I am not sure what you guys are trying to do. Are you trying to protect against inflation, or buying equity securities that behave like bonds?

The two are really different.

As you know, the value of any asset is the sum of its cash flows from now until judgment day, discounted to today’s value.

Bonds

For bonds, the process is quite simple:

- Provided that the bond issuer does not go bankrupt, the future cash flows are contractual and are unaffacted by inflation.

- However, the discounting rate will likely increase with inflation. As an example, take a 15 year bond with a $2000 principal borrowed and a $100 annual coupon. If the discount rate is 5%, the bond is worth $2000. If the discount rate goes up to 7%, the bond’s value is now $1’635 => the bond has lost 20% of its value. Bonds are very fragile against inflation.

Equities

For equities, there are a lot more moving parts. The value is still the present value of future cash flows discounted to today, but the future cash flows have many components.

The free cash flows will be mainly affected by three factors:

-

The ability of the company to raise its prices without losing volume of sales: doable when the company has a strong pricing power (for instance, a brand people are willing to pay for. Not all brands are created equal: you are willing to pay more for a Coca-Cola than for a Klutz-Cola, but you won’t pay more for a Sony Blu-ray player over a Kenwood one…). However if the company operates in a competitive environment, that won’t be possible.the worst case being a provider of a product or service where the only differentiator is the price, i.e a commodity industry. The higher your pricing power, the less you are impacted by inflation.

-

The costs incurred by the company, mainly raw components and labor. While everybody will be impacted by inflation of these costs, the impact on profits will not be the same for everybody - it depends a lot on your margin profile. At fixed sales, if your costs represent 90% of sales (i.e a 10% margin), if costs rise by 1% of sales, then your profits are now 9% of sales instead of 10% → profits dropped by 10%. However, if you have really good margins, for instance 40% margins, if your costs increase by 1% of sales, then profits are now 39% → the drop in profits is only 2.5%. The higher your margins, the less you are impacted by inflation.

-

Finally, free cash flow are impacted by maintenance capital expenditure, i.e the investment needed to make in order to stay at the same level of profitability. Your assets (factories, machinery, etc) wear and tear and need to be replaced after some time. The more you are relying on tangible assets to generate sales (example: mannufacturing, utilities, etc), the higher you will need to pay to replace your assets in case of inflation. Most of your profits will just be consumed by the cost of replacing your assets. The less you rely on tangible assets to generate sales, the less you are impacted by inflation.

-

Finally, inflation tends to increase the discounting rate, same as for bonds.

So in the case of equites, if you want to protect against inflation, you want to buy companies with high profit margins, lots of intangible assets (instead of tangible ones), and with pricing power strong enough to counteract the effect of an increased discounting rate.

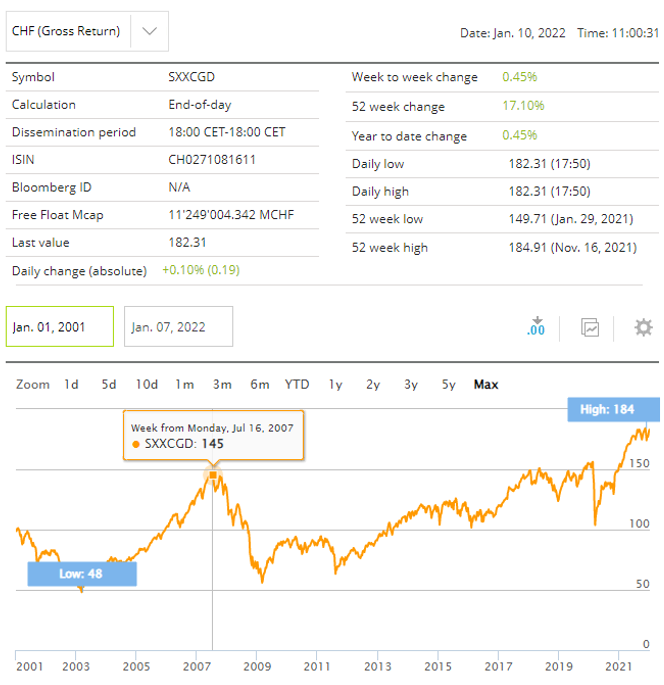

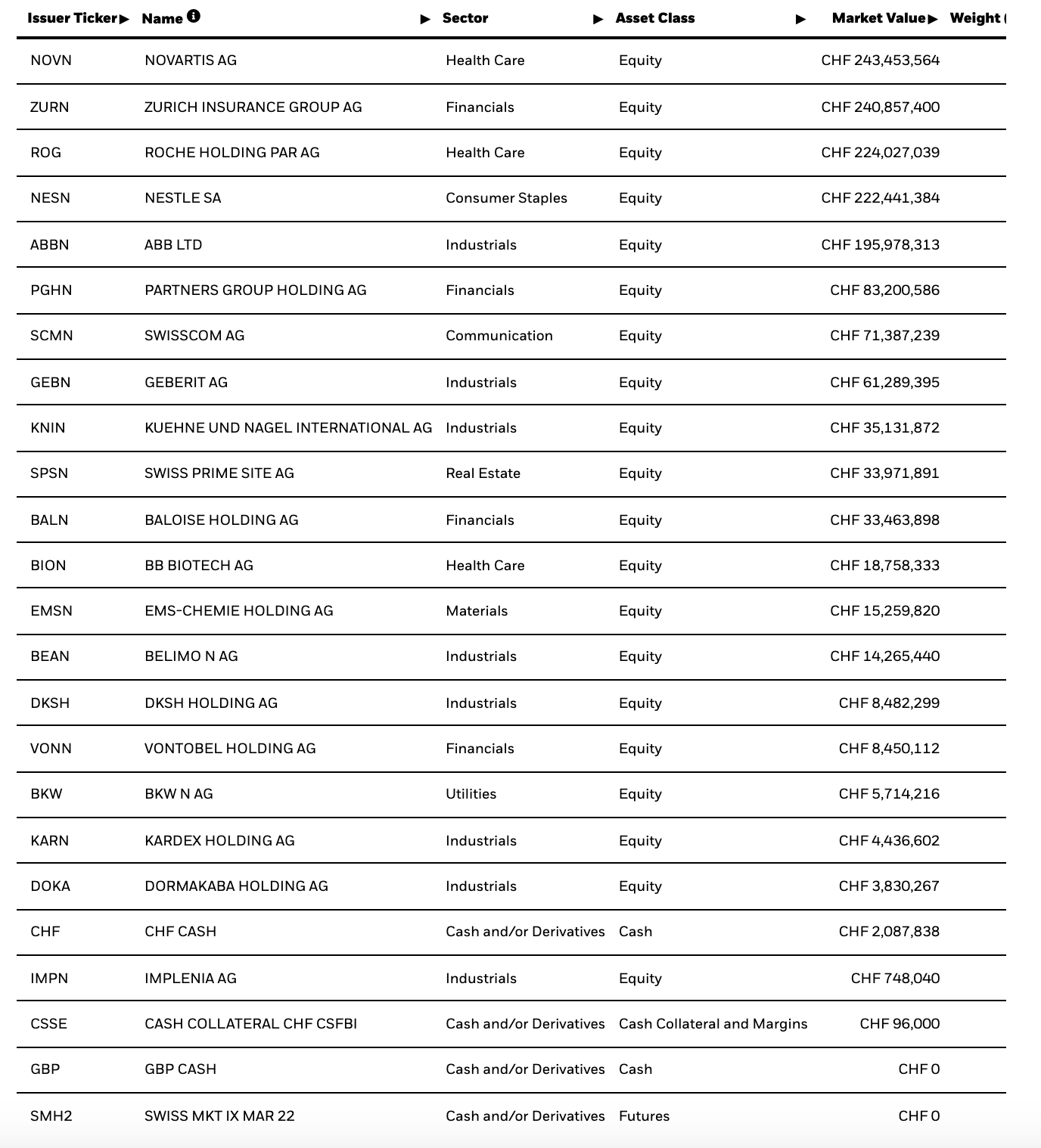

Now when I see companies like Swisscom being suggested, it is true that they behave like a bond. Sales have been flat over the last 10 years, as did profits and dividends. Capital expenditure is high, and combined with flat sales it means that most of the profits are gone into replacing the assets to just keep afloat. In other words, the only thing going to the owners are the dividend - retained earnings are never going to add any value. So it behaves like a perpetual bond, with the dividend being the annual coupon.

And like a bond, it will be smashed by an increase in interest rates. Stable, bond-like equities will not protect you against inflation. You will get your regular dividend, but the principal (i.e the share price) will get hacked.

EDIT: Actually in the case of Swisscom and similar businesses, the case is quite easy to compute. Those businesses are functionally equivalent to perpetuities, so the value is simply the dividend dividend by the discounting rate. So let’s say the dividend is 1 CHF and the initial discounting rate is 5%. The value of a share is then 1/0.05 = 20 CHF. But if the rate raises to 7%, the value becomes then 1/0.07 = 14.3 CHF. The share would lose 30% of its value.