I’m temporarily leaving Switzerland and need to park my LPP vested benefits in a low-risk libre-passage account for about 1 year. No withdrawals planned, just safe parking before new job.

I already have a finpension 3a account (happy with it), but I’m wondering if there’s any real advantage to using finpension for LPP too—or should I go with VIAC instead? Classic banks are out (low interest + high taxes/costs).

Priorities:

Very low volatility (cash or short bonds only; no equity exposure given short horizon)

Low fees

Easy transfer later

VIAC or finpension? Other hidden gems? Experiences parking LPP short-term?

Won’t a bank LPP with ~0% and no fee be better for this use case? (ZKB has no fee, PF has 36 CHF per year, etc)

Edit: and if it’s just a year, how long before your current pension funds sends the fund to the default foundation? For my previous fund, that was 180 days.

(That’s a few extra percent of remuneration with no risk since they usually pay the LPP minimum)

Is it really worth it? If stock does +10% next year(that’s fairly optimistic), you do 0.5% on your portfolio. (And non 0 odds to have 0 or negative instead)

you will not get any kind of yield with short bonds/cash, with any provider. SNB rate is 0% and that will basically determine any kind of cash yield for all providers.

So go to the one where there is the lowest cost for just holding cash.

You’d need way longer term bonds for any kind of yield (and even that is ultra low), but for your horizon that doesn‘t make sense.

Probably a bank with no custody fee and cash will be your best bet.

With the Account Plus «Global» 95% of pension assets are held in the account

at a preferential interest rate of 0.05% per annum. The remaining 5% are

invested globally and broadly diversified in equities

Personally what I’d do is stay at current fund for the longest of the minimum 6 months allowed by the law (which could be up to 2y) and then switch to Home - Stiftung Auffangeinrichtung BVG, assuming the interest rates for 2026 are >0.

Doesn’t Finpension charge their fee on the total amount incl. cash? That’d make them particularly bad for parking. Further, they charge 400 CHF fee if you transfer it out within 1 year.

Mine is unspecific: “earliest 6 months, latest 24 months”, which happens to be the wording of Art. 4 of the law (FZG).

So I’d just ignore any reminder, leave it where it is as long as possible and either go via Auffangeinrichtung or transfer to wherever there’re no fees or you already have an account (and similar interest).

Before I pull the trigger, could you please do a quick sanity check on my reasoning? I want to make sure I’m not missing any hidden details.

Based on the discussion, the choice for my 1-year parking is between the Stiftung Auffangeinrichtung (AEIS) and VIAC (specifically the “Account”/Cash strategy).

Here is how I see it:

Costs: Both appear to have zero fees for opening, account maintenance (on cash portion), and transferring out to a new employer’s pension fund in Switzerland later.

Returns: Interest rates on cash are negligible for both (AEIS is ~0.40% for 2025; VIAC is similar).

Flexibility (My deciding factor): Since I am currently living in France, VIAC seems superior because it is fully digital. AEIS feels more bureaucratic/paper-based.

Bonus: If my 1-year break extends unexpectedly, with VIAC I can instantly switch strategy to invest in equities via the app, whereas with AEIS I’d be stuck.

My plan: Open a VIAC vested benefits account and select the “Account” (100% Cash) strategy.

My Question to you: Is my assumption about VIAC costs correct? Specifically, are there any hidden fees for a 100% cash strategy (e.g., negative interest on cash > X amount, or closing fees) that would make AEIS strictly better than VIAC for this short timeframe?

For a 1-year term, the only “safe” solution is a vested benefits savings account. Even a bond or money market ETF has a fluctuation risk.

Viac and Finpension offer vested benefits savings accounts, but both pay lousy interest (Viac pays 0.05% and Finpension pays no interest and charges you a 0.49% fee to boot!).

Unfortunately, leaving the money with the current pension fund isn’t an option. My former employer is pressuring me to close the account and transfer the funds out by next week, so I need to execute the transfer immediately.

Thanks for the heads-up on the interest rates. You are right:

• VIAC pays very little on cash (~0.05%).

• Substitute Occupational Benefit Institution (AEIS) pays 0.40% for 2025.

• Finpension has fees that would erode the capital on a cash strategy.

My Decision:

Given the strict deadline (1 week) and the fact that I’m handling this remotely from France:

I will likely go with VIAC strictly for the speed of execution (instant IBAN via App) to satisfy my ex-employer immediately.

While I realize I might leave ~250 CHF on the table compared to AEIS (0.40% vs ~0.05% on ~80k), the digital convenience and instant setup are worth the “cost” in my current situation. Opening a traditional bank account or dealing with paper forms from abroad might take too long.

I’ll proceed with opening the account today. Thank you all for helping me navigate this!

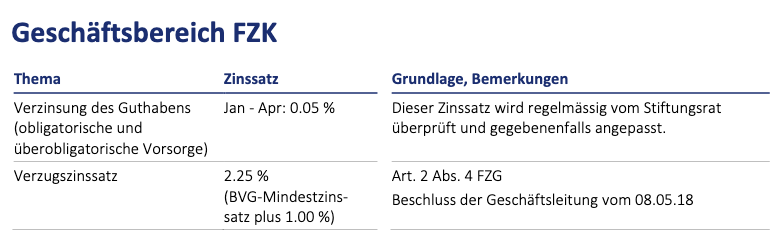

OK, didn’t (only) come to make fun of you, but to help your decision, current 2026 interest at AEIS is Geschäftsbereich FZK - Verzinsung des Guthabens (obligatorische und überobligatorische Vorsorge) 2026 Jan - Apr: 0.05% (thereafter they don’t say yet, but the trend is down…)

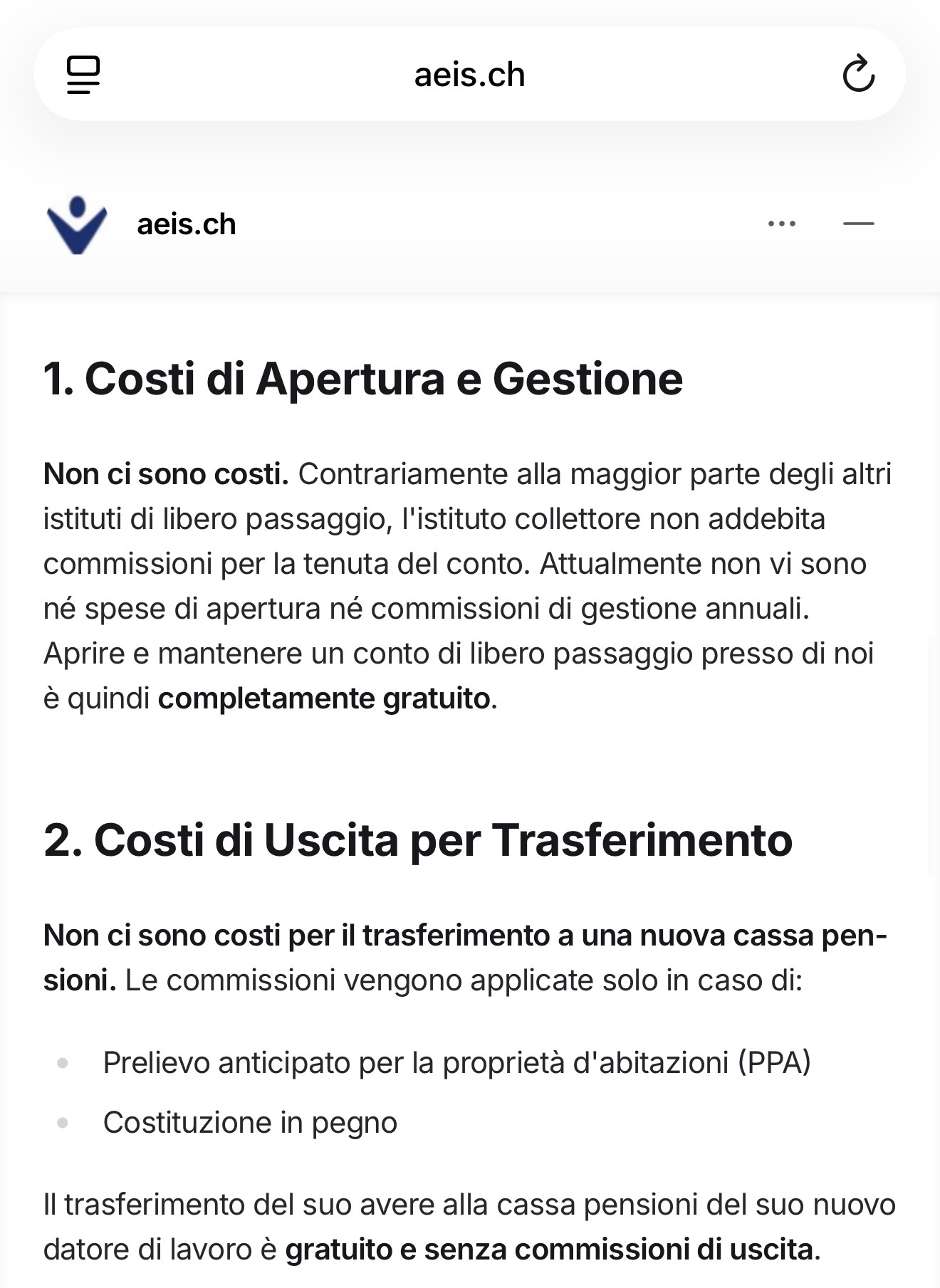

Verrechnet mir die Stiftung Auffangeinrichtung BVG Kosten?

Die Stiftung Auffangeinrichtung BVG verrechnet gegenwärtig keine Kosten. Ausgenommen sind Kosten bei einem Vorbezug bzw. einer Pfandverwertung oder einer Verpfändung für den Erwerb von Wohneigentum zum eigenen Bedarf

I decided to query the official AI assistant on the aeis.ch website to get the latest facts, but the answers I got are in complete contradiction with some of the comments here. Now I am confused about who to trust.

I am attaching the screenshots of the chat with their official bot below.

The contradictions:

On Interest Rates:

• Forum consensus: “Likely 0%”.

• AEIS AI (Screenshot): Claims the rate is fixed at 0.40% for 2026.

My Question to the Community:

How much value should I place on this AI response?

Has anyone opened an account recently (voluntary basis, not forced) and can confirm if the AI is telling the truth?

I’m trying to figure out if the AI is “hallucinating” / quoting the wrong document.

If the AI is right, AEIS is mathematically the best option (Free + 0.40%). If the AI is wrong, it’s a trap.

The yearly interest from January to April 2026 is 0.05% according to this document. The interest after April 2026 is not yet published. See screenshot.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.