I would love to hear your thoughts on the following

Here is the context: after selling my company, I will receive in the next couple of weeks around 1M CHF after tax. I will start a new job with ~300k/year. I already have 700k VT via IBKR, 20k cash, and 3rd pillar maxed out.

In addition, I have a mortgage of 200k (0 amortization) at 0.75% associated with an apartment I am renting out. After tax+mortgage interest, the apartment is generating 15k. I will need to renew the term of the mortgage in 6 months, and I expect the interest to decrease further from what I see now ~1.5%

Finally, I’d like to eventually buy a house in the next couple of years, but I expect I would need less than 300k down payment.

Now that the whole context is set, I am wondering what to do with this ~1M. How would you handle it? I think it makes sense to keep something like 100-200k for a potential down payment and invest the rest.

Multiple directions I see (that are not mutually exclusive).

Put all into VT at once. Then discussion closed.

Since VT is quit high and there is some irrational fear, split the amount in e.g. 12 months and invest each month (still significant amount of money).

Put some of the money in an high-interest account without too many constraints (especially if investing over a period of 12 months). It seems that Yuh gives 1% without any upper bound and allows large transfer. Maybe it is worth it to split among multiple banks with 100k each. However, I should be able to move money whenever I need (e.g., IBKR) without an upper limit or 3 months notice.

Use bonds for the 100k-200k to keep.

Pay the mortgage entirely and have 0 debt. Also theoretically, having this mortgage of 200k generate quite some cash.

Would love to hear your thoughts! Thank you for your time!

Depending on canton, your income and wealth tax could be quite high. I’d be tempted to make large extra payments into pillar 2 pension over several years and get 40%+ of tax back as well as shelter from wealth tax.

With a house purchase on the cards, you have a way to get this out again in the future.

If you have a lot of pension capacity, you could easily put 200k+ each year into it and get 80k back in taxes each year for several years.

Your current asset allocation seems to be following

700 K Stocks

1 M cash

200 K debt

Some cash for normal expenses

In my view the debt is not very high compared to rest of the assets. So the main question to answer would be to decide what’s the best asset allocation for your risk tolerance. Focusing on 1.7 MM portfolio

If you intend to have any portion in Bonds then it might compete with your debt interest and in that case it might be better to pay off the debt before investing in bonds. CHF bond funds have 1.1-1.2% yield to maturity at this moment.

However if you seek 100% equity portfolio, then reducing mortgage would reduce your potential returns.

Carl said to succeed as an individual investor, it is important to focus on the right principles rather than getting caught up in constant market shifts. He shared how he initially struggled with constantly changing investment strategies despite having the best training and working for top firms. Over time, he realized the solution is not about constantly finding better funds but about sticking to a plan that aligns with your personal goals.

The key is understanding why you are investing the way you are. Many people base their choices on tips from friends, articles, or industry familiarity, but these are not acceptable places to determine how you invest. Richards suggested that the correct approach begins with defining your values. Your values then inform your goals, and those goals should drive your portfolio decisions. In essence, you should ask yourself, “What am I trying to achieve?” and “Why do I want to achieve it?” before even thinking about specific investments.

(there are more details in the actual interview)

Woaw, so many responses already, thank you to everybody!

I merge those questions together. @Dr.PI (cannot put a third link)

Thank you! See below.

Age: 32, 2nd pillar 100k, 3rd pillar 90k and retirement goal unspecified but for sure not 60+. As long as I’m happy to work, happy to continue. I’m actually based in Schwytz. I’m more interested into the FI than the RE part. The day it changes, I’ll focus on something else

True I could rebuy some 2nd but it’s “only” 106k, nothing more. But in any case, it will be able to use this amount after exactly 3 years right? Or you mean something else by “extra” payment?

Thank you for your thoughts! 1.1-1.2% yield to maturity is not so great compared to some saving accounts. Might not be worth it.

I don’t mind to have 100% equity. My only concern is that if I need to get some down payment (assuming that 2/3rd pillard can be used at max 10%), I don’t want to sell stocks if it is a bad time.

You are coming from 700k in broadly diversified stocks and 1M in a highly concentrated stock position in an private ultra micro-cap company.

The change from this 1M to cash is a big reallocation. I would assume its value had more in common with local micro-cap (some sector) stocks than CHF cash.

Logically, it should be replaced by something similar immediately. Then the question is, what is your target asset allocation?

If it is not

Asset

Amount

Global Stocks

700’000

Local micro-caps

1’000’000

Apartment

???

Mortgage

-200’000

then you should roll from there (maybe over your 1 year time frame).

But taking a cash position now and slowly rolling back into stocks strikes me as active market timing. Which can be good, if one knows more than the market, but most of us don’t. Then time in the market beats timing the market.

Some of the best leverage one can get. If you don’t intend to hold cash (and maybe also not bonds), but want real estate, this is a good short position. I personally would take more, but not everybody is comfortable with owing money.

Why? That likely wasn’t an allocation they had any control over. Now that they have a liquidity event they can go to something more diversified, matching their risk profile.

They have a big pile of cash now, if they sleep better getting more slowly into the market there’s nothing wrong with it (it won’t make a massive difference over decades, and if they feel bad/second guess themselves because the market crashes right after their lump sum investing it might be worse long term)

Always true, but not necessarily rational or good for profit.

What exactly is unclear about the forced (temporary) cash position being a material reallocation? Immediately converting it back to a similar but more diversified stock allocation is less of a reallocation.

It is also less dependent on being able to time the market. Retail money is known for generating negative alpha with their market timing decisions.

1.7 million in VT will provide you with around 35k per year, growing and more or less inflation-adjusting by itself. While it sounds like a lot of “money for nothing”, it won’t be enough to live in Switzerland without an income. So, an emergency fund in highly liquid savings account (Yuh would be my first recommendation) looks prudent.

There are hardly any situations where paying into 3a and investing these funds into the stock market is not advantageous. All in all, finpension 3a offer seems to be the best one, followed by True Wealth and VIAC.

Considering your age and location, I don’t think paying into the 2nd pillar makes much sense for you. This is up to you, of course. It might save you some taxes if you cycle your downpayment through the 2nd pillar before using it to buy self-occupied property. However, it might be not sufficient to bother and risk ending up on the tax authorities’ radar as a “clever guy/gal prone to tax optimization schemes”. Schwyz tax authority seems to like to dive deep into resident’s situations, according to some feedback.

Same with the mortgage repayment: the interest is tax deductible, but it shouldn’t affect you much. So anything will do: from reimbursing it completely to borrowing more and investing it. In the latter case, your portfolio should be more aggressive than 20% fixed income, otherwise it doesn’t really make sense. Note that you can take mortgage any time, if you have none.

If you do want to “build a real estate empire”, like some investors like to: well, you can’t withdraw funds from the 2nd pillar to finance RE that is not your primary residence.

To conclude, with this wealth and income at your age you have to do something damned wrong, such as falling onto an outright scam, to not be ridiculously rich in 10-20 years.

Oh I agree with first trying to answer that question for themselves before putting together an investment strategy. Nonetheless a contender for “well that escalated quickly” meme

What’s the point of locking away money from the “big pile” when you could use it more proactively for freedom? Better to invest it slowly into post-tax markets, and if you must fill the hole in pillar 2, do it from active income over the next few years.

Can somone explain to me how a 31 year old with 300k yearly salary and approx. 1m cash can buy into the 2nd pillar 200k+ yearly?

Does not the „Pensionskasse“ determine how much somone can re-buy into it? Can anyone suggest me a video so i can learn when it makes sense to reinvest into the 2nd pillar? I‘m 26 years old currently and want to know how this „gap“ emerges over the years if you have a salary over 140k yearly without taking it to buy real estate.

Following is only applicable to defined contribution plans. Defined benefit plans work differently

This differs from fund to fund . But in every pension fund regulation, there is a table which states how much max money the fund can have by age of insured person, there pensionable salary and selected plan.

As you grow older, this number increases

Potential to buy voluntary into 2nd pillar = Max money allowed - Current value of fund

It all depends how long you have been contributing, what have you already bought in etc etc.

In general the gap emerges because the fund would like to assume that if you were always working in the same company at the same salary (= your current salary ), how much money you would have accumulated over this period including some sort of interest. But obviously no one start working at same salary and keep it forever. In addition people have gaps due to unemployment etc

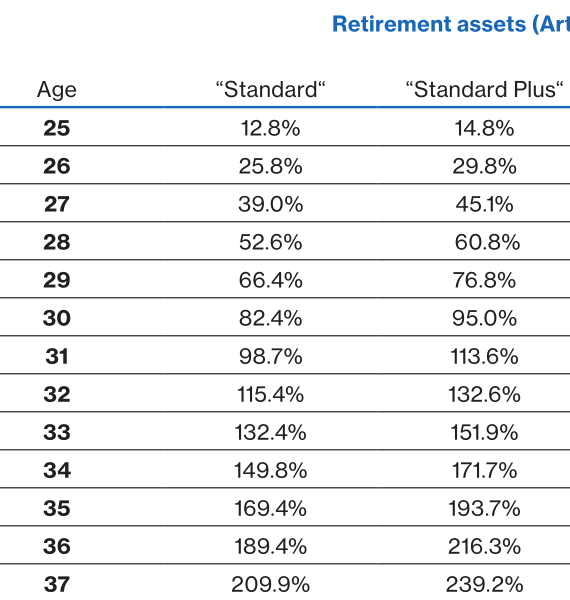

You can contribute up to 132% of your salary at age 32. So if you have a 300k salary, that is 396k. Since OP only has 100k in the pension, he can contribute 200k extra.

If he fills it up, next year (assuming no pay rise) he can contribute an extra 60k. Since OP is not so old, he doesn’t have so much pension capacity yet. But maybe salary/bonus will increase.

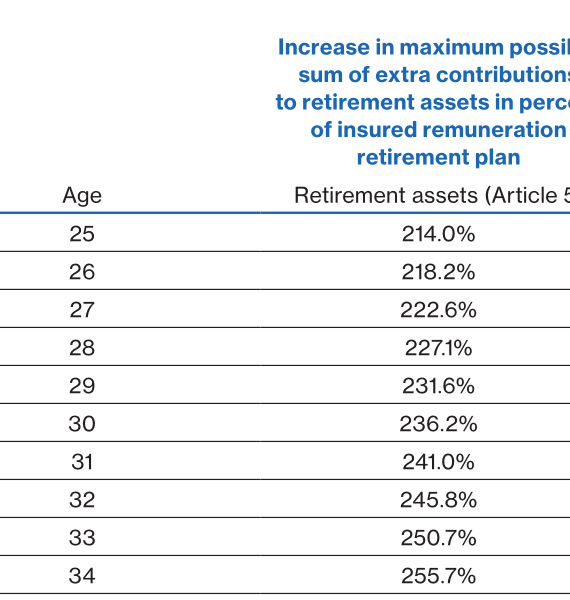

Then your plan might have extra for early retirement so then you have more capacity:

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.