If I understand correctly the 2nd pillar pension system one is allowed to do some voluntary extra buy in (once per year) up to a certain limit and this amount can be fully deducted from the taxes.

So this means theoretically one could buy into their 2nd pillar up the the full amount of their expected yearly taxes. As an example let’s say I pay yearly 50k taxes I could pay this amount into my 2nd pillar pension and expect 0 CHF taxes the following year.

That sounds like a good option to me but maybe I am not getting it right here… What’s the catch? and is anyone doing that here?

Oh yeah right, you deduct this amount from the income you declare and not from the amount of taxes you pay at the end. That would have been too good to be true…

I general it’s also not interesting to reduce income too much due to the progression of the rates, the buy-in potential is limited so you want to use it for the income that’s at the top rate.

You cannot decide for yourself what to invest in (unless you have 1e)

There are pension funds (there are exceptions) that don’t perform so well

The latter is the reason why many invest the money outside the pension fund (so that the money grows faster than inside) and then only pay it in before retirement (observe the deadlines before retirement). But with a tax burden of CHF 50,000 this situation probably looks different.

This is a classic topic for independent financial planning.

Der nach dem Reglement der Vorsorgeeinrichtung versicherbare Lohn der Arbeitnehmer oder das versicherbare Einkommen der Selbstständigerwerbenden ist auf den zehnfachen oberen Grenzbetrag nach Artikel 8 Absatz 1 beschränkt.

Art 8 BVG

Zu versichern ist der Teil des Jahreslohnes von 25 725 bis und mit 88 200 Franken.

I don’t remember the name of the guy this change was informally named after, but there’s a story there

I think if your fund offers higher contributions from salary like PLUS or TOP then it’s better than voluntary buy-In. I just used some nomenclature I am aware of but essentially some employers offer pension fund plans where employee contribution can be higher than standard

For small amounts I would choose higher % contribution rate

Why?

these are not considered voluntary and hence don’t lock your fund for 3 years

Unfortunately this is not the case of my employer, it’s pretty much the “standard” stuff and rate. I guess for a lot of people these terms are non-negotiable except maybe if you have a higher manager position.

Don’t hesitate to contact your employer (most likely HR), or the employee representatives for the pension fund if you have them (I’m one of them for my company, we introduced it this year), and ask for it.

Those kind of “PLUS” plans usually don’t cost anything to the company, and my understanding is that pension funds like them as well. It’s just a tiny bit more administrative work for your employer to ask every year who wants to be on which plan.

So the probability they’re willing to introduce it is non-negligible, they might just not be aware that it’s possible.

1e plans are a lot more complex to implement on the other hand.

There are good arguments for making voluntary contributions to close gaps in your pension fund:

Many employees in Switzerland have substantial gaps in their pension fund, often in the range of 50-100k. That makes it one of the biggest potential income tax deductions for many if not most employees.

Pension benefits do not count towards taxable wealth for wealth tax purposes. The longer the money will remain in the pension fund, the bigger the potential wealth tax savings are.

Swiss pension funds are interest-bearing vehicles (1e plans are an exception), so they can be used for the interest-bearing portion of your portfolio (the bond portion).

If you plan to get a pension from your pension fund (instead of withdrawing the benefits as a lump-sum), closing gaps in your pension fund will result in your pension more closely reflecting your pre-retirement income. The same may also apply to disability and survivor’s pensions. However, each pension fund has its own terms and conditions with regards to voluntary benefits. Some may only let you withdraw these as a lump sum (not as a pension). There are also some disadvantages:

There is a potential opportunity cost compared to stocks, commodities, and real estate. For that reason, pension funds should only be used for the bond/cash portion of your portfolio. If the bond/cash portion of your portfolio is already complete, it does not make sense to close gaps in your pension fund.

Your money is not readily available. It is held in trust by the pension fund, and you can only withdraw it under certain conditions.

If your pension fund’s solvency quota falls below a certain thresshold, you may not be able to make early withdrawals until the pension fund becomes solvent again. Other negative measures may also apply. As mentioned by others, it is important to check your pension fund’s solvency quota.

As with banks, etc. it is possible for a pension fund to go bankrupt. Voluntary benefits to close gaps are not protected the LOB Guarantee Fund (non-compulsory benefits that result from using a pension plan that requires additional contributions above what is required by law, on the other hand, are covered by the LOB Gurantee Fund, within limits). So you risk losing money if the pension fund becomes insolvent.

Pillar 2 (not 1e variant) is often compared to the bond part of one’s portfolio - I’ve always wondered whether it is really the case? I understand that they are both interest bearing instruments, but that by itself does not seem enough: is there evidence that there return-risk profile is compatible?

Even the ordinary (non 1e) BVG 2nd pillar is much better than typical bonds. Here’s why:

Full capital protection, with virtually no downside risk (even in a worst of worst case the pension fund can tap the employer and if necessary the insured employees to restructure itself to uphold that guarantee).

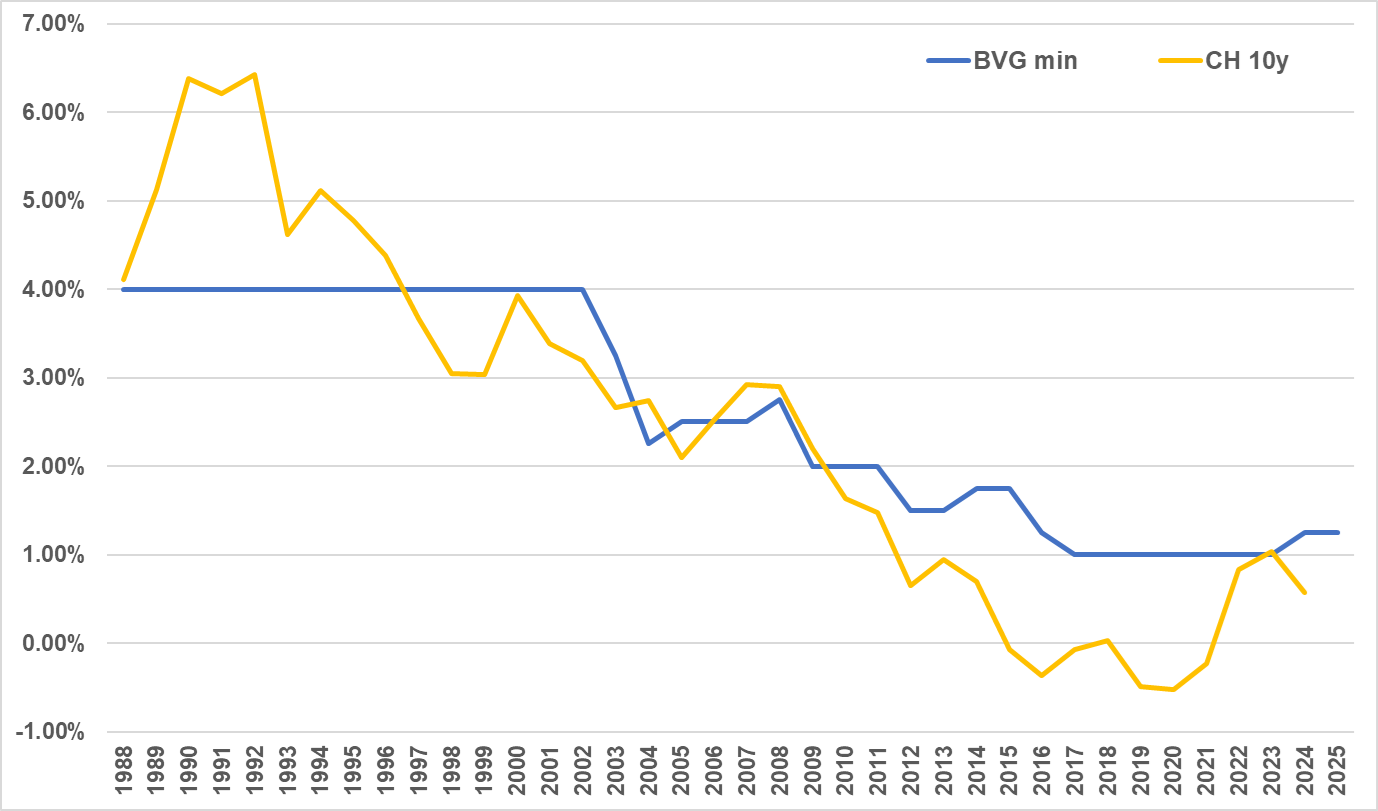

The guaranteed minimum return is equal to or better than that of 10 year Swiss treasury bonds, see graph below.

You benefit from the upside if the funds performance is good, with good pension funds paying much more interest than the required minimum

Your money is invested tax sheltered, both from income and wealth tax

You have the option to pull your money out as annuity when you retire, at an extremely beneficial conversion rate you would never find on the free market.

The only negative thing about the 2nd pillar is that you can’t voluntarily increase your risk and return profile, unless you have access to a 1e solution (which is odd because it is the one investment nearly everyone has with a decades long investment horizon).

Comparing BVG guaranteed minimum interest vs return of 10 year Swiss treasury bonds (sources here and here):

As 1742 explained, pension funds have very low risk compared to most bonds. I would dare say they also have lower risk than money market funds, and possibly even savings accounts. But with the exception of 1e plans, Swiss pension funds are interest-bearing instruments and belong in that portio of your portfolio.

My point was that you should only invest in your pension fund if your portfolio/strategy has a component for interest-bearing instruments, and that component has enough free space to accomodate the voluntary pension fund contribution without throwing your portfolio off balance.

That might explain why pension funds can maintain such favorable interest rates and conversion rates. Theoretically their business is taking the difference between what they earn by investing pensioners’ capital and the amount they pay out in pensions.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.