It factors in stamp duty (0.15% for Saxo/Swissquote, 0% for IBKR), FX fees, custody fees, tax statement costs, and projects the actual end wealth after all costs for your specific monthly amount and time horizon. Saxo’s AutoInvest is simulated with cash pooling (whole shares only, no fractional).

A few things to flag upfront:

The site is currently German only, sorry. English is on the roadmap.

It covers Saxo Bank, Swissquote and IBKR for now.

Free, no affiliate links, no ads.

Would genuinely appreciate feedback from people who actually know this space. Anything obviously wrong or missing?

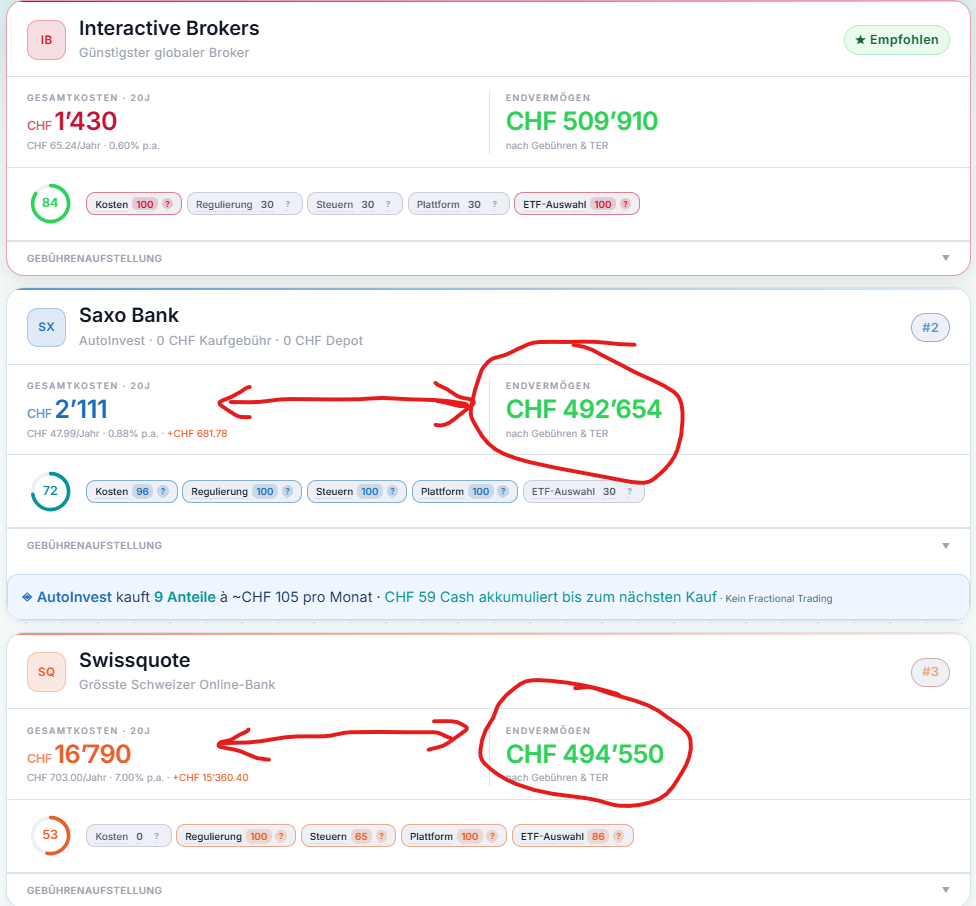

The calculated Swissquote costs are not realistic, or at least not optimized. If I were to buy Vanguard FTSE All-World at Swissquote, I would buy it in CHF at SIX. This eliminates the very high FX fees and caps the commission to a maximum of CHF 9.85 per trade (+ exchange fees + stamp duty). This applies to all “ETF Leaders” traded in CHF.

Swissquote will typically still be the most expensive of the three but the difference to Saxo isn’t that big, at least for larger monthly amounts.

And I’d choose the UBS Core MSCI World ETF (IE00BD4TXV59) over the iShares MSCI World. It has a TER of 0.06% instead of 0.20% and it’s also traded in CHF at SIX.

My personal preference is also to always calculate with inflation-adjusted numbers, in which case I would be more conservative and assume 5% p.a. for stocks. That may be just me, though. Maybe a slider for the return assumption would make sense.

A larger addition I’d like to see is to include selling but as monthly selling over a number of years, not as a (in my opinion, unrealistic) one-time exit.

Overall, I get a bit the impression that the aim is to make Saxo look good and/or make Swissquote look bad. I’m not claiming that you’ve intentionally built this to be misleading. However, as it is, I consider it an unfair comparison. It probably won’t require too many changes to make it a reasonable and useful comparison, though.

Most of the ETFs are iShares ETFs, which are eligible for AutoInvest but are otherwise not the best choices (significantly higher TER, especially for the MSCI World case mentioned above). A good option might be to let the user just select the index and allow the tool to choose the ETF with the best conditions at each particular broker (or even show separate calculations for each broker-ETF combination of a particular index).

And this claim is also misleading:

You get 0.002% at IBKR only for $100k+ trades. The maximum trade amount you can choose is CHF 5’000 at which point the best you can get at IBKR is 0.03% with auto-conversion (which is obviously still great).

I think IBKR and Saxo are both great brokers and Swissquote is too expensive at least in some aspects. A fair comparison should still result in IBKR and Saxo coming out at the top. There is no need to make it unfair to Swissquote or improve the odds for Saxo by choosing AutoInvest-eligible ETFs.

706-NA applies only to people holding US situs assets such as US stocks and US ETFs, right? Investing exclusively in UCITS ETFs (as in your comparison) shouldn’t require 706-NA. IBKR may still be a bit more complex to deal with compared to a Swiss broker but with UCITS ETFs, it shouldn’t be a big issue either.

You and jay are not wrong. This really is my blind spot and I agree it‘s biased. The reason is I started building it for myself and my friends first. We were discussing back and forth about the cheapest broker. I couldn‘t really find a comparison tailored to my investing plan. Since we were mainly discussing Saxo, SQ and IBKR. I only focused on the three. In order to be able to calculate for all three brokers, I decided to choose the biggest ETFs based on volume that can be purchased on all three brokers. But I took the ones that can also be Auto Invested on Saxo. The feedback is good and I agree with both of you. It needs a more neutral approach.

Depends on how you define „building“. I definitely let Claude do the coding (and noted it in the footer of the website). But I spent way too many hours actually building it and experimenting with it until I got the calculations to work and the UX to be somewhat streamlined.

The initial main goal of the tool was to just see the total costs when you account for everything. So on the left you see the total costs and on the right you see the projected wealth minus the costs (assuming 7% yield and compounding).

Hi jay, first of all thank you for your very appreciated feedback. As noted in my other comment to Phil Mongoose, the Saxo bias is real and definitely was my blind spot until your comment.

The CHF-traded ETFs point is a good one and honestly something I hadn’t fully accounted for. You’re right that buying VWCE in CHF at SIX avoids the FX fees entirely and caps the commission at CHF 9.85. I’ll look into how to reflect that properly in the calculator.

The UBS Core MSCI World tip is also useful, 0.06% TER is hard to beat. I’ll add it to the ETF list.

The return slider is already on the roadmap and your inflation-adjusted framing makes sense to offer as an option alongside the nominal view.

The decumulation scenario (monthly selling over time) is a bigger feature but a genuinely good idea.

Thanks again, this is exactly the kind of feedback I was hoping for.

You’re right on the FX fee claim. That’s misleading and I’ll definitely have to fix that.

The ETF selection bias is also a valid point. Having mostly AutoInvest-eligible iShares ETFs does skew the comparison in Saxo’s favour, even unintentionally. The UBS Core MSCI World you mentioned is a good option that doesn’t fit neatly into the current structure.

And the CHF-traded Swissquote scenario from your first comment is something I need to model properly.

I’ll work through these and update the calculator. The goal was always a fair comparison, so if the current version doesn’t reflect that I have to fix it. Thanks for pushing back!

If I do back of envelope calculations to compare buying same ETF on all platforms . Let’s say SPDR ACWI which is sold in CHF

IBKR will cost 0.05%

Saxo will cost 0.08% + 0.15% stamp duty

Swissquote will cost 5-10 CHF flat per trade + 0.15% stamp duty + 80-200 CHF custody fees.

So this means Saxo should be more expensive than IBKR but it’s not a very big difference. For 1000 CHF monthly investment, the total additional cost for 20 years would be 432 CHF.

Calculation for Swissquote are a bit tricky because they have capped custody fees & flat trading fees for key ETFs. But still the difference would not be life changing

I don‘t get your comment. I put that myself there. I could‘ve tried to hide it if I didn‘t want anyone to know. As long as AI isn‘t the thought leader and just does the tiresome coding according to your needs and vision, I think that‘s ok I‘ve also seen tools that are done 100% by AI including the thought leadership. But this isn‘t one of those.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.