Haven’t paid attention to the geographic / FX split in my portfolio and realized that I had gotten far lower on my CHF denominated stocks than I wanted so am looking to write some puts on Swiss stocks in the coming months to get some premium income potentially leading to a position. Am curious if there’s any posters with any high conviction on certain Swiss stocks (in particular: good div yield ones)? I still have a decent position in Novartis but that’s about it.

Why not buy a Swiss ETF?

I would buy Julius Baer

A complete different topic and rather simple question, still related to “Stockpicking”:

Banks/Analysts publishes ratings BUY/HOLD/SELL for stocks. Has anyone try to use those ratings to create a trading strategy?

Tempting to create a strategy with those recommendation. But, of course, selling on strong buy and buying on sell.

But then analysts don’t live in a cloud; they may be wrong, actually they are wrong more often than right; but they may not be wrong alone. Meaning they will not recommend a really good stock until all the others do the same… and then it is too late.

So, to answer: the analyst recommendations have little correlation with what will happen to prices in the future. Therefor I just and completely ignore them.

2 Likes

And about a year ago there was a little story I got aware of because I hold Supermicro. An analyst of Susquehanna did publish a sell recommendation. Unfortunately just a few days after the position in Supermicro Susquehanna was acquiring after this recommendation reached the threshold to have to declare it to the SEC. Just a few days after their sell recommendation they made hundreds of millions buying the exact same stock.

A typical case of “do what i say, not what I do”.

![]()

3 Likes

I believe most of these ratings handed out by analysts are for price targets. IMO nobody can predict prices, analysts included.

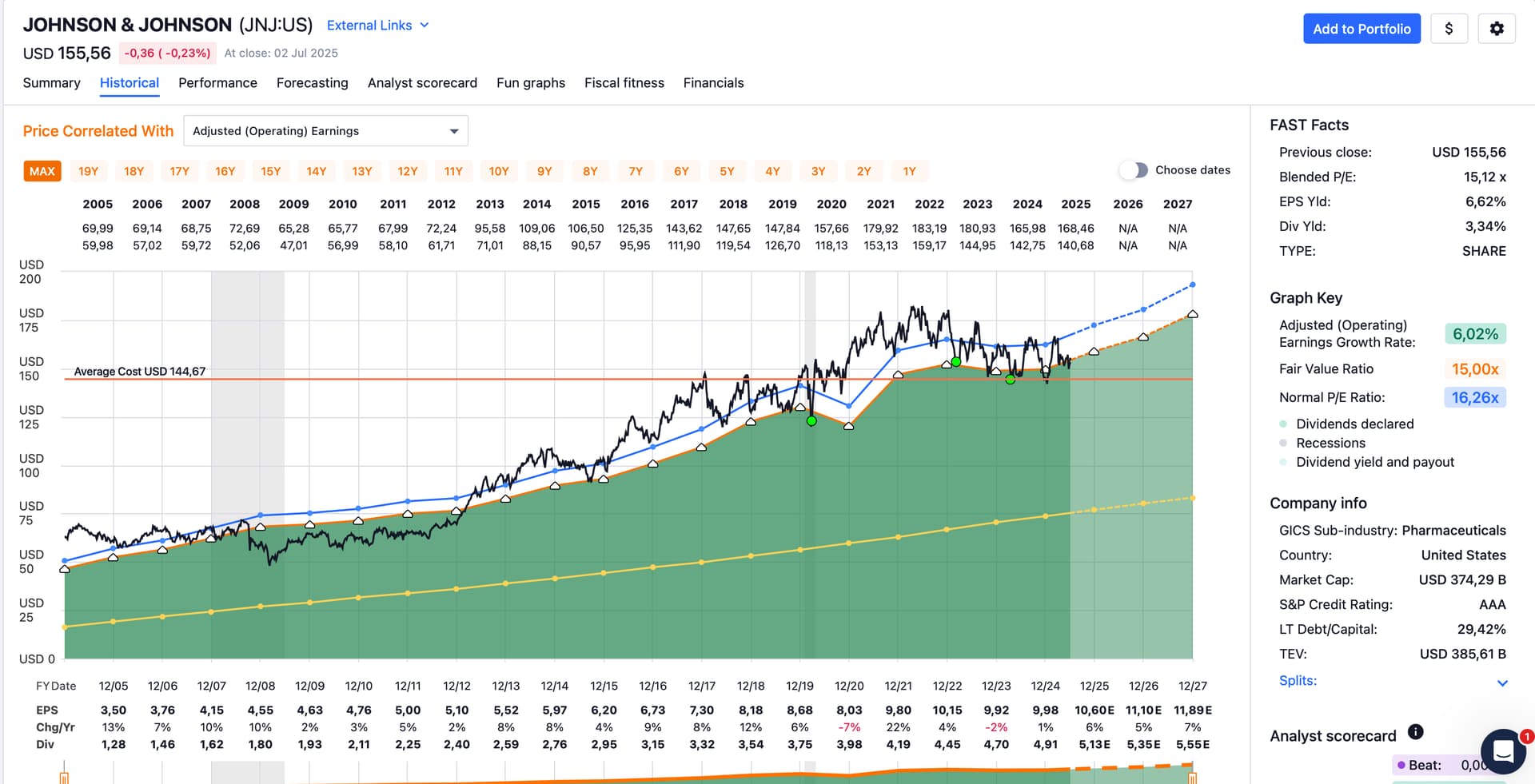

What analysts tend to be better at is predicting company earnings. Price tends to follow earnings (if you’re in the fundamentals camp like me) and thus earnings predictions can be useful (but mostly, as a long term holder, you often don’t need them predictions, just look at a steady trajectory of rising earnings.* Price usually follows some earnings per share (EPS) multiple, depending on how fast the company is growing their earnings.

* E.g. textbook example Johnson & Johnson:

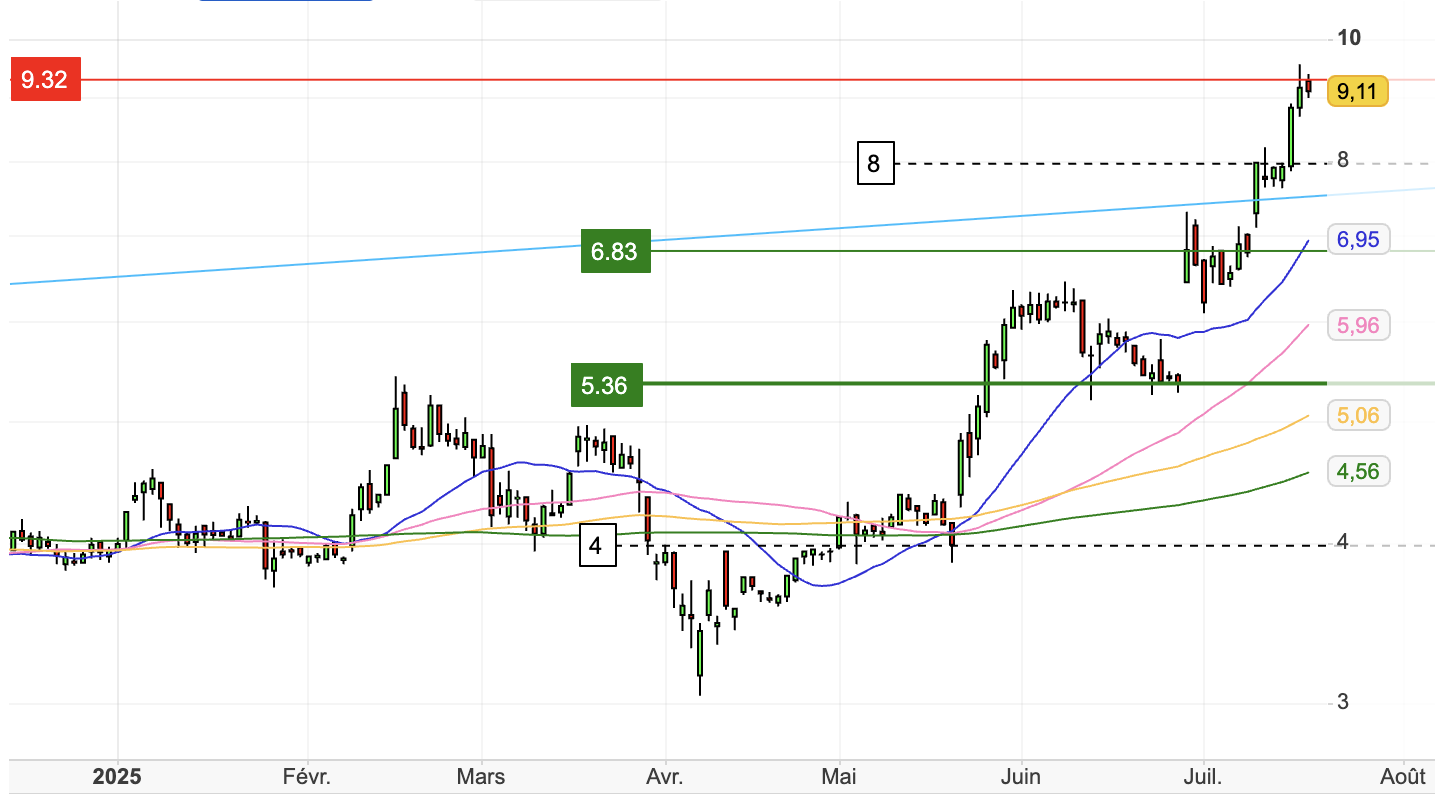

(There exist of course textbook counter-examples, e.g. Tesla:

Best to stay away of these, IMHO. YMMV, of course).

4 Likes

Does anyone understand what Circle actually does?

It seems to me that their model is following

- clients give them their cash (USD)

- clients get a token

- Circle buys US treasuries and collect interest

- I guess they need to maintain some reserve of highly liquid holdings to avoid bank run.

- I also think it’s kind of interest rate risk game. What happens if interest rates rise suddenly (unless they work with very short term bills), do they need to buy more treasuries to match liabilities?

So somewhat similar to savings account in bank?

Is this the business model? Or they do something else

According to their yahoo finance profile yes, they do: they provide a platform for anybody that wants to issue stablecoin. But yes, I suppose their main income comes from the issuance of their own stablecoins in EUR and USD.

The tokenized treasuries service is not allowed for US citizen due to regulation. The stablecoin may not be that stable after all, because there is no way of knowing what they exactly do with the cash.

Looking for a high-potential stock?

Consider the French server manufacturer 2CRSI. The company has recently signed contracts amounting to twice its current market capitalization, a strong signal of commercial traction. They supply high-performance, energy-efficient servers to international clients, including in the US and UK, leveraging cutting-edge NVIDIA chips.

The addressable market is vast, and the growth potential is significant; the stock has already tripled* since my initial investment. Looking ahead, I estimate an upside ranging from +100% over the next year to possibly +1000% in the longer term (personal view).

Valuation-wise, forward P/E ratios are extremely low, especially when compared to peers like Supermicro (SMCI). Importantly, 2CRSI has the ability to scale quickly without requiring a capital increase in the near term, an advantage in today’s market.

If this piques your interest, I encourage you to dig deeper. (ofc text generated by ChatGPT, that doesn’t call into question the relevance of this paragraph)

Nice LLM summary, now please tag it as such

3 Likes

I see Circle as a gigantic cash machine because of their USDC stablecoin. Roughly said with their current capitalization of 62 billion USD they earn approximately 4% (all stashed in US treasuries) meaning that company earns around 2.4 billion USD per year very likely without having much costs…

So I started DCAing into CRCL with 1-2 stocks per month as part of my fun portfolio. Let’s see where this one goes to… ![]() or

or ![]()

![]()

But isn’t this same thing as having a bank account ?

JPM also have a lot of cash where they pay low interest and they also can invest in ultra short term treasuries

I don’t understand how this thing is unique?

1 Like

Unique it is not (there is already Tether with it’s USDT stablecoin since 10+ years). Tether/USDT is roughly 3x the market cap size of Circle. But Tether is not on a public traded company on the stock market…

So for me Circle It is more “unique” in the sense that this is a crypto company offering the second most widely used stable coin and the company behind it is on the stock market publicly traded. Furthermore compared to a bank it is making money out of “thin air” (crypto) if I may say and has basically no operating costs if you compare it to a bank like JPM.

USDC has also become the standard stable coin used in Europe as probably all EU crypto exchanges where forced to remove USDT.

I guess this is also a reason why this year there has been a surge of new stable coins popping up from crypto exchangs, crypto currencies, and more. Everyone would like their share of the cake…

No expert here, it’s basically also as risky as crypto I would say and hence my minimal DCA into it and part of the fun portfolio.

I still think it is a nicely packaged Money market fund from Company perspective.

Imagine if this was launched in Switzerland, the interest rate is 0% and company will have zero revenue

Agree with that, it looks like a proxy for buying US treasuries but with volatility on steroids due to the crypto market behind defining how much USDC will be bought or sold.

Elliot builds stake in GPN.

I hadn’t noticed it had crashed to as low as $67. I really need to set up a notification system…

No need to. 95% of all stocks lose money over the long run. The market gains come from the rest. So you need a notification system for those, not for the losers… ![]()

Over 30 years the ratio goes even down half, only 2.4% of the companies are responsible for the complete stock market gains. Just make sure you hold some of them and you are OK…

https://www.marketsmedia.com/handful-of-stocks-responsible-for-long-term-global-returns/

1 Like

So maybe just buy and hold the index is the right strategy after all! ![]()

1 Like

Yes, if you are OK with holding a lot of trash.

The main reason I do not do index investing are those companies: zombies, cheaters, overvalued bullshit with CEOs that travel with two private jets in case of one breaks down and so on. I would not touch those companies with gloves. Index investing is probably the only reason they make it that long.

It is OK to pick up a lot of stones in search of a diamond… but why should I pick up feces?

But anyhow, this is the stockpickers thread. ![]()