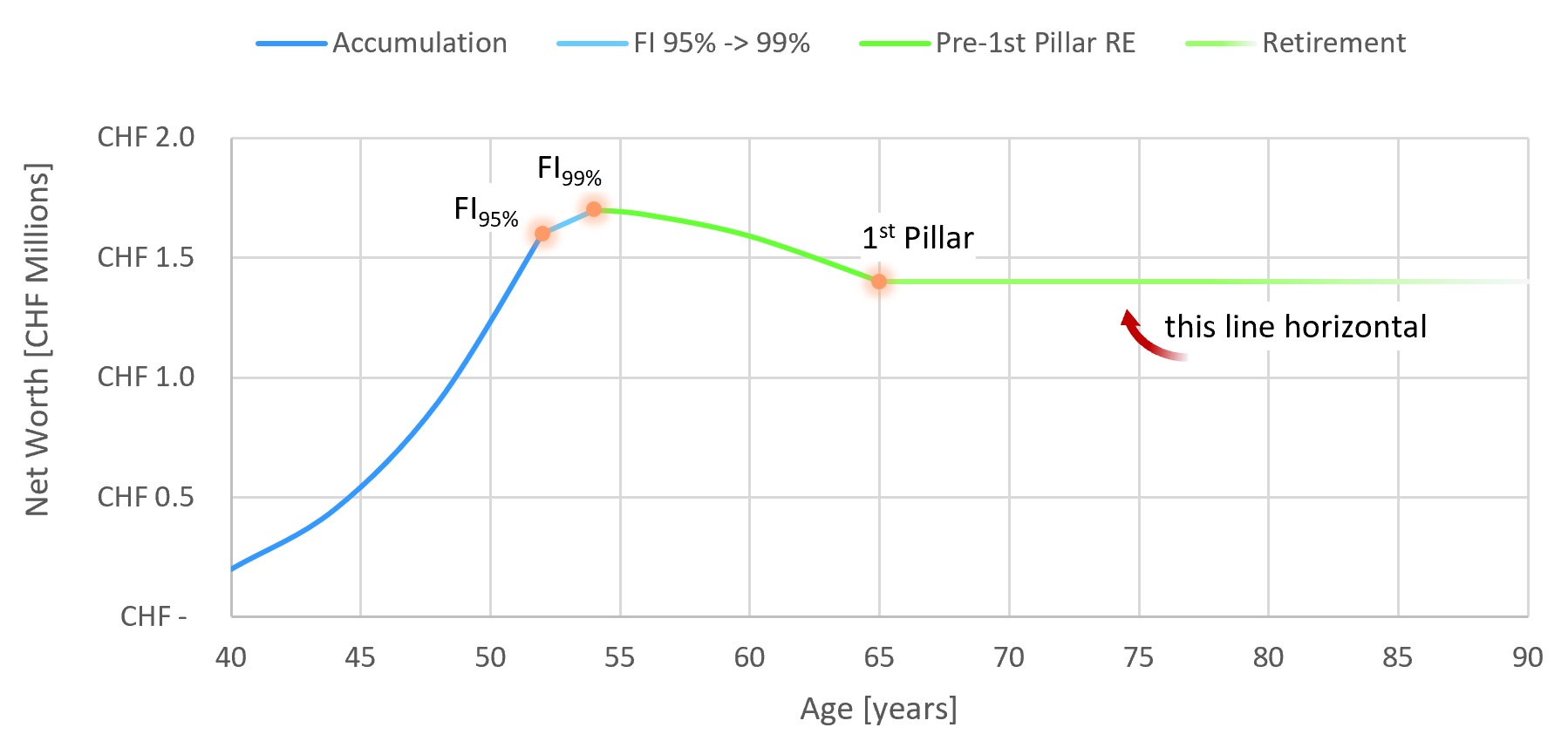

While keeping an eye on political developments, I currently still assume that there will be a 1st pillar pension waiting for me. With this in mind, I plot four phases shown below.

1: Accumulation, I hope I will do better than that but we will see… So far I’m roughly on that curve.

2: After reaching FI with 95% probability (maybe) reduce work load / look for other activities, while staying economically relevant. Maintain some income & see which way the market goes. Probably increase bonds allocation.

3: Once reaching FI 99% (probably) retire, allowing some depletion until 1st pillar pension kicks in. Will need a hard look at how likely that 1st pillar will still be there, resp. how much…

4: Remaining capital & 1st pillar plotted as capital preservation, but this is against an assumed SWR.

So this is not precisely capital preservation, but it is a model that provides ~99% chance of avoiding disaster and based on the same numbers ~93% chance of preserving capital. Unless (shock!) the future turns out differently than the past…

Totally in line with what I’d like to do too…I’m probably later than you though based on the graph.

2 Questions: do you have a 2ieme Piller? If yes, did you take as capital at retirement or not?

This will be my next big challenge is setting how much capital of 2ieme to manage myself as lump sum and how much capital to leave as guaranteed income? Lots of details/restrictions to consider and the decision on preservation and depletion of overall capital could be easier in those different contexts.

I see your perspectives and I can’t disagree with that logic. One certainly can’t know when he will die and the capital preservation strategy has to have a higher success rate, the gap widening the longer one’s life extends. When I made this poll, I saw this preservation/depletion question as, in part, a philosophical one.

My question then is, by going with the preservation strategy, what will happen to your capital after you died? I divided the capital preservation in two because of course if you’ve got children it goes to them and you can easily convince yourself that all the time you spent working for that money you never used was worth it because it will help perpetuate your gene pool.

On the other hand, if you don’t have children or you don’t want them to receive hundreds of thousands of CHF for doing nothing, do you give it to charity? Do you simply count this money as a loss? In that case I would be troubled by the obsession of the FIRE community to stop working as fast as possible but then never using such a large sum of cash.

Am I the only one planning for “continuous capital growth” ?

All my life I spent well below my income, and growing wealth has been a goal. It would take a major psychological shift to change my goal to wealth preservation. Let alone to managed financial decline coming on top of the inveitable physical decline

As I am currently happy with my job I would rather delay the RE date a little

For me, the purpose of financial independance is to enjoy freedom and to grow influence in order to support the causes I want to prevail. In that prospect, I guess creating a fundation or giving to charities (depending on the amount) would be a fitting way to dispose of any extra wealth when I die. My children, if I have any, would get a good chunk of it too, though they’d have to grow a good piece of wealth on their own first as a character building experience.

Of course, targetting more safety in RE means sacrificing getting there quicker, so that extra safety bears a risk in and of itself, that is, sacrificing good years of life and enjoyable time in order to get it. I’m pretty far away from reaching the lowest of my FIRE numbers so my view has time to evolve until then.

That is an interesting point. We do not see a lot of people seeking “continuous capital growth” in the FIRE community.

I am interested about this goal? Can you explain what is the point of accumulating wealth if it is not to spend it (for yourself, for charity or for your children) at some point?

Yes I do, and I’m planning to take it out as lump sum and park it at VIAC / finpension. In fact it will have to be taken out if your RE age is below 58, although you could consider joining the “Fondation institution supplétive LPP / Stiftung Auffangeinrichtung BVG”. I’m not sure that this will be financially attractive.

If you will be over 58 at retirement you may consider of course to draw some as guaranteed income and reduce future volatility in your total net worth. Personally I instead plan to increase the bond / cash allocation towards RE (e.g. 60/40 or even 50/50), and after RE slowly reduce that again over time (to e.g. 80/20 once the 1st pillar kicks in) to have some hedge against sequence of returns.

This also allows market risk to increase while the risk of drastic changes to the 1st pillar before retirement reduces. As of today I’m not too confident that the 1st pillar will look the same once I get there. But the closer one gets, an at least partial exemption of big changes will be likely.

For the more philosophical side your question, I can, with close to 100% certainty, tell you this: I will not care much about what happens to the remaining capital once I’m dead. Only close to 100% certainty, just in case my epistemological model of the afterlife turns out to be disastrously wrong.

I do have a child, and it provides me some measure of comfort to know that the family is provided for if I would keel over tomorrow. And this without financing this years bonus of some insurance company. However since I fully intend to live until at least 110 years old, it doesn’t seem very meaningful to spend much thought on what my then 90 year old offspring is going to do with his inheritance…

What it does do though, is giving more options as life progresses. I don’t need to look at date X where the capital will be depleted. If markets do well I could possibly even adjust lifestyle upwards, without having to worry too much of being destitute one morning. And who knows what old age will bring, maybe sickness and disease, or maybe grandpa will bail out of the retirement home one day and develop an expensive drug habit…

I’m currently planning on reducing % rather than a full RE to allow me a transition over a few years, so 60-63 is my current goal (reducing % at 60-63 then RE at 63 instead of regular at 65-67).

With that in mind, how do I calculate how much to keep in pension as retirement salary and how much as lump sum capital at retirement when considering everything else? By then my 3a will be cashed out and either used for 2ieme buy back as top up before retirement (min 3 years before) or as top up to Fire Fund.

I’ve also checked and I’m allowed to request lump sum of 50% under 1.0mio in pension and 100% above 1.0mio. I can give more details as needed, but I started my pension at 25 and didn’t start FIRE until 40 unfortunately…so my pension is currently 2x my FIRE fund+3a combined (but I’m catching up )

In that context: wouldn’t it make sense to leave more than then minimum 500k as a fairly good salary of guaranteed income and use it as a bond allocation even in retirement? I currently also count AVS as bonus (who knows what it will look like), so I’m feeling that I want to consider my pension as my portfolio safety net of guaranteed income until I die. Maybe I should look at what my retirement salary needs to be for my mortgage and go from there?

Thoughts?

Edit: I kept this question in this thread since it will help me to determine how much “preservation” is needed depending on how much I keep in my pension…

My main reasons for not settling for capital preservation and preferring to work a while longer to be able to keep growing wealth are:

I am risk averse and a worrier

Human nature to want to continuously improve and not stagnate or decline

Keeping flexibility to upscale my lifestyle with luxuries that I don’t need now but I might value later. Example: would be nice to be able to fly business class to visit my kids when I am 90 and decrepit

Fear of losing status and feeling “poor” vs peers - I am a bit embarrassed about this one but I admit it

To give my kids a good start in adult life (plenty of pitfalls here)

Probably I have OMY (“One More Year”) syndrome and possibly I should start a thread about that…

p.s I over stated it when I stated growing wealth has been a goal “all my life”. What I meant is that about 14 years ago I made the decision to focus on growing my own wealth vs. progressing at work. Watching all my nice charts turn negative would be a psychological wrench! I suspect I may not be the only one

I actually think I may have misunderstood the original pool question since i answered based on “once retired”. For sure I’m the same as you mention in the meantime…I’d definitely rather work 3-5 years longer, reducing % perhaps, but ensuring no compromise on long term “FI” (above “RE”). Once I start to stop, would be hard to go back up if I miscalculate something - better to be sure ;).

If health and family allow it of course…priorities are clear there…strategies will evolve accordingly.

P.S. In terms of taking it with me or not: I would love to be able to spend (intelligently) but to have enough be able to give living donations to my kids while I’m around to enjoy their pleasure too…at least periodic contributions to their own FIRE funds…I’d much prefer managing as much as possible while I’m around than leaving a huge inheritance.

Interesting post. Giving your reasoning for continuous capital growth, why retire early at all? Do you just want to see your net worth grow, with no regards to the CHF amounts? To fulfill everything on that list there is not a better option than keep working, even after 65 years old if possible while investing the money you do not spend.

If you can acheive a spending rate of 2.5% of Net Wealth instead of 4%, it would not be necessary to work at all to fulfill the list, because the compounding effect is spectacular.

I use Portfolio Analyser Monte Carlo simulation with a pinch of salt but if you can achieve starting NW 3M USD and annual spending 2.5% (75k) , increasing with inflation, it predicts that after 30 years the ending NW 50th percentile value is $11m, inflation adjusted ($21m nominal). Almost 0% probablity of running out of money. Gets funny with a 40 or 50 year horizon …

Yes and no. My point here was that the strategy on “preservation vs depletion” could influence my consideration on when I decide to retire. But clear now, sorry for adding any confusion on that.

One reason is that we don’t know how long we will live. For all we know, there might be medical advances in the next 50 years that eradicate diseases such as cancer etc. and we end up living until 300!

Warning: the graph on the tumbnail of the video is clickbait. The video seems to be actually about retirees not allowing themselves to spend (which also means they don’t deplete their assets).

It doesn’t mean it’s not interesting but it’s a method I really dislike so wanted to point it out.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.