With a Swiss pension fund (unlike bonds), you also need to account for the tax (and taxable-income-related) savings when calculating returns.

Tax savings vary hugely depending on your family situation, the canton/municipality you live in, your income, etc. In my case there are also additional savings through benefits (scholarships, health insurance premium reductions, etc.) which are based on my taxable income. These are far more substantial than my actual income tax saving, generally in the tens of thousands of francs per year.

It’s important to calculate the real return based on your specific situation.

Many cantons have steep progressive rates, so after you reduce taxable beyond a certain level it is not worth going further as the tax savings are low. If you go really further, tax savings go negative if your marginal rate becomes less than the tax rate on withdrawal.

Nach dem Börsenboom zeigt sich eine riesige Kluft zwischen den Pensionskassen. Die Verzinsungen reichen von 1,5 bis 9 Prozent.

«2024 ist ein Glanzjahr für uns», sagt Laurent Schlaefli. Der Geschäftsführer der Pensionskasse Profond kann seinen Versicherten richtig viel Geld ausschütten: 8 Prozent beträgt die Zinsgutschrift für die Erwerbstätigen. Erst einmal, im Jahr 1997, war die Vergütung noch höher. …

Die grosszügige Ausschüttung kann sich Profond leisten, weil die Pensionskasse mit ihren 70 000 Versicherten an den Finanzmärkten eine Rendite von 9,6 Prozent erwirtschaftet hat. …Profond gehört zu jenen Kassen, die einen besonders hohen Anteil in Aktien und Immobilien investiert haben. Festverzinsliche Gelder machen bei ihr lediglich 14 Prozent des Portfolios aus.

Auch Pensionskassen mit weniger Aktien haben 2024 allerdings sehr gut verdient. Gemäss einer Schätzung der Beratungsfirma Complementa erreichte die durchschnittliche Rendite 7,6 Prozent. …

…Complementa-Chef Markus Wirth. Nach seiner Schätzung erhalten die Erwerbstätigen für 2024 eine durchschnittliche Verzinsung von knapp 4 Prozent – ein solcher Wert wurde in den letzten beiden Jahrzehnten nur einmal überboten.

Dabei zeigt sich jedoch eine enorme Kluft zwischen den verschiedenen Kassen: Zu den grössten Profiteuren zählen die Mitarbeitenden von UBS oder Sulzer, die eine Verzinsung von 9 Prozent erhalten. Auch die Migros-Angestellten gehören mit 7,5 Prozent zur Spitzengruppe. Auf der anderen Seite müssen sich die Bundesbeamten mit einer Zinsgutschrift von mageren 1,5 Prozent begnügen. Auch das Aargauer Staatspersonal erhält weniger als 2 Prozent.

…

Doch wie gut ist eine Pensionskasse wie Profond gegen einen erneuten Einbruch an den Finanzmärkten gewappnet? Die Bewertungen an den Aktienmärkten sind im historischen Vergleich hoch. Ausserdem tendieren die Zinsen der Schweizer Staatsanleihen wieder gegen null. Schlaefli gibt Entwarnung. Entscheidend sei der Kapitalfluss aus den laufenden Erträgen: «Wir müssen sicherstellen, dass die Einnahmen aus den Dividenden und den Immobilien die Rentenverpflichtungen decken können. Dies ist für die nächsten Jahre gewährleistet.» Nach seiner Überzeugung hätten auch andere Kassen das Potenzial, höhere Renditen zu erzielen. Eine übertrieben vorsichtige Anlagepolitik sei nicht im Interesse der Versicherten.

AKA Dividendenstrategie von @anon17469660

Actually yesterday’s article on the Tagesanzeiger is one to pay attention. We need to wonder for how long you will still be able to buy in the 2nd pillar as we can today…I wouldn’t be surprised if they will change the system closing loopholes that enable aggressive tax avoidance

I think the problem is not about voluntary contributions. The pension gap arises because of increase in salaries. Just because someone makes more money doesn’t mean they are avoiding taxed via contributions.

Of course government can limit amount that can be contributed every year to X% of annual income to avoid big purchases. In addition, the calculation on how voluntary contribution potential is calculated could also be changed. Today it doesn’t take into account years of service in CH. It just takes into account your age.

However the loophole that might be closed is

staggered withdrawal that is caused via house purchases. It could be that total cumulative withdrawals would be taxed irrespective of when you take them out.

tax avoidance when people move abroad to favorable countries. This is not easy to change because this is driven by DTAA.

I feel Swiss press these days seem to pretend that they forgot what the business model of Switzerland is. CH wants rich people to live in CH and offer them lower taxes. Same is true for corporations too. There is no point complaining about advantages for the rich when the business model is based on that.

waah wahh some people are paying in 100k’s into their pension in a year

waah waah one or two people ended up with a 8 figure pension pot

waah waah if they were taxed on this 8 figure amount as income they would pay $xxx but instead they pay only $yyy

what they miss out is:

what is withdrawn from the pot is not necessarily what is put in. capital invested outside of pension would not have any withdrawal tax at all

if you invest 1000 per month for 40 years, with decent growth you’d end up with a pot over $8m. assuming a marginal tax rate of 20%, you’d have saved 96k of tax over the 40 years. assuming you pay a low 5% withdrawal tax, you’d still pay over 400k in taxes, far more than you would have saved in tax deductions

But by staying put, you are providing (tremendous) shareholder value. Thank you for your sacrifice. (of course sarcasm, before anyone thinks I’m serious)

The whole topic in the forum here has aged like fine milk There are no changes yet on the tax deduction, but taxing you more when withdrawing the capital, basically is just the other side of the coin.

Politicians are already speaking about a probable referendum, also citing the break of trust, as critics argue that increasing taxes on lump-sum pension withdrawals violates the principle of good faith and weakens the three-pillar system. According to Urs Arbter, director of the Swiss Insurance Association, citizens contributed to the 2nd and 3rd pillars with the expectation of stable regulatory conditions, and changing the rules now undermines that trust.

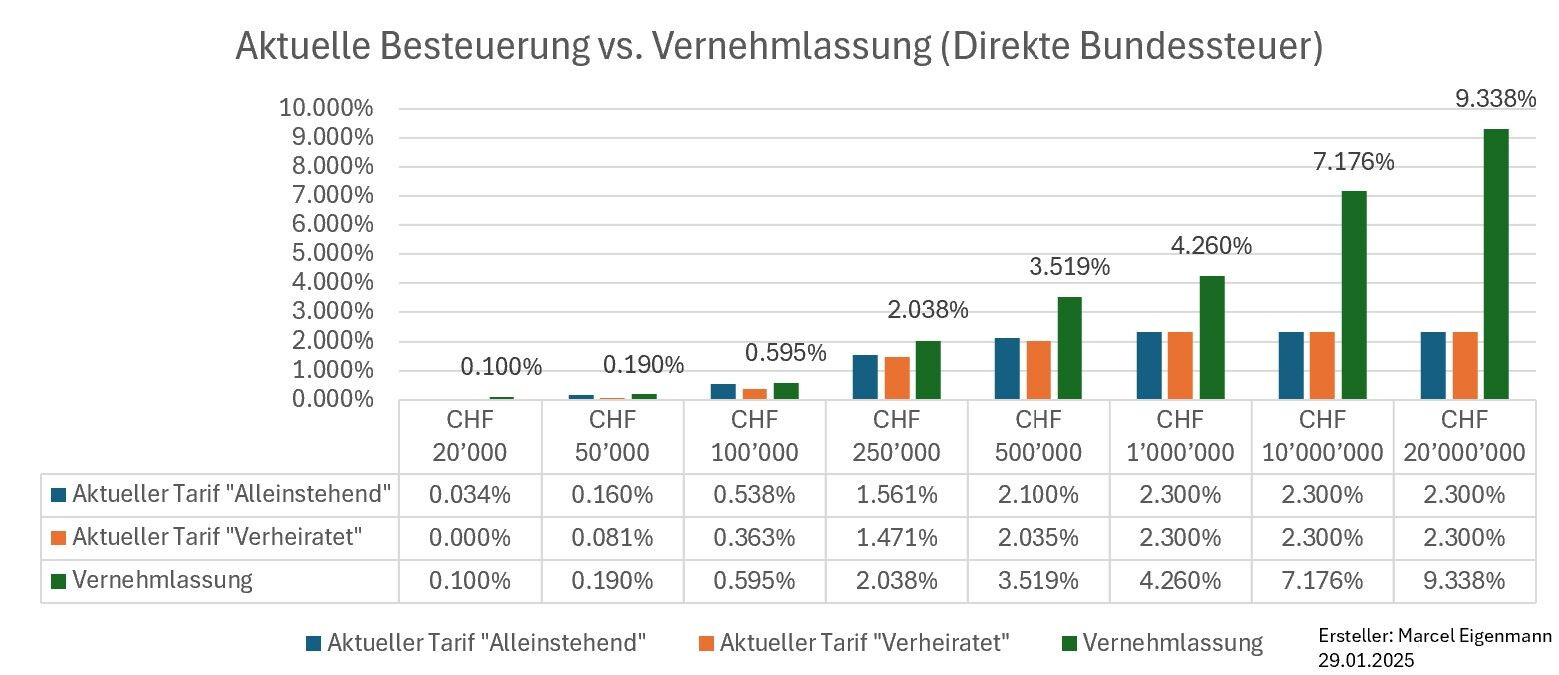

Key changes:

Higher taxation on lump-sum withdrawals:

The new progressive tax rates apply to both the 3rd pillar (Säule 3a) and the 2nd pillar (pension fund capital withdrawals).

The higher the lump sum, the higher the tax rate.

Larger withdrawals from the 2nd pillar are particularly affected.

Lower taxation for smaller withdrawals:

Small and moderate capital withdrawals, typically from Säule 3a, will still be taxed at relatively low rates.

This is especially relevant for self-employed individuals, who often use the 3rd pillar as a substitute for the 2nd pillar.

Staggered withdrawals over multiple years can help reduce the tax burden.

New progressive tax structure:

Up to CHF 100,000 → 0.1% to 1.0% tax rate

CHF 100,000 – 250,000 → 3% tax

CHF 250,000 – 1 million → 5% tax

CHF 1 million – 10 million → 7.5% tax

Above CHF 10 million → 11.5% tax

For comparison, the original maximum tax rate for lump-sum withdrawals, was 2.3%, now can go up to 11.5% .

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.