For what it’s worth, you get the same exchange rates on other Swisscard cards (which are then 2% more expensive PLUS up to 2.5% foreign fees)

1 Like

I have Wise, not Revolut so cannot compare them.

Currently the Wise fee for EUR to CHF is 0.423% and CHF to EUR is 0.23%. These percentages get deducted from the amount you are transferring, the reminder is then exchanged at interbank rate.

The app shows you the details of all this before you finalize the transfer.

Wise periodically changes the fees, but the EUR-CHF pair is quite stable. There is no change whatever the amounts transferred per month.

Edit: forgot to say this is for exchanging between wise accounts, when you transfer to another bank, you might have some additional fees, last time I paid 1.34 CHF to transfer CHF funds from Wise to UBS, seems to be a per transfer fee

1 Like

Unless I am missing something, that means ultimately it is not really different from the Cumulus card. No additional FX fees but horrible FX rate, but you would still get Cumulus Points.

Revolut does the same if you have local currency balance or not, it will convert automatically your payment

UBS used to have all their cards (debit or credit) integrated into their budgeting/spending classification tool.

Which… when you have one provider for the account, another for the international card, and a third for the daily spending… just gets time consuming.

Maybe interesting:

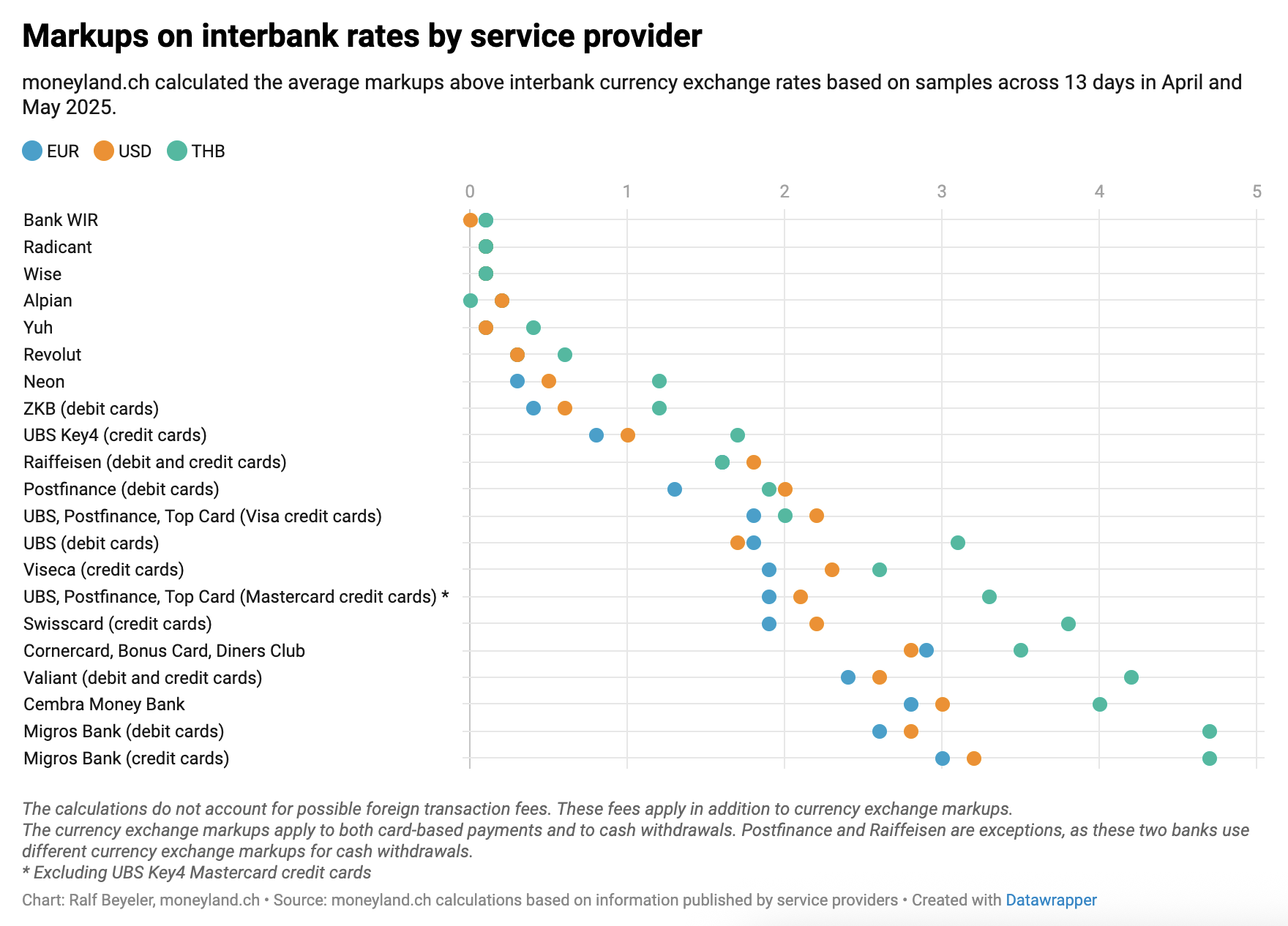

Based on samples across 13 days in April and May 2025, Moneyland determined the average markups above the euro, US dollar, and Thai baht interbank rates published by Oanda. The WIR bank, Radicant, Wise, and Yuh all have very favorable currency exchange rates, with markups of 0.2 percent or less. (..) The calculations do not account for possible foreign transaction fees.

8 Likes

I would be careful with this table that only show markup on interbank rates but doesn’t take into consideration the FX fees…

For example Yuh with 0.1% is completely wrong because they didn’t count 0.95% of basic fees.

7 Likes

Yes and no. I think the point was to figure out the markup only, which is hidden. The fees also apply but they are transparently reported.

1 Like

Correct! But that is exactly what is mentioned in my quote and under the graphic ![]() . But yes, with fx fee yuh looks really really bad.

. But yes, with fx fee yuh looks really really bad.

2 Likes

To be fair/frank, the only number relevant to a person using the service (AND actually also to the service provider) is overall cost, so reporting part of a price is at best useless and would at worst be considered misleading.

(Of course you could report all of it in a comparison of what makes up the prices, though this doesn’t seem to have happened in this presentation.)

1 Like

I agree.

I don’t understand how a chart can be misleading because additional fees are missing when this is stated in the title, in the description below, and in the article text. The author’s idea was to find out how much thes cards deviate from the exchange rate … Or: How much the advertised FX fees are misleading, because there are still hidden surcharges on the exchange rate. But if you click on the source, you will find a table that also includes the FX fees ![]()

I think the author has done a good job. Very few online comparisons make this effort.

7 Likes

I can confirm from this post almost 6 months ago, the top credit card from a non-neobank in Switzerland is definitely UBS with their Key4 option, with 0.5% markup on the Mastercard rate, albeit they have monthly fees, but come with KeyClub points to be redeemed as CHF.

1 Like

Do you consider Wir a neobank?

Edit: you’re talking about credit cards, not debit card. So just ignore my question.

TopCard is changing the conditions for the Supercard credit card. The 1.5% foreign transaction fee will no longer be charged from May 11th, 2026. Instead, they say the fee is now “included in the exchange rate” to make payments abroad more “enjoyable” and “transparent”. This means:

-

Payments in CHF abroad are now free and still earn 0.33% cashback

(e.g. airline tickets or CH online shops that process payments abroad) -

The exchange rate for foreign currencies might be worse than before,

but it’s not clear if or how much it has been increased to include the fee

So the Supercard credit card is now comparable to Cumulus for the first bullet point above:

That’s the opposite of more transparent, no?

7 Likes

Correct, and by a far far margin

If they publish the exchange rate markup somewhere, I would actually consider it more transparent. The reason is that you won’t ever get surprised anymore by extra charges on online CHF payments that happen to be handled outside Switzerland (which should be illegal, in my opinion, because of the lack of transparency). And only one markup is clearer than markup + fee.

If they don’t publish the exchange rate markup anywhere, it’s indeed not exactly transparent, and annoying as you have to rely on e.g. moneyland testing the markup.

However, I consider the nontransparent CHF fee completely unacceptable. I categorically don’t use cards with such a fee (which is why I use UBS key4). So the dropping of that fee is definitely an improvement in my book. And unless they published the markup in the past and now stop publishing the markup, it should be strictly an improvement (assuming new markup is not higher than old markup + fee).

The current factsheet (based on the old approach) says “Der Devisenkurs beinhaltet einen Aufschlag. Dieser kann beim Kundendienst erfragt werden.” Not ideal but if support indeed answers that question (and will do that also in the future), it’s not terrible - obviously depending on high the markup actually will be.