I think I’ve read the discussion a bit here and a bit there, but it wasn’t the main topic so I repeat it here.

Is it better to have bond (or bond-like) ETF on a normal account like IBKR/PF/SQ or on a 3a account?

I think the preferred solution is to have all stocks on 3a, since it’s long term, and bonds on a normal account. “Long term” shouldn’t be the main reason though, since we can always rebalance a 3a account as well, so it doesn’t matter. The main reason to have something on 3a is to avoid taxes, so I’d imagine that it’s preferred to have dividends on 3a rather than on “normal” accounts, but also that could be avoid by having all accumulating accounts everywhere.

So is there a preferred place for them?

You are quite limited in how much you can put into the third pillar on a yearly basis (CHF 7’065 for employed, or 20% of profit for self-employed with a maximum of CHF 35’280 [1]).

If you plan to only invest CHF 7’056 (CHF 588/month), then sure, putting everything into a3 is a good choice, otherwise it’s just a small addition to your portfolio to save on some income+wealth taxes. I personally just want the highest return possible for both portfolios. And since capital gains are not taxed I don’t understand why it should be better to have all stocks in 3a?

You pay taxes, once you pay out your third pillar [2]. If you sell your normal portfolio, you won’t. Sure, over time you save on wealth taxes, but if you live in Schwyz/Zug, it’s negligible. And your normal account will always be bigger than your 3a account anyways…

You could put your dividends/interest you get from your normal account, towards 3a so they are kinda tax-free, because you write them off in your tax declaration by butting them into your third pillar. But that’s just a random non-complete thought.

high yield assets (tax advantage on dividends/interests)

low capital growth ones (reducing the tax drag when withdrawing for something that wouldn’t be taxed in taxable)

assets that allow for recovery of witholding tax that I couldn’t otherwise recover on my own (I haven’t studied that but Japan, I guess?)

Bonds/bond funds would tick the first two boxes so they would be good candidates in my opinion.

As long as you have assets both in 3a and taxable, it doesn’t matter: you can sell stocks in taxable and buy more in 3a (by selling whatever other allocation you have in there) to make it a mostly neutral operation on a global portfolio basis.

Accumulating ETFs in taxable accounts are still taxed as if they had issued the dividends so that’s mostly a moot point too.

It is an interesting discussion. I never really thought about it but now that i did, I tried to formulate the equation. I am going to ignore the impact of witholding tax rate for foreign dividends for now but i know that is also different for swiss residents.

Higher level understanding from my side is that 3rd pillar defers the taxes to later period and is often taxed at lower rate (lump sum) than marginal tax rate…BUT the whole amount is taxed for lump sum tax and this is important to consider. Taxable account like IB would obviously reduced effective income yield but it is not taxed at the end of the period for capital gains.

Wolverine already highlighted his thought process which i think makes total sense. However i just wanted to do the math

N = Number of years to retirement

r = income yield of investment

t = Tax on income on yearly basis (defined by marginal tax rate)

r* = r*(1-t) effective yield post tax

c = capital gains yield

Lt = Lump sum tax at withdrawl (defined by residence domicle at time of payout)

Value of 3a account at time of retirement

((1 + r+c)^N) * (1- Lt)

Value of IBKR account at time of retirement

((1+r*+c)^N)

So i tried to simulate this. But there are many variables which can affect the decision. Some are below

a- If your contribution to IBKR is more than contribution to 3a OR NOT

b- what is your assumption for expected income and capital gains yield for asset class (Stock vs bonds)

c- what is your marginal tax rate

d- what is your lumpsum tax rate

e- What is your overall asset allocation (stock vs Bonds) across IB /3a

An example

Assumed bond etf income yield = 1%

Assumed bond etf capital gain yield = 1%

Assumed stock etf income yield = 2%

Assumed stock etf capital gain yield = 4%

Contribution to IBKR annually is 2X of 3rd pillar contribution (i.e 14K in IB and 7K in 3a) and I will only simulate one time contribution and not yearly contributions

Holding period 20 years

Marginal tax rate 30%

Lumpsum tax rate 10%

Targeted overall Bond allocation = 25% (IB + 3a)

Variables that can change are following

Bond allocation in IB

Bond allocation in 3a

Constraint is that weighted average bond allocation needs to be same as 25% target

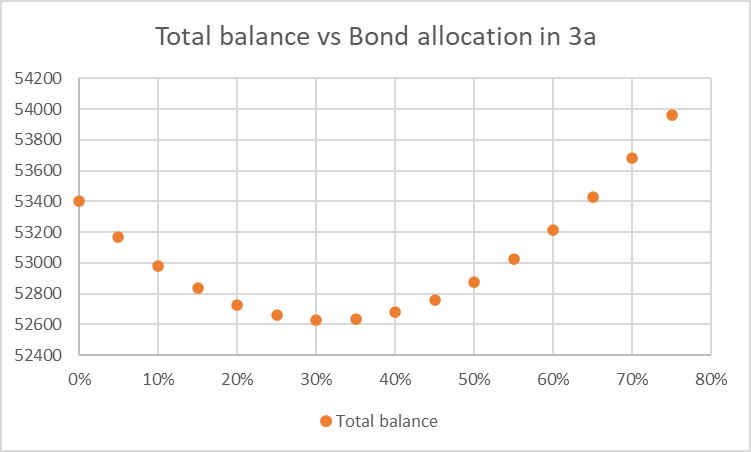

Conclusion - model is suggesting to put all bonds into 3a. But i found it interesting that having a split strategy is reducing the overall returns. I would love to see if someone can challenge this conclusion. I have a feeling i might have missed something.

To me intuitively this makes sense because the objective of 3a is to have tax deduction at the time of contribution and i believe the lumpsum taxation at the end reduces the incentive to grow this account. So if this account does not grow that much, then it doesnt matter much. However, this might change if Lumpsum taxation was much lower or much higher. I would let you simulate

P.S - I wanted to attach my excel simulator but i dont know how to do that on this forum

Ok, so it seems that bonds are better in 3a. It might also be a way to have an 80/20 (or similar) portfolio, since we are limited on how much we can deposit in it.

The choice of ETF in viac is limited:

Still better than using their strategies, since VIAC has just 1 strategy and all they do is increase/decrease the percentage on the CHF Corporate bonds fund. (They don’t believe in Bonds?)

finpension has a longer list and also their strategies use more than one fund.

There is a small problem having bonds on 3a only. If you apply a glidepath or if you need to sell to get money, you can’t sell your bonds if they are segregated there. You then still need bonds outside 3a.

What you do is sell your bonds etfs in 3a, buy an equivalent amount of stocks etfs in 3a and sell the same amount of stocks in taxable. Your amount of equities is unchanged and you have sold your bonds.

I think the analysis I did was for holding the portfolio until retirement. If you plan to increase your bond allocation with age, why would you need to sell bonds?

Won’t you need to buy bonds (in IBKR) to increase bond allocation with age?

I think here, we are just talking about where to put the bonds part of your portfolio. i.e. given your bond/stock allocation, where should you put the bond portion and where the stock.

Now from an income tax perspective, it makes sense to stick the bonds in the 3a as the income is sheltered and if you have growth stocks in ibkr, sales are also not taxed anyway.

One complicating factor is wealth tax, the amounts growing outside the 3a will be subject to wealth tax.

You could also consider the dynamic of putting growth in 3a first and then changing the allocation within the 3a.

example.

let’s say you have 200k bonds in 3a. 800k stocks in ibkr.

after 10 years you have say 230k bonds in 3a and 1600k stocks in ibkr.

if instead you did:

200k stocks in 3a, 200k bonds plus 600k remaining stocks in ibkr

after 10 years: 400k stocks in 3a, 225k bonds at ibkr (assume 5k loss to taxation) 1200k stocks in ibkr

here you have more sheltered in 3a. you could even rebalance then to do:

230k bonds + 170k stocks in 3a, 1425k in stocks in ibkr.

This is very canton dependent, but where I am wealth tax is high and capital withdrawal tax is low - so it makes sense to shelter it from wealth tax and pay the withdrawal tax at the end.

I agree.

One need to add wealth tax in simulations. This will complete the picture. It would depend on what canton one lives in and what’s the difference between Wealth tax and lump sum withdrawal tax

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.