Interesting. Are there explanations as to why the cost depends on the currency?

I only use Radicant as a payment card and usually don’t keep more than 10k there. But even then: I assume that Basellandschaftliche Kantonalbank (BLKB) will wind down Radicant properly in the event of closure or insolvency, and in any case, you are insured up to CHF 100,000.

3 Likes

No, unfortunately not. I have actually contacted Wir twice and they were not able to tell me why because it’s Mastercard that sets the exchange rate. Maybe because exotic currencies have not that high volumes… I don’t know. Anyway, for me Wise remains the cheapest option at the places where I am most of the time!

Mastercard exchange rate definitely has higher spread for more exotic currencies (and iirc 0.5% for major ones)

Yes, that makes sense. In that case, Wise and Revolut might have their own currency conversion system (not relying on Visa or Mastercard) for which they can apply their own pricing.

What makes WIR a lot better than Neon?

It would seem that it’s pretty hard for anyone to do much better than Neon (free account, WISE for international payments).

Neon isn’t free anymore for best fx.

WIR is all free and better fx rates than mastercard rates (EU for sure, but used also in Bosnia and Serbia).

The downside so far compared to neon: the purchase via card is shown 1-3 days later on the account, but is shown in the separate SIX card app. In e-banking you see it under account > disponierte Beträge (there at first with the mastercard rates, then when booked you see the better (I suppose) interbank rate which is almost always lower).

The 2nd downside: you have 3 apps (one for authentication).

Neon uses wise for transactions abroad with a price tag not sure if cheaper than WIR.

I calulated some times ago the break even of neon plus; I think it was ca. CHF 5.5k.

So, spending less than this circa CHF 5.5k a year, an upgrade does not make sense.

But I think, the offering of WIR is definitely more sustainable since it is a bank with enough funds (and therefore not dependend from their mother as Radicant or Alpian).

Since I managed to link my neon mastercard with various streaming online services and I should not unlink the card, I “have to” stay with neon, haha.

2 Likes

I change Forex at Interactive Brokers and then send it already converted to my wise account. I have 3 phisical accounts there for CHF, EUR and USD. For cash takeouts I use a free DKB account in Germany.

Using the wise card charges you automatically in the currency you use if you have a credit in this currency. You can get a physical card or create virtual ones for your phone or your watch. DKB gives you a free account and a free debt card with free unlimited cash takeouts.

I am a long term client of IB. As IB is by a big difference the cheapest place to exchange currencies they don’t like to be used just for that and may close your account if you only use it for Forex exchange.

4 Likes

Why focus so much on Wise while Revolut is so much better for international transfers, and better than Neon for international payments

Revolut may be a bit better for major currencies on weekdays as long as you’re within the monthly limit. I prefer Wise where I don’t have to care about the day of the week or any limits. It may not always be the cheapest but it’s pretty much always reasonable, as far as I know. Keeping it simple.

That said, for card payments, I’ve actually switched to a UBS key4 credit card, which makes things even simpler to me, as I don’t have to manually transfer any money in advance and I can use a single card across the world for nearly everything. The main exception being ATM withdrawals but that’s something I no longer need regularly (and I still have Wise and also Revolut as backup).

1 Like

Not having a key4 in my wallet anymore is one thing I actually miss about changing away from UBS ![]()

Hi, are the FX fees good for traveling? Or did you choose Pro or Prime accounts? Thx

1 Like

Depends on the country, and has also changed over time.

India was for long time not possible with Revolut, while with Wise you got a real good deal.

Revolut is getting better there though, especially by getting the relevant banking licenses/partners (I guess)

Since you’re discussing Wise and Revolut, is there a straight forward answer to which one is better if I wish to transfer 3k / month from a Swiss bank to DKB for say a year?

(I don’t have either at the moment, wouldn’t mind subscribing to one of their options if that helps.)

**Edit: Seems like they actually do have a considerable exchange rate markup, as highlighted by @xmj below.

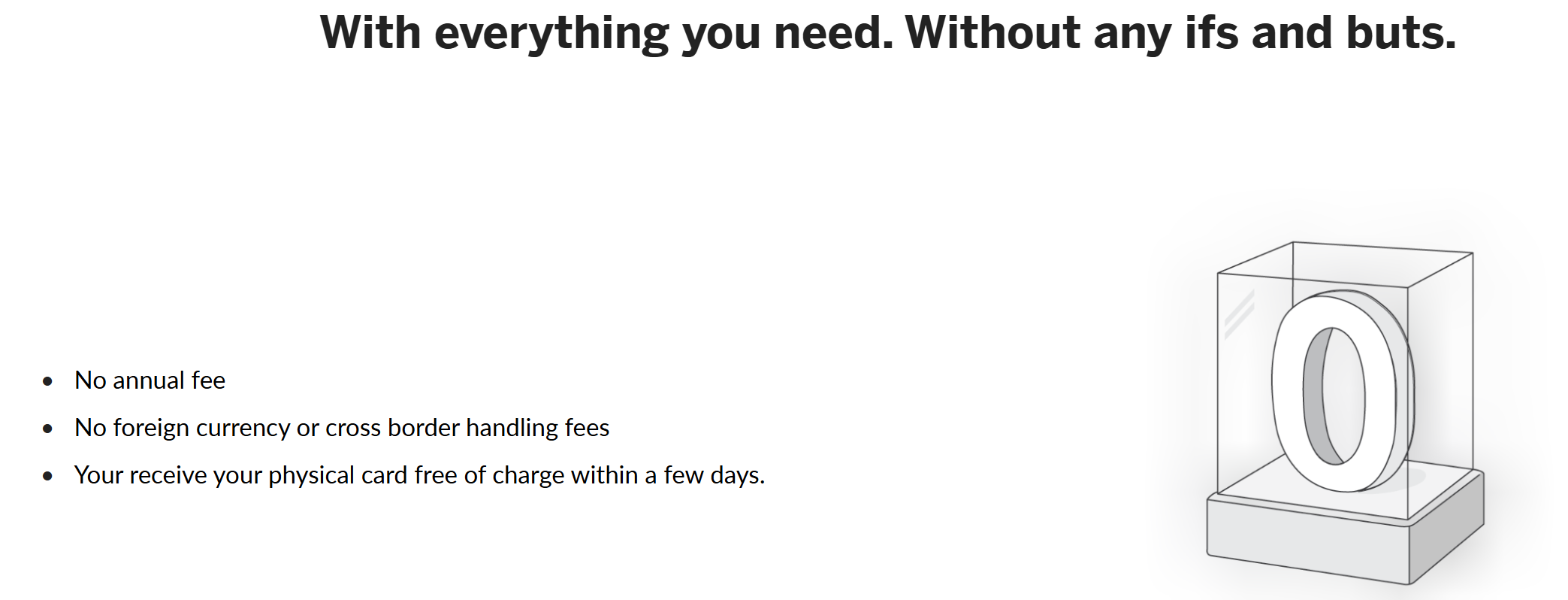

There is also a new Swisscard credit card that claims to have “no foreign currency or cross border fees”. This card doesn’t have cashback like some of the other popular Swisscard credit cards, but it could be an attractive option for a real credit card (not prepaid or debit) abroad.

I dug a bit further and from what I’ve found, the (Visa) card would use the Visa Exchange Rate without a markup of Swisscard but it is not that transparent either*, so before getting one, I suggest to directly ask them.

If these claims hold, this would be a very attractive option for many.**;

*if a card starts with “3758” its a different exchange rate according to the disclaimer after entering some values in the calculator; whatever that means

1 Like

key4 cards use the Mastercard rate with a 0.5% markup (but no additional foreign country markup). This is slightly worse than Neon but I do get 0.4% back in KeyClub points with key4 premium (0.2% with key4 standard) - also on CHF payments where there is no markup, of course.

2 Likes

Careful here. Just from the link you posted the EUR/CHF exchange rate e.g. for last Thursday is 2% higher than spot Forex rates.

2 Likes

You can pay 110chf for one year of Revolut Premium, no exchange limit (free is limited to 1250chf/month then you pay 1%). With Premium you can have some other things like Perplexity Pro or VPN, etc…

I have no idea about Wise, sorry.

1 Like

You’re right; I edited the post above. I misinterpreted the

The exchange rates for foreign currencies used are set by the issuer. They are based on the usual market sources and rates from card networks.

as based on Visa (“card network”), even though they likely mean themselves with “issuer” and put their random markup on top. ![]()

2 Likes