I got no issue with Defense papers, I’m not the pacifist style and you can actually do some (greater) good with the defense sector’s output. Not true for that of the tobacco industry.

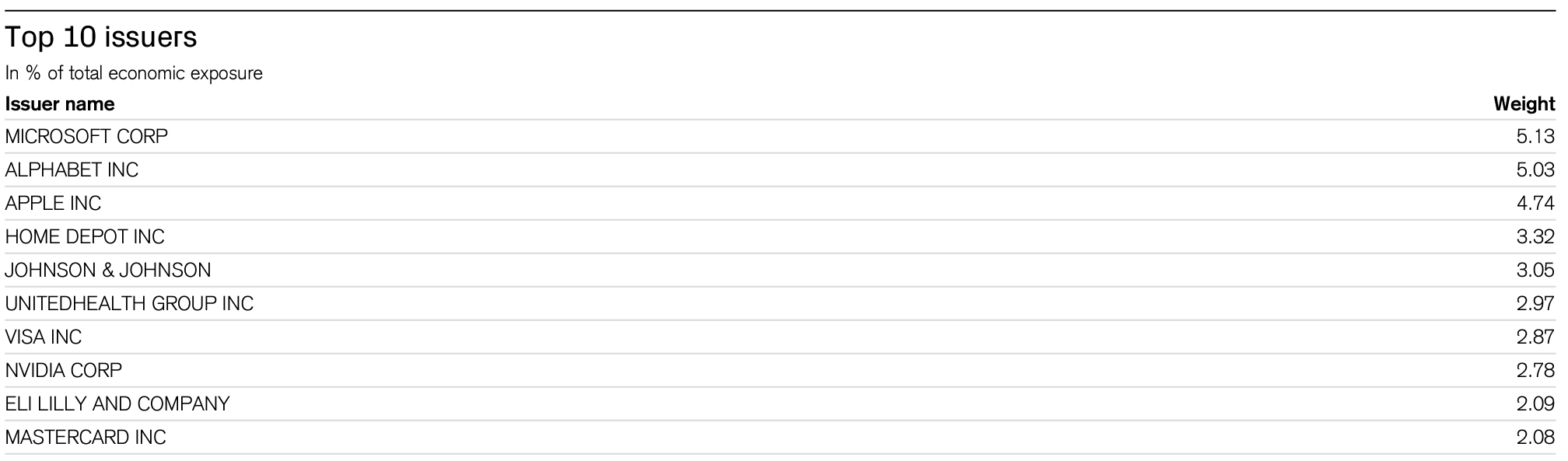

I’m not holding MSCI Quality directly, but the Finpension variant (CSIF Quality ex CH) with the following top10 holdings are “all clear”. Don’t know for the rest of the 290 companies.

Not even Meta is included in the heavyweight top10 bucket - strangely, I might add.

So, in conclusion, I still feel pretty OK with my choices. What my 2nd pillar pension scheme does in the background is not something I can directly or indirectly influence, so I’ll just leave at that - “ignorance is bliss”.

Having worked at Google (if I got that correctly from your posts?), that’s a somewhat weird statement. Sure enough, Facebook was much more reckless on occasions with personal data and data mining, but it’s the same sector, same goal (monetizing people’s data and lives for profit), with both of them shamelessly violating multiple privacy layers.

(I’m not talking about META, that metaverse thing is nonsense. Too bad it cost so much for the shareholders so far and Zuck is still not pivoting.)

I was naive and enthusiastic about the technology and the people when I started there.

I did not understand that all that money was made from ads off personal data mining. I mean, I understood it, but not its ramifications.

Probably drank too much Kool-Aid at the time. And Google was really a cool company when I started with them earlier in this century.

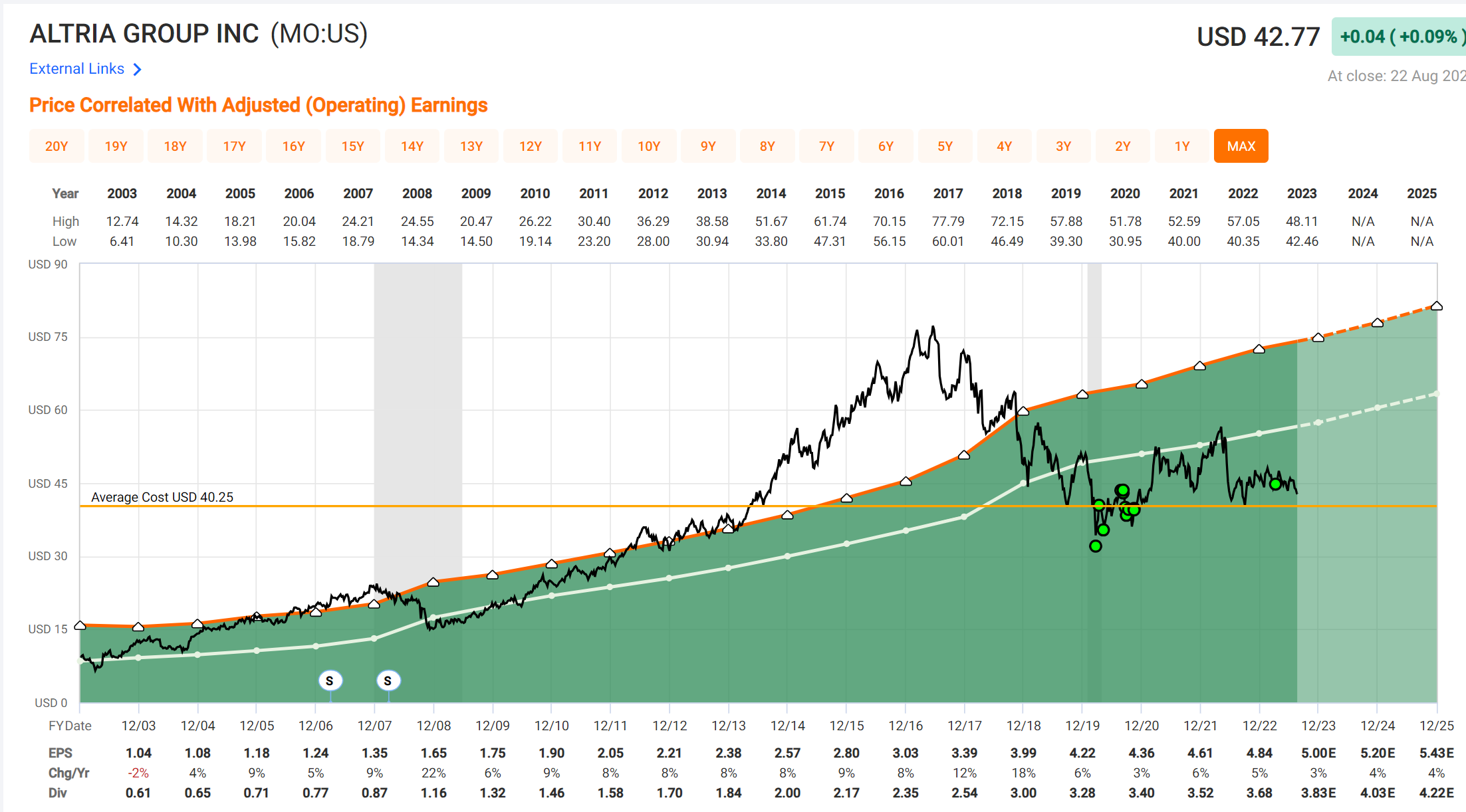

Indeed almost no tobacco (except for Imperial Brands).

Not even Lockheed Martin (however, Northrop Grumman).

I like this index. Lots of … ahem … quality, indeed.

Includes many companies which are on my watchlist but too pricey still (e.g. Home Depot, Tractor Supply, Costco, Diageo, Estee Lauder, Hershey, Kellogg, L’Oreal, Pepsico, Factset, Moody’s, United Health, Canadian National Railway, Cintas, Honeywell, Northrop Grumman, Accenture, Adobe, Apple, Mastercard, Microsoft, Oracle, Texas Instruments, Visa).

If anything, too much Tech (a third of all holdings) which explains why the fund performs mainly like the market.

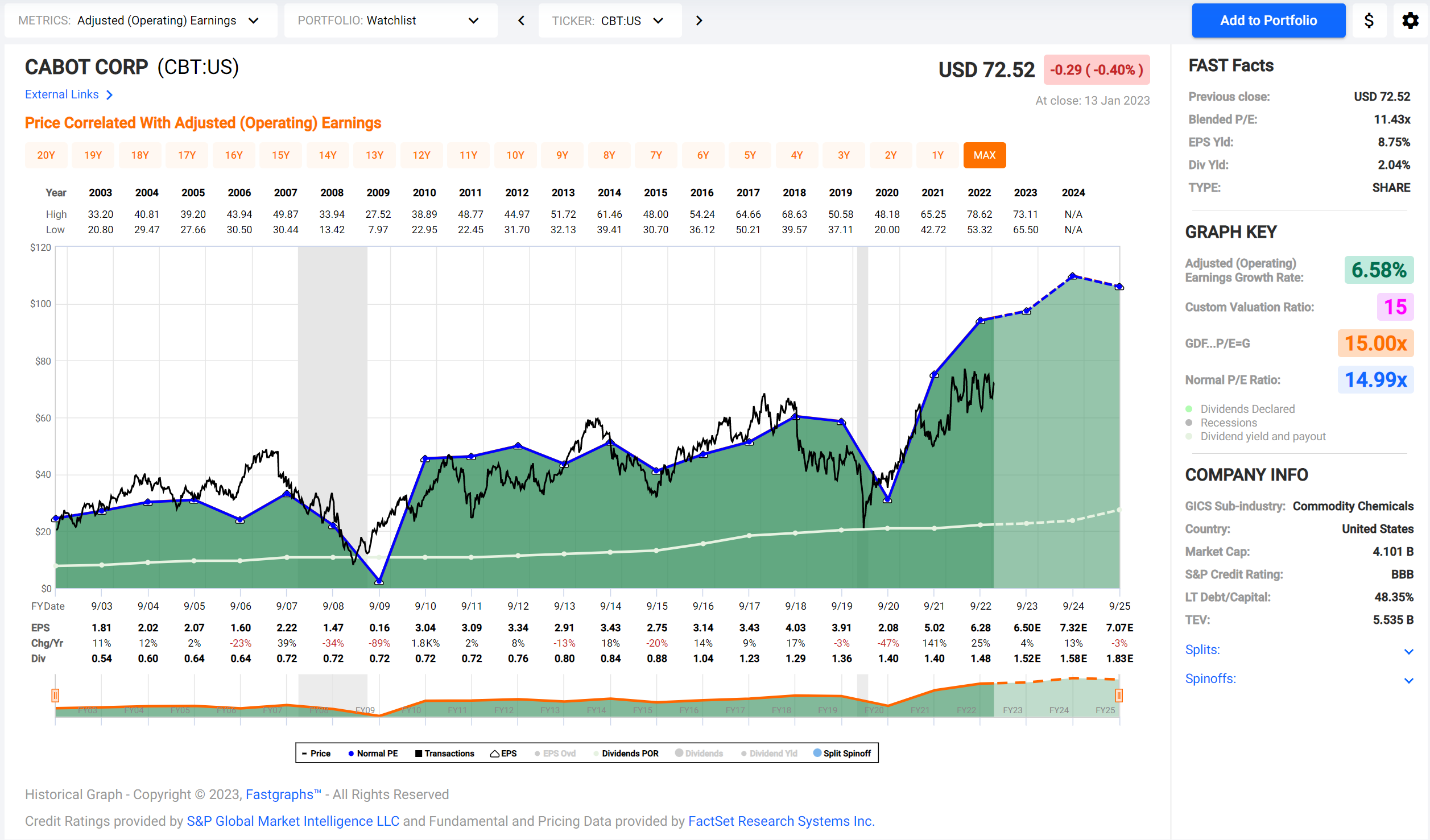

I was reminded of you, @conquestador, looking for Basic Materials companies as I went through my watchlist this afternoon and came across Commodity Chemicals company Cabot Corp (ticker CBT).

Cabot’s principal products are reinforcing and specialty carbons, compounds, conductive carbons, carbon nanotubes, fumed metal oxides, inkjet colorants, and aerogel.

Notably, the conductive carbons are used for batteries in case you like this narrative.

The company’s earning yield* is close to 9% which seems rather attractive.

The company appears undervalued and pays a 2% dividend that hasn’t been cut in more than 20 years (somewhat rare in the cyclical Basic Materials sector). It’s expected to grow earnings at 3.5% and 12+% over their 2023 and 2024 fiscal year, respectively.

Credit rating of BBB is pretty good and their Long Term Debt to Equity is about 50% which is ok given how it’s staggered out into the future:

It’s a small cap and isn’t in any major index (which I both like).

I also like that they’ve done a bunch of buybacks in their fiscal 2022 as their stock price remained attractive.

I would like it in my portfolio as I am underweight Basic Materials and the facts listed above speak in favor of the company.

What I don’t like, though:

Dividend Growth: They have a relatively low dividend yield of just about 2%. The low yield doesn’t automatically purge it from my buy list, but I would like to see the low yield compensated by a high growth rate of the dividend. Alas, the compound dividend growth rate over 20 years is just above 5%, and it’s not a steady growth: there’s years with 0% increase, years with 18% increase and everything in between.

Analysts struggle a bit with predicting the company’s earnings and the company misses analyst estimates about a third of the time. I guess this is due to the cyclical nature of Basic Materials companies.

(Possibly) Lack of Pricing Power: although they call themselves a specialty chemicals company, their industry classification is actually Commodity Chemicals. Not sure how much pricing power they really have, although they claim to be #1 or #2 in their business.

I’ll keep the company on my watch list, but it probably would have to drop a fair bit before I would buy - just to ensure a large enough margin of safety against further surprises to the downside.

If you’d like to dig deeper yourself, here’s their latest earnings presenation from September 2022 (which is also when their financial year ends) and their 10-K.

* Earnings Yield: Imagine you buy the entire company at their current price. The earnings yield is how much profit the company makes on the capital you allocated.

Thanks a lot @Your_Full_Name for the tip. I will add the title to the watchlist where I have also the tobacco stocks. Now my problem is more that I do not have the cash to buy them now I need to save for the new PV on the roof in February. Luckily in March it’s bonus time and I will most likely add some of the stocks from my watchlist.

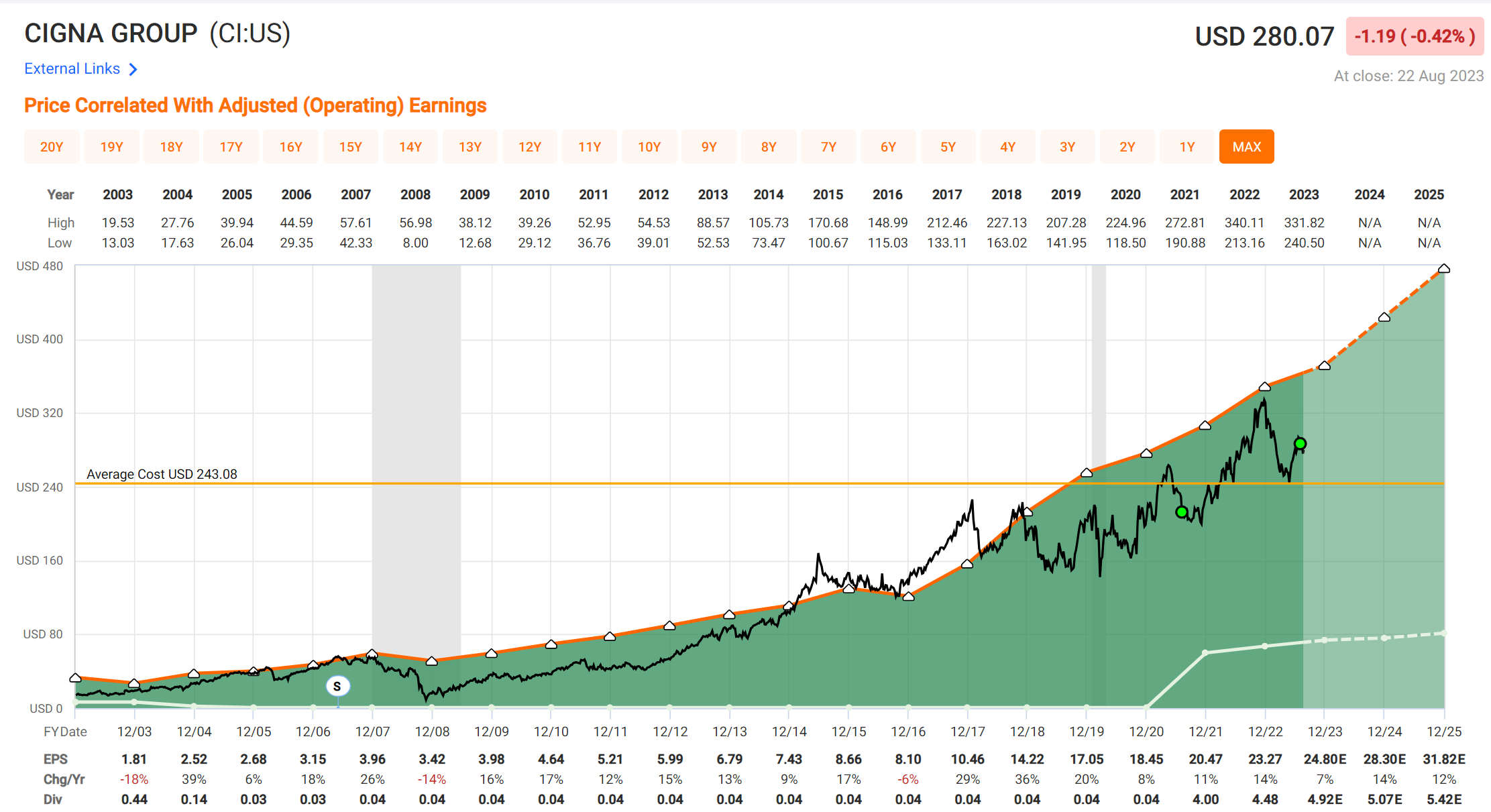

When I look at the list from your shares there are a lot of interesting options on. However, I can not add more healthcare stocks as I’m already overexposed to this section. I like basic goods, REIT‘s and Tobacco (I just like them now after your inputs and some research )

There are some industries which I would not touch with a stick (ok I told myself the same for Tobacco ). Why do you go for financials? They manage generally only money and no not create any additional value. Hence as soon as yields changes they are fully impacted. And I do not like them personally same applies for energy stocks they earn now good money for the next 2-3 years but in general I hope that we really change the way how we use and handle energy.

Well there is still some emotional factors on my site which I should remove from my investment decisions.

Again thanks a lot I‘m really glad to have such good tips from so experienced people .

Why spend billions on setting up an expensive factory to produce something “real”, when you can just manage billions of money on comission or something from a cozy office or (increasingly, these days) your own living room - and scale your business at the tip of your fingers?

True enough! This is why I have a (romantic) hope that blockchain could change things in finance. Right now I feel that all the players in the financial industry get rich with back room deals and unknown transactions. With a blockchain universe all these transactions would be open and transparent. Ok I know „dreaming off“

I know what you mean and I personally benefit from this economy (also not creating any physical value) but still I think it’s not right.

I remember that I saw once a study that sad, in the pharmaceutical/biotechnology sector the margins are really high but also the investment in R&D is huge. In finance though there is no (or almost no) R&D, heck not even improvement and still the margins are insane, hence I try to stay out when I can actively control this.

Working part time for exactly such a (boutique) company, I see first hand how lucrative it is to extract sub percentage management fees for managing billions by basically following the respective benchmark.

They, well, I guess I should be saying, we do some active management voodoo (factor investing) which I believe I could literally script to replace 80% of the portfolio managers’ day to day work (ok, ok, they script it, too, but they still show up full time for work).

To be fair, occasionally, we have alpha in some of our funds, which helps with our business model. Overall, though, our excess (or negative) return tracks the benchmark really really closely. Squint a bit, and the return curves are the same.

To be doubly fair (IMO), it’s hard to beat the benchmark in bull markets. I certainly can’t do it (see my performance in my Stock Picking Portfolio). However, given a sideways or bear market, if your performance just tracks the benchmark … great for the fees for the money manager, too bad for the returns for the investor. Probably what the majority of (index) investors already knew before touching this thread: just buy the index, it’s cheaper.

Reading your March bonus time comment I was wondering if there’s data analysis and charts correlating bonus payouts and stock price action, maybe even segment wise.

@San_Francisco already commented on why Financials maybe aren’t the worst choice, but generally speaking, I would say that business cycles allow you to time average accross all sectors if you are patient enough, and individual company valuations allow you to time average through companies within the respective sectors.

Financials still have the stigma from the Great Financial Crisis and are maybe generally still cautiously valued. In some cases that might me adequate, in many cases, that seems too cauious to me.

The ‘yield on cost’ … is from a purely technical angle probably not really that relevant? However, investing done by humans includes emotions, and I thus use it more as a psychological tool for myself.

I like it because it demonstrates (to me) easily that even for relatively low yield dividend payers that grow their dividend at a good pace, you’ll receive a nice dividend over time. In fact, those would probably be my favorite companies to buy, as they demonstrate they can grow their earnings even when handing out a portion of their earnings as distributions to the company owners.*

E.g. Comcast initiated paying a dividend in 2008 (in the middle of the recession, no less), then a meagre 1.12% dividend yield. Their compound dividend growth rate over the past 14 years has been close to 19% (even exceeding their earnings growth rate of about 15% over that period, but they managed to keep the payout ratio below 30% of earnings).

You would have reached 10% yield on cost after 10 years in 2018.

I just like that thought: I payed X for the company, and now every year the company pays me X/10. In less than 10 years (taking into account the years leading up to the 10% yield on cost), the company will have paid for itself (minus some opportunity costs maybe if I had been able to find a better investment).

It allows me personally more easily to not just chase high yield but also evaluate relatively low yielding companies if their prospect of growing the dividend looks like a possible and probable avenue.

Good luck with your stock picks and the transition to passive/active.

* Alas, I can’t afford to buy only low yielding fast dividend growing companies at my stage in life, but if I were a young person not having to rely on dividend income, that’s all I would do for my stock picking portfolio. In fact, this is what I do for my son’s portfolio.

I’ve started using FastGraphs more regularly now (second tool in my pocklet after SimplyWallSt), and I’d like to take the yearly subscription, but it’s quite a hefty sum.

Do they have Black Friday or back-to-school sales events?

I’m not aware of any. The did have a promo code a couple of months back when they introduced international companies as an additional feature and the promo code was featured in one or two videos on their YouTube channel, but I don’t remember the code or which videos exactly featured the code (and I don’t know whether that code still works).

Well, I just got an subscription update from Fastgraphs that includes a promo code (for the Premium subscription, at least):

“If you would like to upgrade and lock into our Premium Annual subscription, use code ACTNOW2023 at checkout for 25% off your first year on the Premium Annual.”

BTW, is the Premium Sub worth it? It’s quite some money with $500/yr.

I have the basic plan now, I’m following about 40 titles and I’m spending about 10 minutes per week in the tool - and I think I have all the info I need to base my decisions on data.

I’d be interested in your workflow and decision points, especially with FG.

I like the data in the premium subscription, but I don’t want to cough up the, ahem, premium for it (pun intended).

I like your routine: I also like to do basic FG check-in on a weekly basis, for a few more companies, albeit. I probably could reduce it to once a month (and sometimes I do) or even once a quarter, but I like reassuring myself more often.

Workflow, decision points … wow, simple question, complex answer. I’m afraid I don’t have a clear cut answer because …

For my own portfolio I have a mix of dividend and dividend growth stocks, and I am somewhere between still (re-) investing dividend income but also already starting to consume some of it. I am not sure I have one defined investing workflow for this yet.

I also manage the “starter”/junior portfolio (seeded with 10k in March 2020, no less!) for my son with an investment horizon of 40+ years, looking for undervalued growth, re-investing all dividends and expecting additional cash flow in from his future savings with the purpose of getting him rich slowly and for educating him that investing in companies really pays off!*

What I do use for both investing strategies is maintaining a Google Spreadsheet called ‘Candidates’ which is a watchlist for potential buys in the near term. When I have cash to deploy (in either portfolio) I update the spreadsheet weekly (usually Sundays). When I don’t have any cash, it mostly goes dormant, except for me adding tickers (but usually not yet decision data) when I come across interesting potential not-yet-researched candidates. The decision data gets added at the latest on the Sunday having before I want to invest in the upcoming weeks.

Decision data would be (extracted mostly from FG):

Earnings Yield - my soft minimum is 6.5%, but I do like it approaching or exceeding double digits

In simple terms, this is what earnings I would get from the company if I owned the entire company, before deciding what to re-invest, and (not deciding) what taxes and interest to pay on, etc.

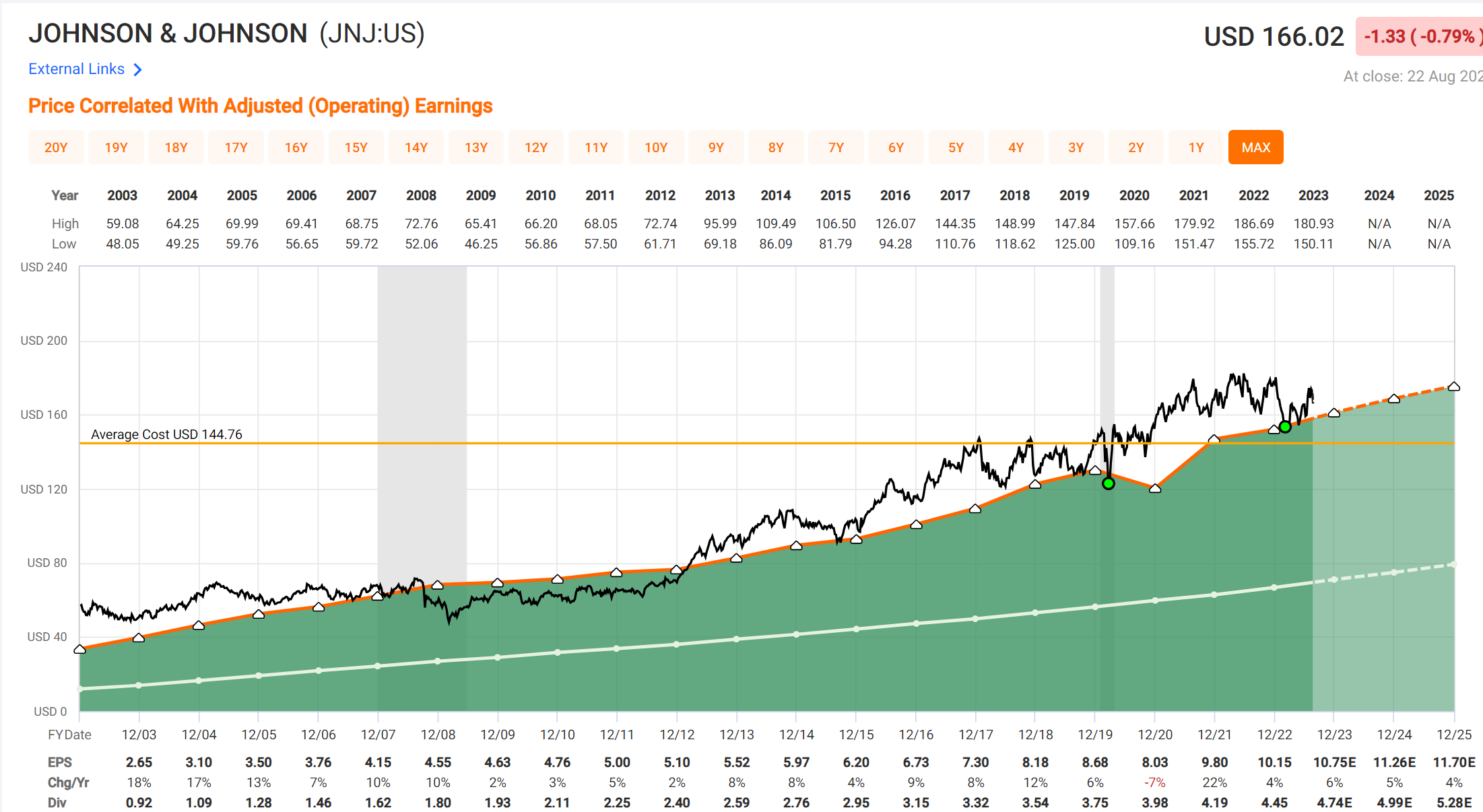

Earnings Growth - I look at Adjusted Operating Earnings growth as indicated by FG. No hard rule here, it depends on the current dividend yield, the company’s history of growing earnings,

dividend growth, dividend yield, whether the business seems cyclical, etc. Ideal companies display earnings growth like Johnson & Johnson:

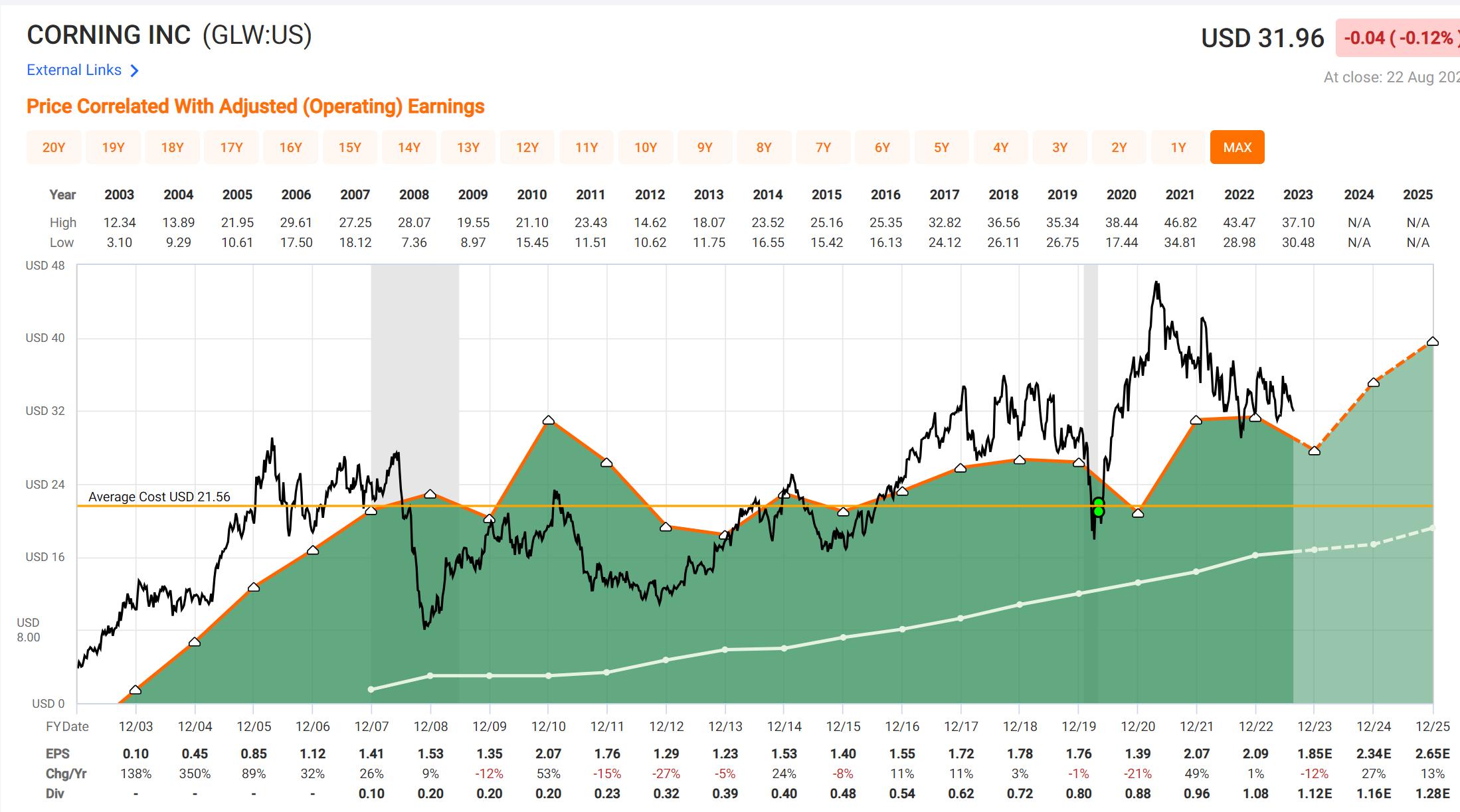

As a counter example of something that I like but that has cyclical but steadily growing earnings: Corning (they produce “high tech” glass, everything from the iPhone touch screen to your Pyrex oven form):

And, mayble lastly for earnings growth, when paid close to a 10% yield, I’ll buy into those even if their EPS history looks dismal as long as their prospects aren’t dismal. I’ll get my money invested back in 10 years, hopefully. E.g. Ship Finance Lease:

(pretty sure I’m jinxing it with this, sending SFL onto its terminal decline)

Dividend Growth: looking at the history of (ideally steady) divident growth over the past 10 or 20 years

Dividend Yield: well, speaks for itself. I am biased to ignoring companies that don’t pay a dividend, though I have made exceptions in the junior portfolio (and that was a mistake).*

Credit Rating: I like to do investment grade or above (S&P rating of BBB- and above).

Maybe easier to illustrate with some recent decisions on the portfolios:

T:

I added to AT&T about a month ago, mainly for dividend income and because they look undervalued. I don’t expect much growth as indicated by the FG forecasting calculators, but I’m happy with just collecting the dividend in the mean time.

GPN:

I added to Global Payments Inc. in December last year and again in June this year, mainly because they look severly undervalued and because their (albeit only with a very short history) dividend growth track record looks enticing.

UGI:

UGI Corp: Added to a position in July, because of their dividend yield, earnings yield, and expected Earnings Yield Growth.

GPK:

Graphic Packaging Holding: Initiated postion in March, added in July. Reasons: seeming undervaluation, nice (very recent) divident growth.

* BTW, a surprising lesson that I learned from investing in the two portfolios is that my watchlist (candidate buys for the near future) should be mostly the same for the two portfolios despite the hugely different investment horizon.

Nice Story, did pretty much the same thing. My initial Idea was that above 500k+ ETF Fee is quite alot in absolute terms. A SP500 would still have performed better

Glad to see there are stock pickers on here. My portfolio is also manual picked.

Even Buffett will tell you that you don’t need to be smart to succeed wtih stock investing. In fact, I think the individual investor has several advantages over a professional investor!

I share the Top 10 in my portfolio. It is rather boring now as I sold quite a lot of my holdings (particularly tech and energy) and moved the proceeds into bonds.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.