Buying market index funds is an active bet on the market and increases the value of the market relative to other investments. This can be a bubble.

If the index is constructed well (maybe free-float market cap weighted), it will impact the prices equally, leaving no (additional) opportunity for arbitrage within the index.

If intelligent active capital is too small to arbitrage inefficiencies from “passive” index investment and dumb active investment, their return will increase. They will outcompete other investors and their wealth share will grow until all inefficiency is arbitraged (at least) down to friction constraints.

Is that your conclusion, or AI’s?

If the latter, is AI maybe “bullshitting” us again? (I mean no offense to you (although I don’t care about AI’s feelings). I hope no offense taken!)

…Or at least not giving us the whole picture.

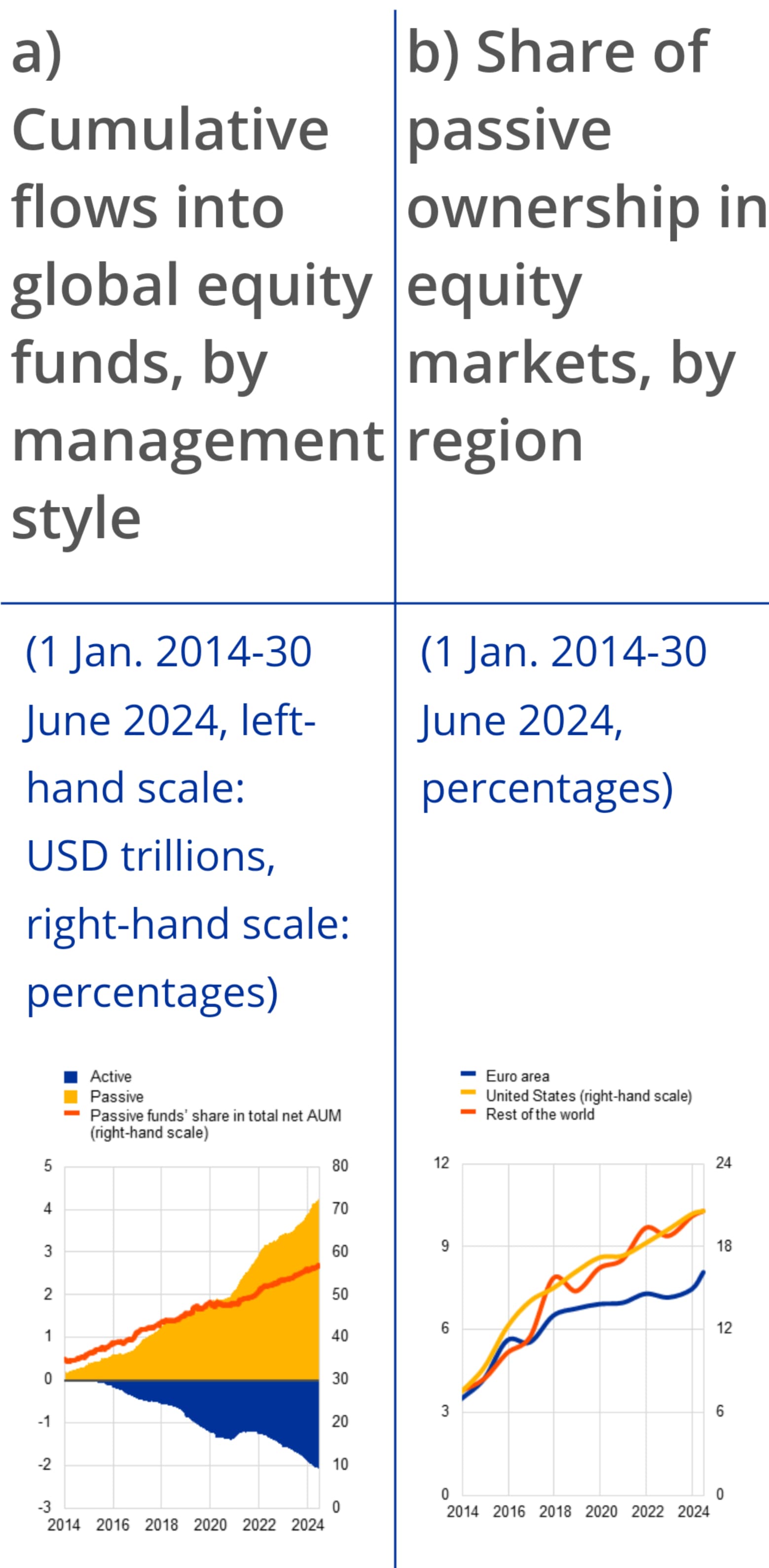

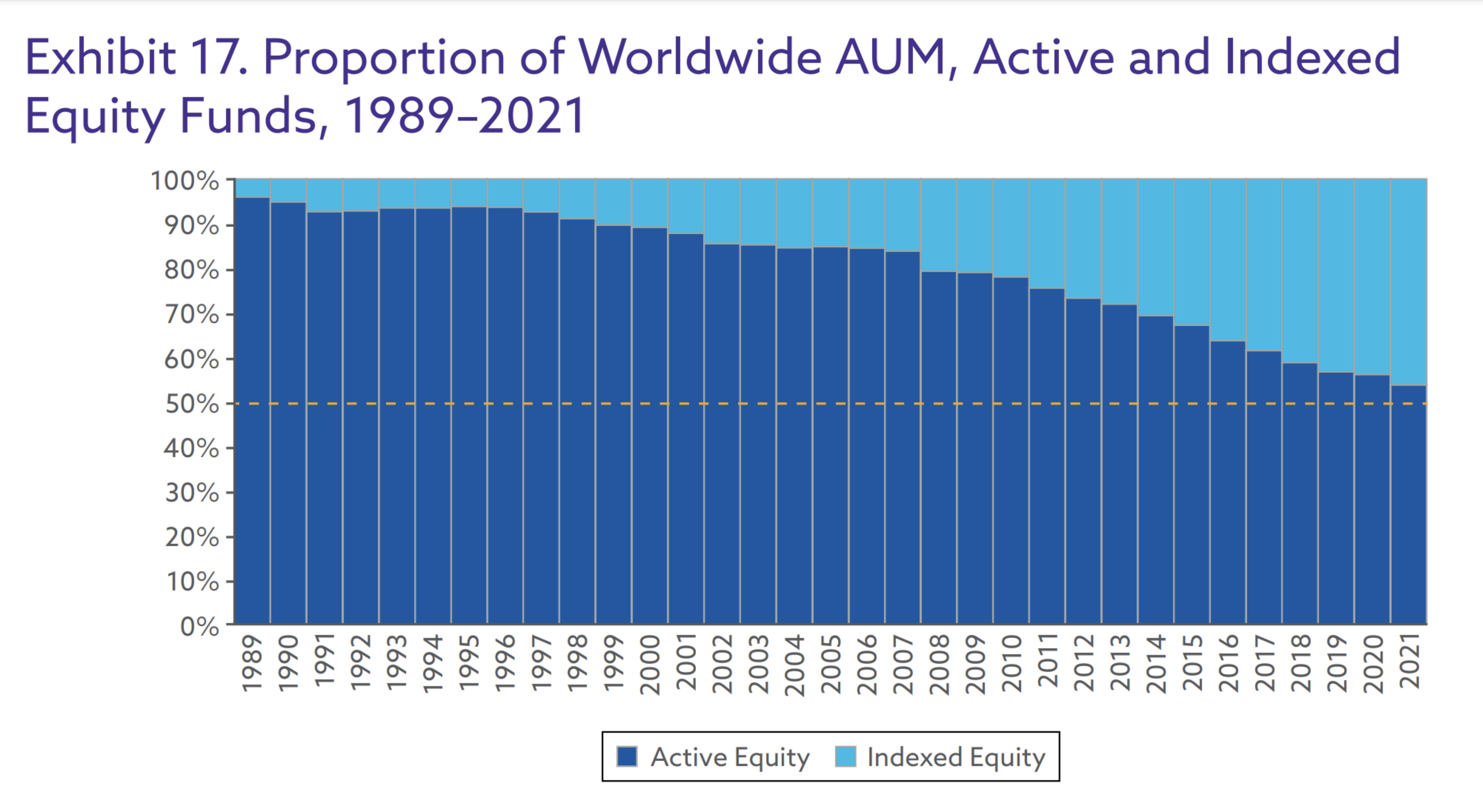

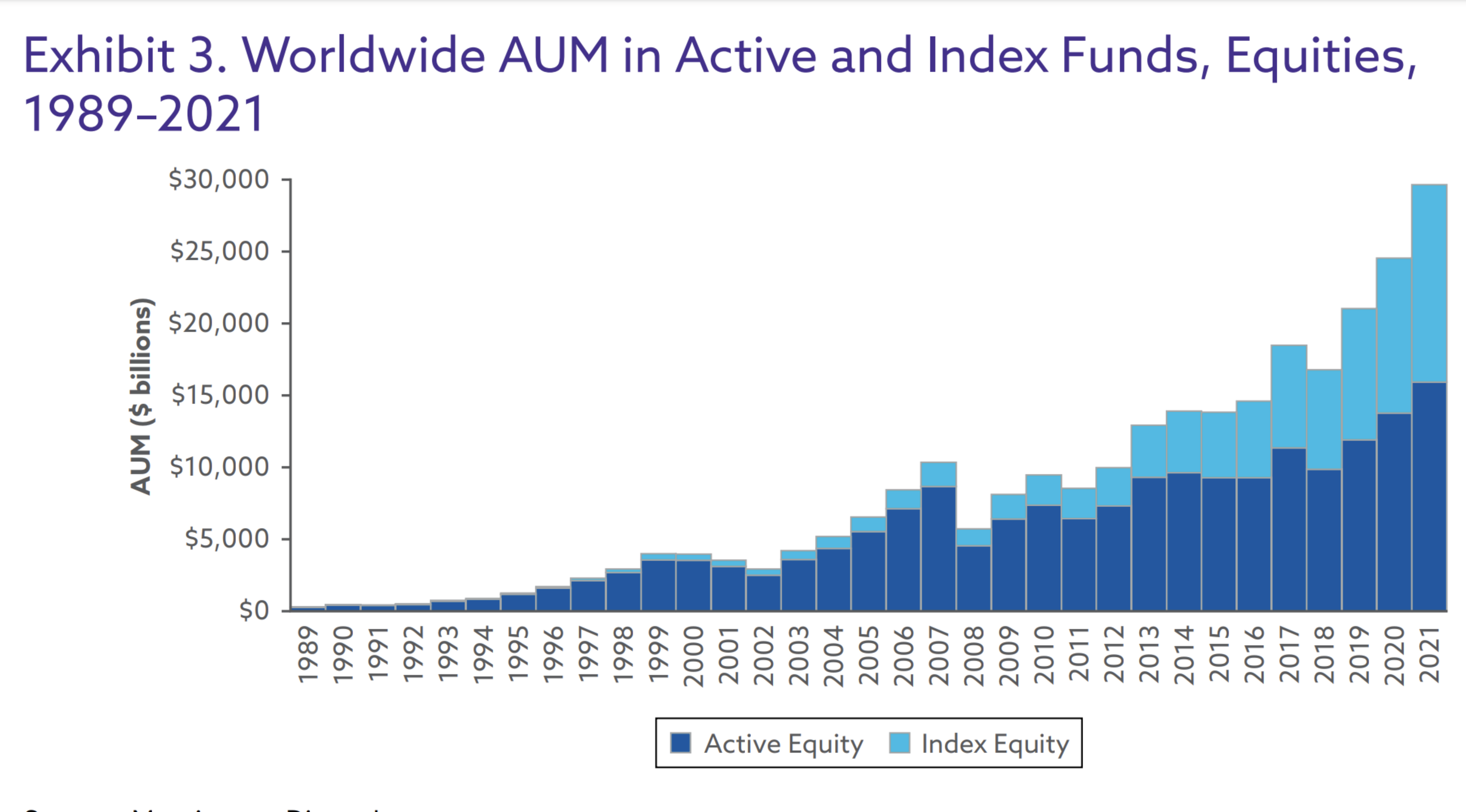

These points seem to be taken from these charts in that report.

Passive fund is about 60% of total fund AUM.

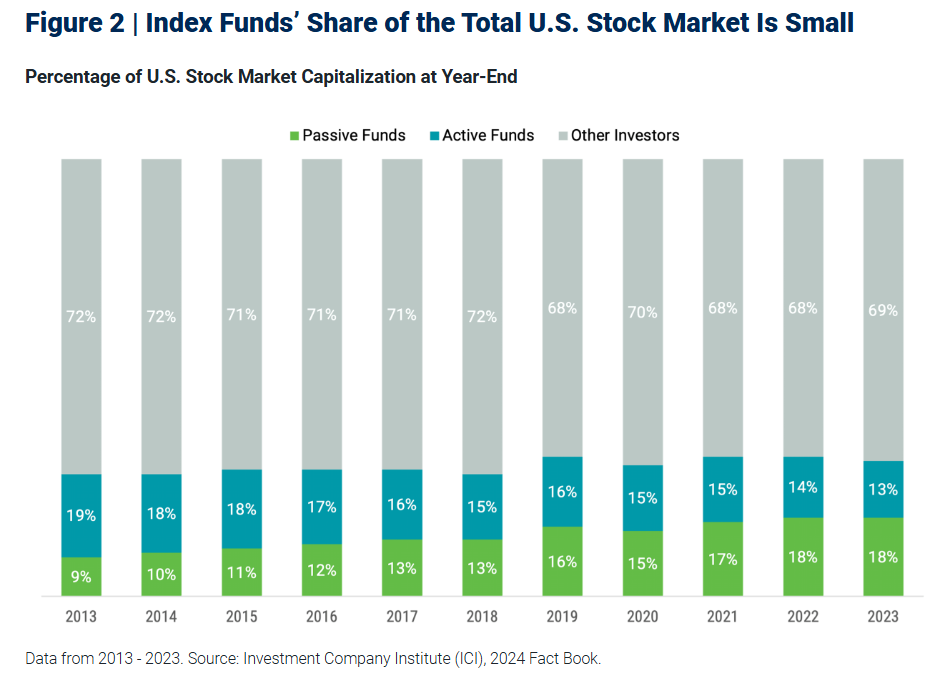

But total fund AUM is only about 20% of total Equity market value (120 trillion). Isn’t the value outside funds “active” too? @Your_Full_Name 's stockpicking etc. is in the 90 trillion outside of funds and efficiently & correctly values the equity.

We acknowledge that this still may not provide a complete picture of the ownership of companies attached to passive strategies, given that there may also be passive approaches managed in institutional and retail separate accounts. A recent study considered this reality and estimated the actual ownership of passive strategies between 30% and 35%.1 So, while it’s difficult to determine the total share of passive investing, we know it becomes much smaller when we expand our view beyond mutual funds and ETFs.

I wonder what ‘Other Investors’ are … I would have assumed that most assets are owned via funds (in the article’s terms this includes mutual funds and ETFs), but apparently not.

I think the article suggests that ‘Other’ is or includes “direct holding”, but it’s not entirely clear.

yes that’s why they are estimating “passive” strategies to be 35% of market because other also includes family offices etc who might have index hugging strategies too

This is one of the times when stocks have made a significant appreciation and everyone is scared about the future.

It is quite possible that we’re seeing the “unpuzzling” of equity premium puzzle.

The stock market has been reduced to one stock: VTI or VT if you prefer global. The risk of VTI is lower than of any subset of the stockmarket. As we know that investors are compensated for only undiversified risks, the equity premium is reduced to the risk level of VTI.

Hence higher valuations and lower future returns.

PS although it is likely to be true, the returns in the next 10-20-30 years are unpredictable and will look more like noise.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.