I was looking into the numbers of becoming landlord in Switzerland and I found this example:

(Source: The bliss or burden of letting you can change the language to DE/FR/IT)

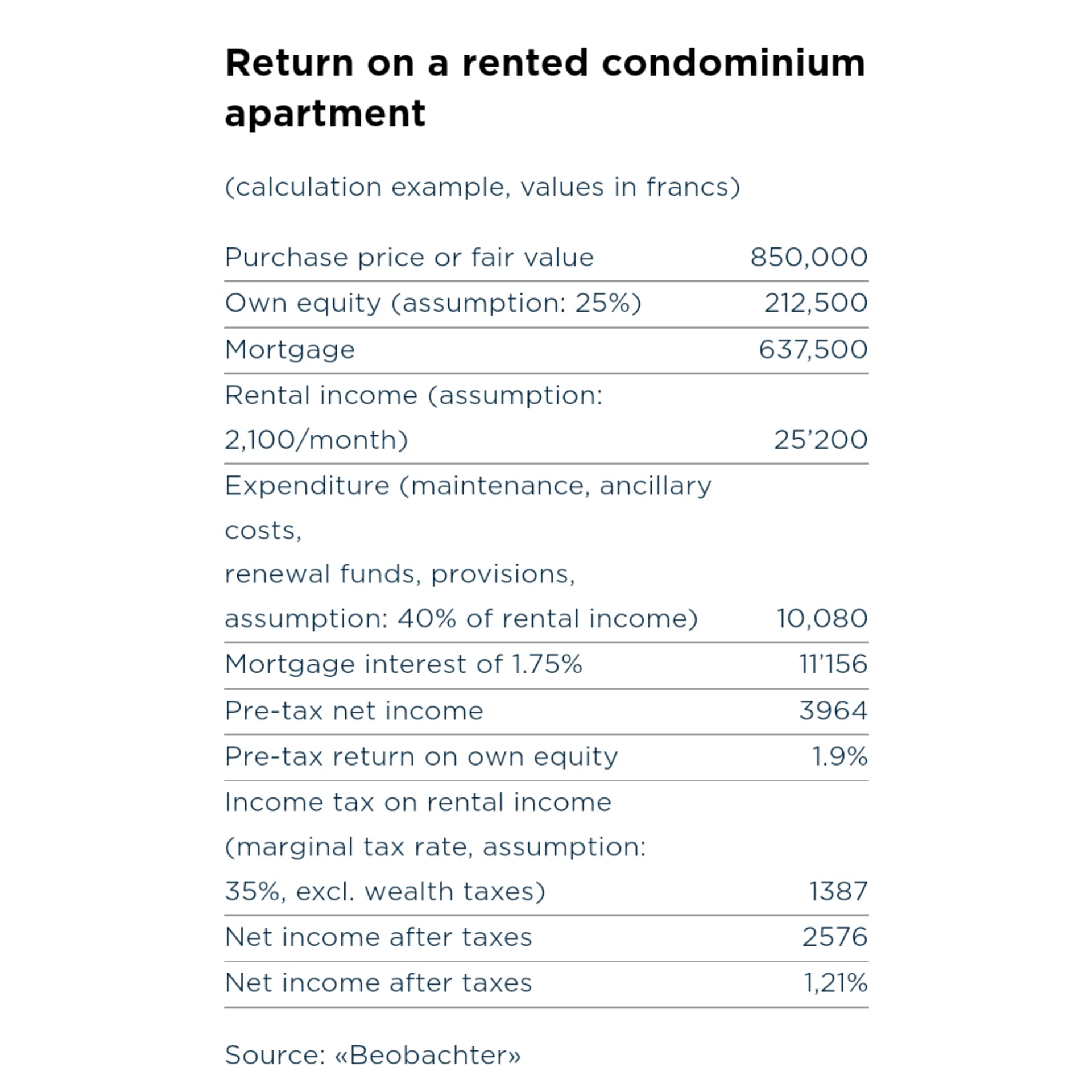

Considering that there are some factors not considered on the example like, position of the unit, size, etc. I found that a additional 2.5k CHF a year in a personal cash flow for an investment of 210k CHF to be quite low. I was wondering if some mustachians investing on real estate can confirm the numbers?

I understand that the value on real estate is generated over time with the grow value of the property but I found difficult to believe that the benefits on teh cash flow are so small. Maybe I am naïve.

Let’s say I would like to live out of it and my need will be an income of 100k a year. In this case I would be required to own around 40 apartments!!

Also to buy the first unit, as I am not gonna live on it, I can not count on 2nd and 3rd pillar money as this money is just for your personal house.

That makes 2% ROI on invested capital, not too bad for RE.

Basically the main leverage in RE is buy cheap. And in CH it is really difficult for the moment. Even junk which needs renovation go away for prices beyond reasonable.

Yes, an this is why we discuss the “rent vs. buy” and can’t find a real solution.

To gain 2.5k/Year you make a massive (leveraged) deal and hope that the value of the unit rises.

I find the maintenance costs assumption incorrect. 40% of rental income, on which basis? It can be much more, if it is an old property, or much lower for something new.

I am not sure that you are right on this point. As a Swiss resident, you will have to declare your wealth on your global wealth, not only your Swiss wealth. And since wealth tax is not levied in Germany (non existent for now), I think that Swiss tax authorities will tax it as Swiss wealth.

Since there are no capital gains in Switzerland, this is not appliable anyway ?

However, I think it is possible to buy RE on 0% financing if you prove your project is cash flow positive, so you might be able to leverage the crap out of it. And in some areas, it might be still possible to get RE on a discount, but you have to be sure that the demographic bomb will not hit too hard. Some rural areas are at a real risk to die out (like it already happened in some parts of rural France).

You are 5+ years too late for this one. Yes, some German banks might still finance 100% or even 110%, if the apartment/house is cash flow positive. The problem is that you can hardly find any such property anymore, unless you go to really crappy areas where you can get a gross return of 6+%.

I looked into it already 5 years ago and went to some meetups. Already back then, it was risky from my point of view. Now that the prices have even more skyrocketed, I wouldn’t touch German real estate. Especially with such a high leverage like 100%.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.