i was just about to open the exact same thread. glad i used the search engine

Seems quite inconclusive atm though

What i got was go for an ETF like VT and if it goes south pay from your emergency fund.

It just this year doesnt look like its going to be a great year for the stock exchange starting from a crazy ATH.

Iam paying yearly something around 12K in taxes so i was interested if there was any short term investments with 5-6% interest and as low risk as possible.

I live in Zurich

Also someone commented on “Vermögensteuer” which i have completely no clue , if anyone was kind to explain it a bit.

Finally I decided beginning of this year to invest the money required to pay my taxes in a what I believe to be a low-risk bond ETF. To be precise that is Vanguard’s US treasury bond (VUTY) which I buy at no cost on DEGIRO as it is on the list of their free or charge ETFs.

If that is a good solution in terms of profit, I can clearly say no, as the price has even lately been dropping due to probably the currency appreciation of the USD. But I did not want to invest in any bonds in Europe, Switzerland or emerging markets so what’s left? US… US bonds still enjoy from positive interests rates as far as I know and it’s always better than my bank account.

You mention looking for 5-6% interest with low risk, which on top of that has to be short-term as you will need to money latest 1 year later to pay your taxes… let me tell you that will be very difficult, and if you find, please do let us know, we would all be interested to invest there and no, unfortunately P2P is not the way to go to achieve that (I just saw your post in the P2P thread).

@mabi thank you very much for the thorough update. I dont understand bonds yet ,unfortunately the only market i know is the crypto market. for me a swing of 5-6% percent up or down is sometimes literally the few seconds it takes to refresh a price.

So far the ETF approach with with the emergency fund backing that seems quite reasonable and i will see if the swiss p2p lending platforms make any sense .

in any case if i do act on anything i will share it here for others to see learn from my mistakes

That’s right, the CHF seems to have depreciated for example in regards to the USD (CHF/USD currency pair) since around mid of February which means it gets more expensive to buy US treasury bonds for us living in Switzerland and being paid in CHF but on the other hand if we sell now our US treasury bond we would get more money as logically the USD has appreciated in regards to the CHF (USD/CHF currency pair).

So now back to the price of our US treasury bonds ETF it looks like the appreciation of the USD is one factor among others which brings the price down.

I’ll use these values for debt from Taxes 2019. That’ll be the exact numbers.

For tax debt from 2020, even though only due on 31.5.2021, I will add up,

Kantonale Steuer netto (Verrechnungssteueranspruch & Steuerrückbehalt USA has been subtracted in this value)

Gemeindesteuer

Bundessteuer

All together called “Voraussichtlicher Gesamtbetrag ordentliche Steuern 2020”

These 2020 numbers I obtain from the Steuerkalkulator at the end of doing the 2020 Steuererklärung.

This value minus the Akonto-Zahlung 2020 I already did for Kant. Steuer before end 2020 = Debt from 2020

Basis: "Die am Stichtag (31. Dezember) nicht bezahlten Steuern des laufenden Jahres und früherer Jahre können als Schulden abgezogen werden. Dies gilt auch für die direkte Bundessteuer, obschon die Steuer für das vorangegangene Jahr erst Ende Februar fällig wird.

Zu erwartende Steuerforderungen früherer Jahre können ebenfalls abgezogen werden (Einkommens-, Vermögens- und Grundstückgewinnsteuern usw.)."

ok soooo lets experiment! as i told you if i act on anything i will share and you can learn from my mistakes.

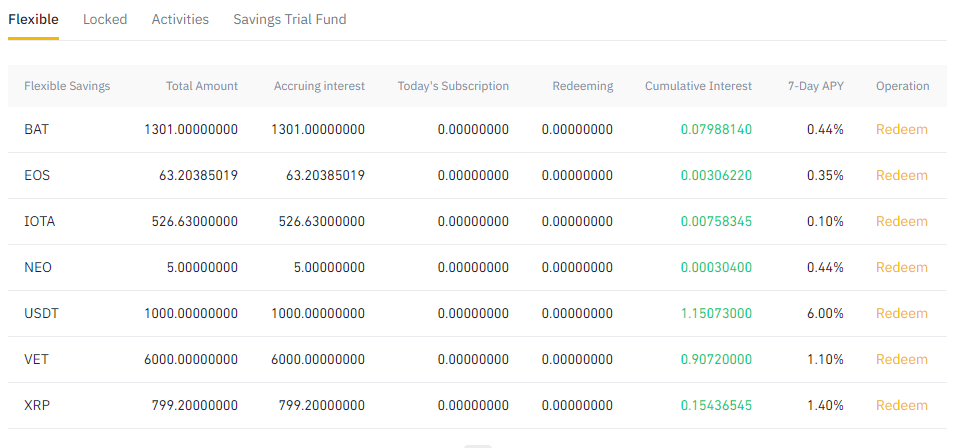

So i had few USDT lying around in binance doing nothing so iam trying the following

1000 USDT on a flexible savings account expected annual return 6%

1000 USDT on a 7 day locked savings account expected annual return 6.3%

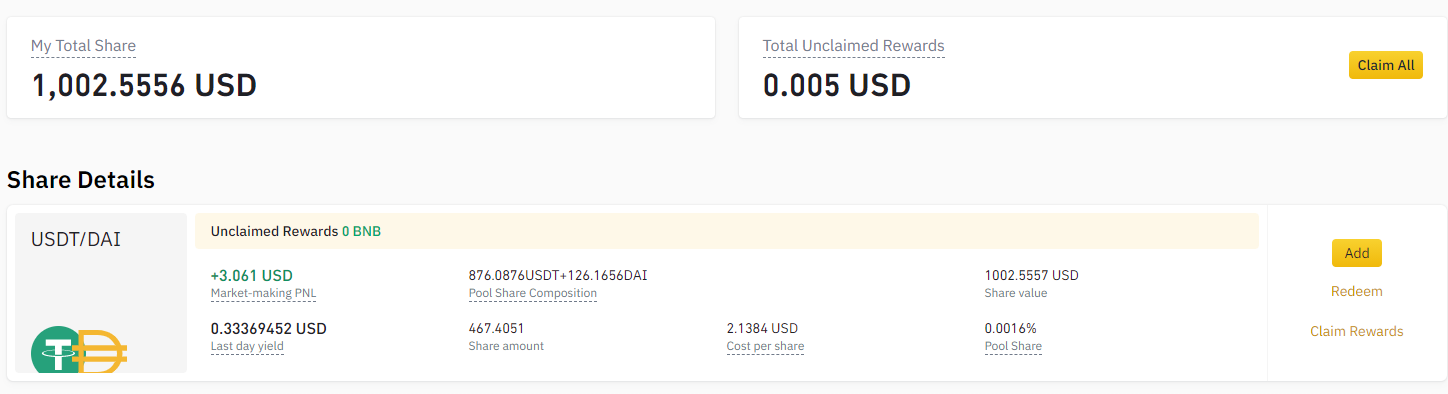

1000 USDT in a liquid swap paired with DAI with annual return 11.5%

will check 7 days later and report back with what happened : )

My understanding of the settlement with the new york attorney general is that tether will be required to publish their asset backings soon. I could’t find a deadline for this though.

Personally I’d avoid locking money in USDT at least until they provide that information…but I’m probably too risk-averse for this anyway.

Alright Alright Alright time to report back with the Results!

so 1) returned in 7 days 1.15 CHF money remains on the usdt savings account till i pull them the account is credited daily with the returns

2) returned in 7 days 1.2 CHF, money was returned to my main USDT balance no fees

3) returned in 7 days 2.4 CHF (net after taking out the fees)

1 and 2 are as straightforward as it gets and iam in binance now for 3 years with absolutely no issues.

3 there are more risks around that plus if you dont have both currencies that the swap pool supports you will pay some fees for partial conversion ,also the available information on the topic on forums etc is beyond minimal (or my google-fu went rusty)

…but what about a 4th experiment with bigger returns? →

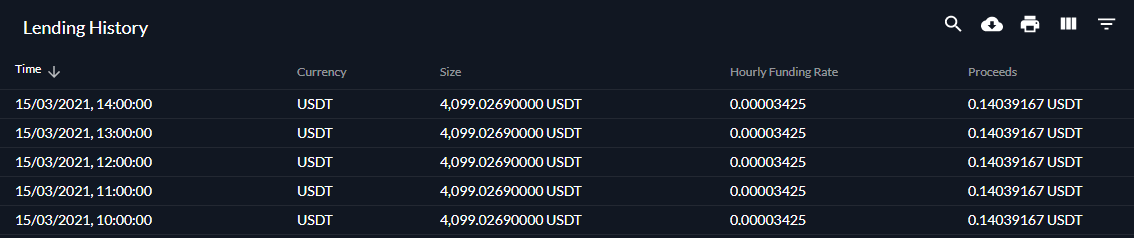

So couple of days later i find out FTX that has similar functionality albeit with higher and more volatile returns. so there i get for USDT an average of 20% p.a hourly. i say hourly because the rate changes every hour, funnily enough it supports also Fiat lending and USD -so far had better returns sometimes reaching 100% p.a hourly

So on 3 days ago i transferred there 4000 USDT that they were sitting in Binance doing nothing and so far it has returned 6 CHF

FTX is a much newer exchange but seems to be on the right track for the right reasons ,having said that iam still far from trusting it the same way i trust binance so for me this is higher risk. Though the fact that it supports Fiat lending thus removing the risk of the cryptocurrency makes it a very descent choice for me.

This are my money and my experiments and my risk tolerance you be you and have your own parameters. What i would say for sure is irrelevant to what exchange you sign up on take it slowly and by that i mean, take the time to transfer really small amounts see how it works how much time does it take what kind of fees are involved then also withdraw and look at the same parameters, then and only only then when you fully understand the process transfer bigger amounts.

Here also pics so you can see how it looks like plus its proof : )

Buying crypto → instant without a delay and fair market price ( 1% fee for the transaction…).

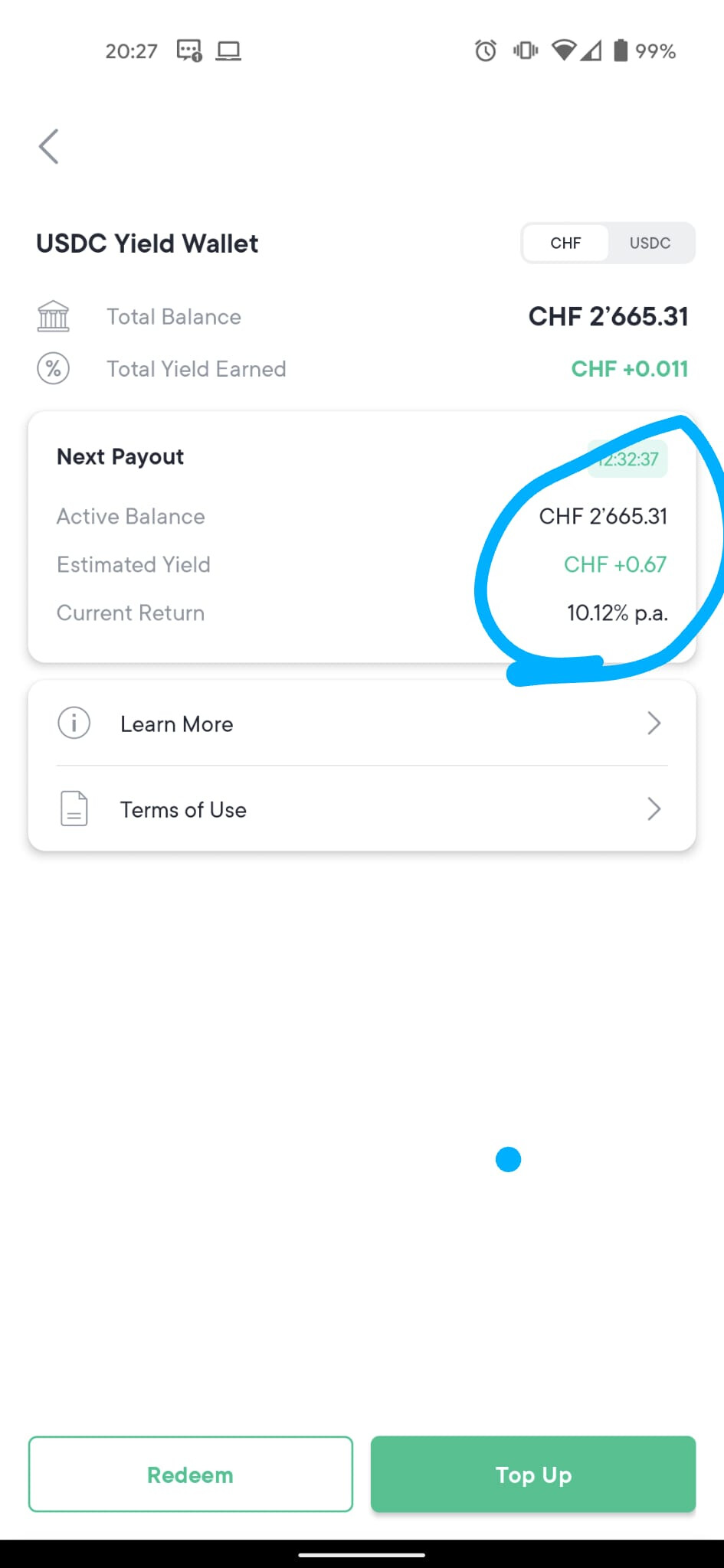

I invested some money in the USDC and activated the Yield Wallet option to get daily interest.

At the moment 10.12% p.a.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

and no, unfortunately P2P is not the way to go to achieve that (I just saw your post in the P2P thread).

and no, unfortunately P2P is not the way to go to achieve that (I just saw your post in the P2P thread).