It is a nice concept “Burggraben” or margin of safety. But… everything changes over time. And the real advantage is time.

I don’t try to put a “fair price” on stocks but try to limit the risk of not being able to hold for a really long time. While there is cashflow the risk is limited, that is why I use mainly cashflow for that purpose. The really big winners are always surprises… nobody knows the future.

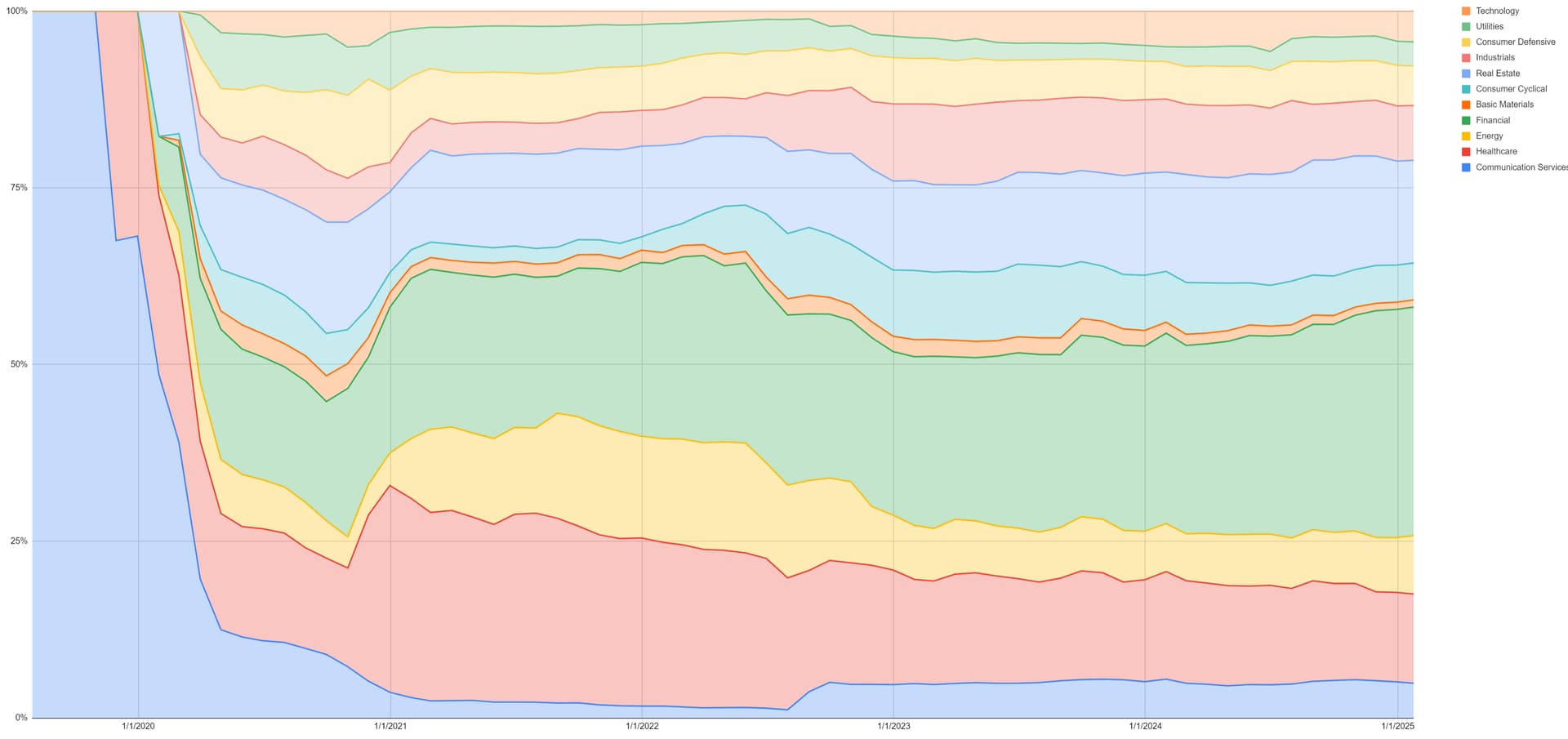

Sector diversification is an important risk-limit factor too.

Anyhow, my mechanics just keep out stocks that are too risky, do money management and tell me when to sell and where to reinvest dividends.

Stock picking is not part of my mechanics in the dividend strategy. Apart from that I am sure that your “quantum computer” is best to select what stocks to include, as was mine.

However, mechanical stock picking is part of my growth-momentum strategy. Yes, that took a lot to overcome my natural skepsis: when my model says that I should buy a certain stock I buy it, no questions asked. The questions to ask are already contained in the mechanics.

I find it interesting and refreshing to hear about your “mechanical” approach even if you seem to apply it mainly (only) to your growth-momentum strategy.

My stock picking portfolio overlaps about 90% with my income generating (aka dividend and dividend growth) approach. I am mainly looking at maintaining and increasing dividend income, capital gains on top of that are nice, but not my main goal.

I feel that your approach is more mechanical than mine (or to express it in terms more favorable to me: mine is more flexible), but we’re probably not that far apart in pursuing a somewhat rigorous framework. Yours is just different from mine.

I’ll explain my “quantum computer” ruleset along some of the axes you chose in the previous post:

I think these are actually two different things.

The “Burggraben” (moat) means that your business is fundamentally shielded from competitors (e.g. a railway company, as nobody can or will build a railway next to yours).

I don’t really have any moat companies in my stockpicking portfolio.

The one I came closest to buying so far is the Canadian National Railway Company (CNR), but it’s always been a little too pricey given my minimum cash flow restrictions.

The margin of safety means that I want to buy at a price that is below the historic* “fair”** value (P/E multiple) of the business or below the business’ “normal”*** multiple – I tend to pick the multiple of those two that is lower and want to buy below that price.

Amen.

That’s the definition of the future.

I used to think that, too.

I’ve meanwhile come to the conclusion that the market cycles through sectors and that these cycles surface buying opportunities when “recessions” in some sectors appear, but that over time, these sector weights will more or less balance out.

Perhaps some sectors will always be overweight given my preference for cash flows being paid out (at least to some extent), but I don’t limit myself to strictly no longer buying in sector X if sector X is already overweight in my portfolio. At best, if I have a somewhat equally attractive choice of two companies between already overweight sector X and underweight sector Y, I’ll pick the one in sector Y.

My sector allocation over time is still not fully balanced, but I feel comfortable with it.**** The only sector I really feel challenging to allocate to is Basic Materials.

* Choosing the time frame for determining the “fair” or “normal” P/E multiple is a little bit of an art in itself, where I feel my quantum computer might do better than an strict mechanical ruleset.

E.g. when evaluating a bank or an insurance company, it’s often best to ignore the years before the GFC.

** The fair value depends on how fast the company grows. For most companies it’s 15 (e.g. for most companies of the VTV’s top 10 holding) , for fast growing companies it’s P/E = G (short: PEG) meaning the “fair” P/E equals the earnings growth rate of said company (and I would expect the earnings growth rate to be sustainably about middle double digit %, e.g. for Broadcom in the above list).

*** The multiple the market has on average valued the company at over a chosen time frame. E.g. The Coca Cola company sports a normal multiple of about 18-19 x P/E even though – given its growth – the “fair” multiple is only 15 x P/E.

The normal multiple is the higher (or lower) price that the market thinks the company deserves.

Finance stocks tend to have a lower normal multiple than the calculated “fair” multiple.

Very interesting stuff, and thanks for the clarification of moat.

I neither use growth nor earnings. I would not call the strategy “not mechanic” but the stock picking cannot be automated because the universe is too big and I only want 25-30 stocks. I did use different methods to pick single stocks, had to pick 25 of them when I started. If I remember correctly I did select bigcaps with low price-to-sales ratio that were in my cashflow, enterprise value and debt parameters, then sorted them by dividend yield and just selected the first 5 per sector.

Interesting that I found over the years that stock picking is not that important for my goals in this strategy, which are low volatility and high cashflow. However, stock picking is very important for performance.

Sector diversification lowers the risk, but is also important for my “market dividend - invest dividend” concept. Market dividend: I use percentage of portfolio value, sell down to 5% whenever a position reaches 6% and invest the dividend and market dividend round robin in all stocks still on buy and that have a worth less than 4%. This makes some money on cycles, sector-specific or not.

Now in my growth-momentum mechanical stock picking I cannot find any stocks for months sometimes, especially after such a long bull run. But that is OK, it is like a scorpion that rarely eats but can survive a very long time without food…

I only hold MO in my dividend portfolio out of that list. Since a very long time and it is still on “buy” for me.

AMD looks nice, almost too good to be true. When checking the balance sheet however I find something a little disturbing: goodwill of 24 billions originating from 2022.

That may be a sign of bought growth. At least it means that future earnings will be lowered by that amount. What did they buy when, was it worth the effort?

Goodwill is still growing, meaning they buy more new companies than they write down the goodwill of past buys. Another sign of bought growth?

I like AMD for the CPU business, which I expect will displace a lot of Intel’s market share (I had long AMD, short Intel for a long time). However, AI has thrown a spanner in the works as it brought a lot of hype and sent AMD stock higher on the hopes of AI profits.

I would have rather invested in a less flashy, but more certain AMD without AI, which is why I sold all AMD once it hit $160.

I did not like to do that. Was with me for over a decade I think, many nice dividends. But the merger and split game with Dupont left them in a strange state and washed some Dupont shares into my portfolio.

My mechanical system says: they have negative free cashflow, but spend like crazy on dividends and stock buybacks. And they are in the worse half of momentum of my dividend portfolio. Adios.

I hope Dupont manages its cashflow in a better way.

It is not about guessing the future, it is just about risk. Burning cash and spend it on nonsense like dividends (of which I live…) raises the risk and therefore the stock has to go.

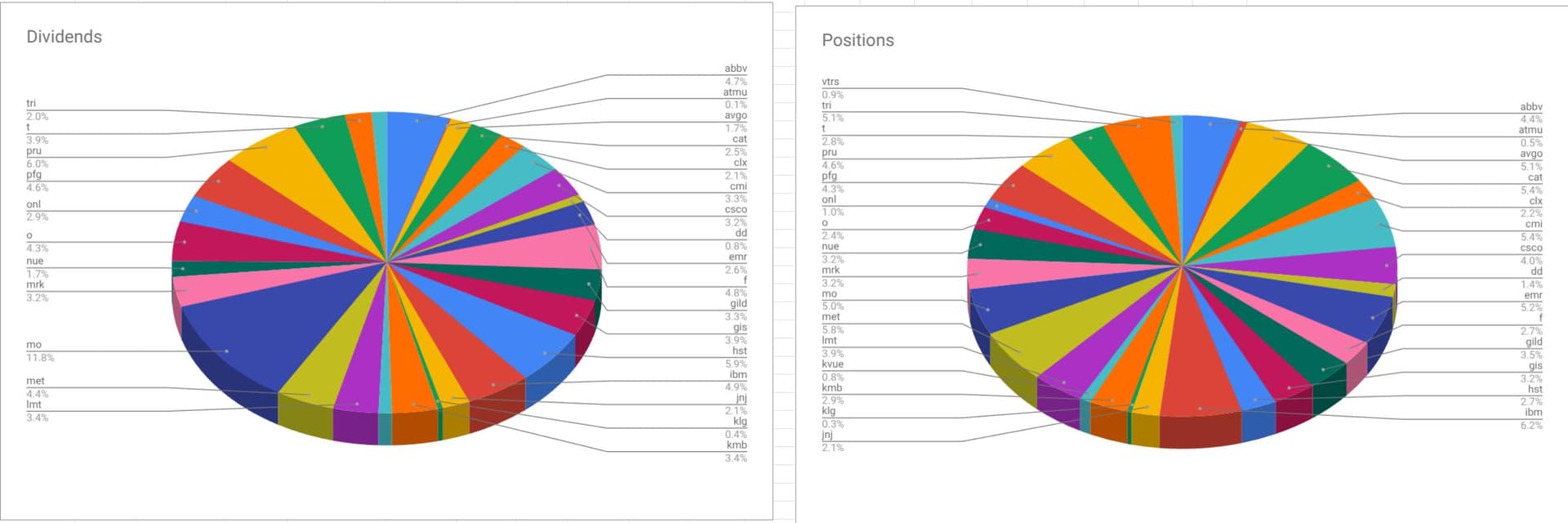

As I own already a bit too much positions I used the money to buy more of those stocks: ABBV,CSCO,F,GILD,GIS,JNJ,KLG,KMB,KVUE,LMT,O,ONL,T

There were some dividends left from January, which I invested in PFG and MRK.

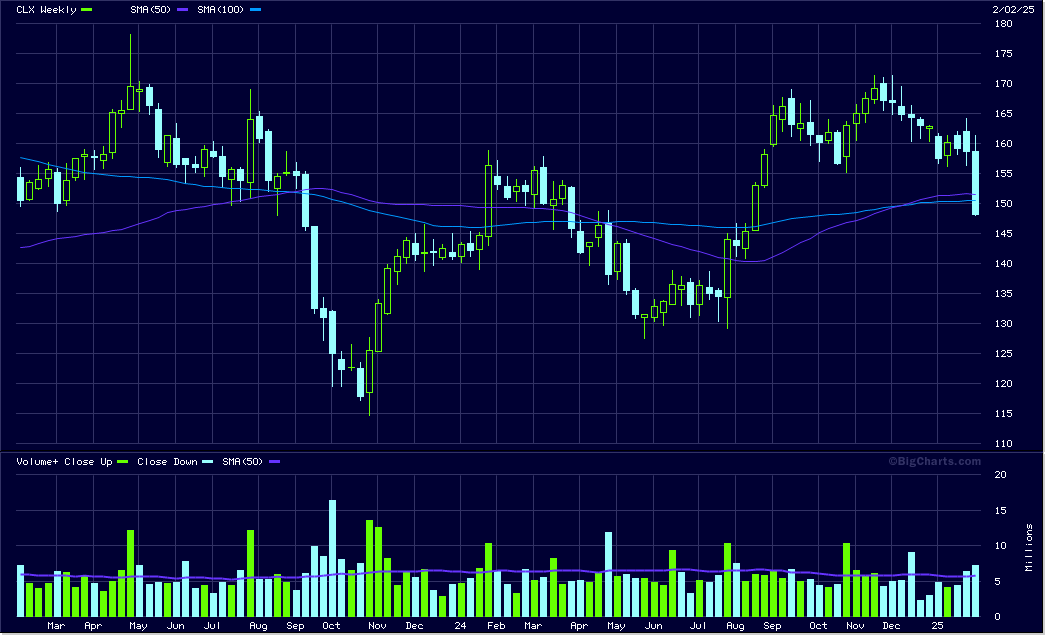

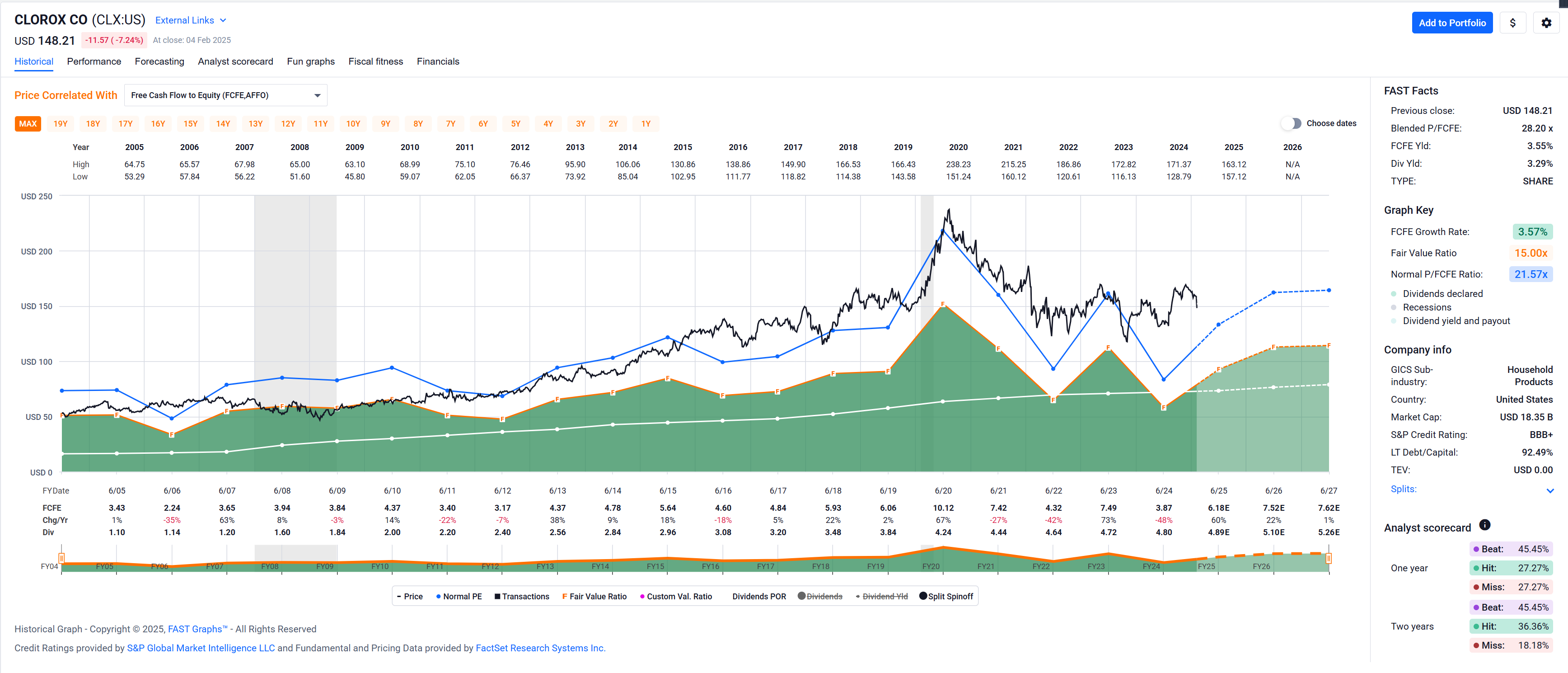

And again it happened: for felt two years there was no action in this portfolio and now already the second giant had to leave me, a stock that used to belong to each and every dividend portfolio and was with me for over a decade: Clorox.

The free cash flow in relation to the enterprise value was too low for at least two quarters. That alone would not be a problem as it could source from a market overpricing. But that was certainly not the case with Clorox: it did hardly move in two years.

My rules are mechanical and Clorox was not in the better half of momentum, so it had to go. Again I did spread the money to other stocks I did already own.

Sorry, I am travelling at the moment, nice weather in Spain. I hope at the end of the month I can go into more detail.

And the first market dividend of the year is here too: thank you IBM. I call “market dividend” when a stock rises to 6% of my portfolio value and then I sell down to 5%. Nice 16% extra dividend and tax free…

Clorox has been on my radar ever since Trump mused about the topic of injecting disinfectants* but I always found the company as (too) overvalued, not growing very fast, having a little too much debt, and clipping the growth of their dividend to minimal levels (probably mainly to stay in the list of dividend growth companies, but in the past two years only at anemic levels).

Cash flow coverage of the dividend seems a little spotty, but I personally wouldn’t panic yet as they – on average – still seem to be able to (slowly) keep growing their free cash flow and that in most years – and especially in the coming years – their free cash flow will cover the dividend (although admittedly the payout ratio seem on the higher end.

But then again, what are they going to do with free cash flow not paid out? Invest into inventing a super new form of disinfectant? I think not. So perhaps investor friendly to pay out a big portion of earnings/cash flow instead of buying, say, an overhyped AI company for the next generation of disinfectants.

Since your trading in this part of your portfolio is mechanical, it probably makes sense to sell.

If this company was in my dividend growth portfolio, I’d put it on my sell watch list, and depending on my entry price, they’d be at worst at the tip of the plank of being kicked into the ocean, or at best in the lounge area of plank jumping candidates where potential jump candidates mingle and discuss future cash flows over cocktails while watching the latest jumper in my portfolio: WBA.

* “And then I see the disinfectant, where it knocks it out in one minute. And is there a way we can do something like that, by injection inside or almost a cleaning, because you see it gets in the lungs and it does a tremendous number on the lungs, so it’d be interesting to check that, so that you’re going to have to use medical doctors with, but it sounds interesting to me. So, we’ll see, but the whole concept of the light, the way it kills it in one minute. That’s pretty powerful.”

Most numbers are OK, the relevant number is about efficiency, the FCF to EV ratio. I think too that Clorox will manage to get it right again, but because the risk is rising it had to leave.

My target in this portfolio is not dividend growth; it is high cash flow with low volatility. I want to hold as long as possible… but not longer.

Clorox was with me for over a decade, paid nice dividends and even some market dividends from time to time. It was a solid rock during Covid too.

As said, it is not about guessing the future but about avoiding certain risks.

I regularly browse my stock picking portfolio (which focuses on a subjective mix between steady dividend and dividend growth companies).

I tend to inspect positions that aren’t full* yet but in the course of browsing I come across a bunch of existing positions that I would label as conundrums.

They’re conundrums in the sense that earnings (or whatever suitable metric) keep growing, but price doesn’t follow, even for many years.

While price isn’t the focus of this portfolio – steady and growing dividends are – the price charts still puzzle me.

Some examples off the top of my head: Comcast, Global Payments, Imperial Brands, Altria, Verizon and probably a few others.

Today I’ll make the case for Comcast and you tell me why the market is actually right and I am wrong.**

According to ChatGPT “Comcast operates in telecom, business networking, entertainment, and international media” (international = non-US, i.e. Sky, hence UK?).

Plus points (looking at Comcast through my rose-colored glasses):

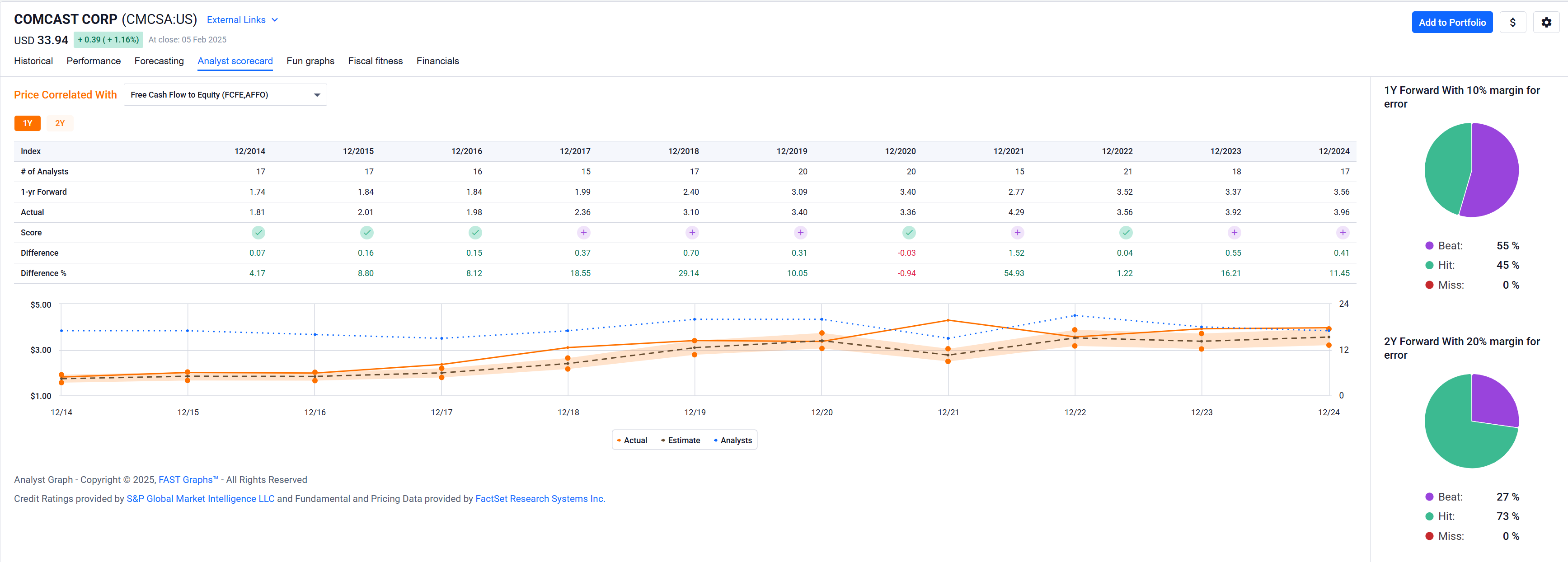

20 years of growing earnings at a nice cliff, over 20% annually.

Even if you cut off the spectacular earning growth years until, say, 2009, the company still grew nicely at double digits of over 10%.***

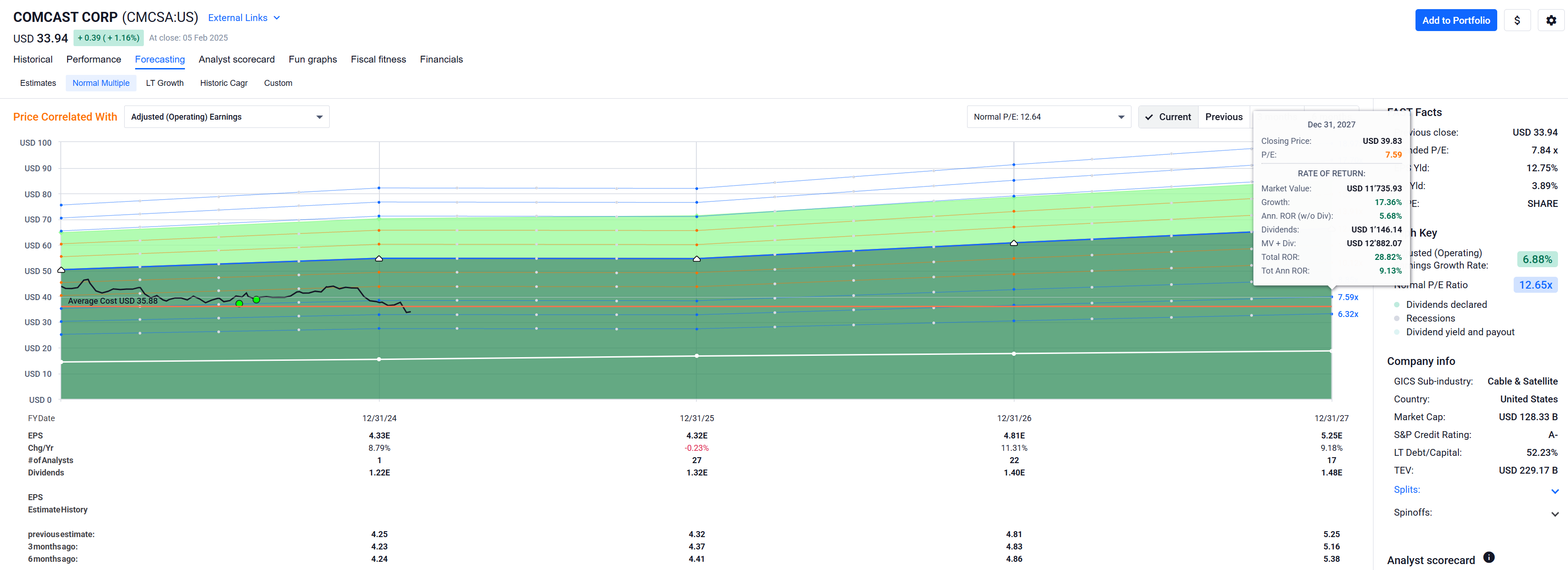

A- S&P credit rating,

about 50% long term debt to capital (yeah, could be better, but not bad either),

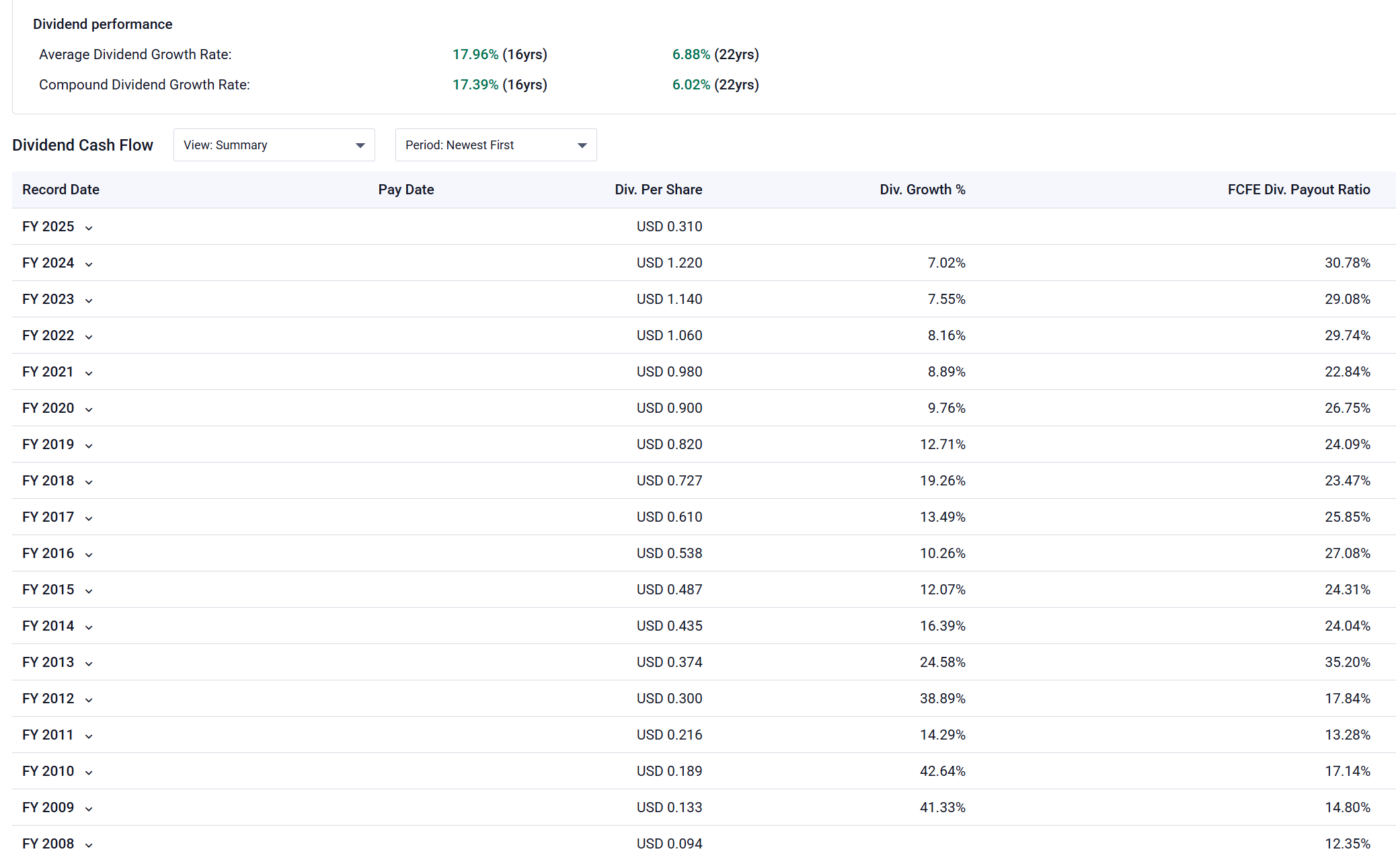

less than 30% payout ratio (if counted in Adjusted Operating Earnings) and about the same when looking at Free Cash Flow to Equity,****

they typically beat or hit their analysts’ earning forecasts (no misses for forecasts one or two years out when looking at Free Cash Flow to Equity,*****

16 years of dividend growth, averaging at 17.96% and compounding at 17.39%.******

even if the company stays at its current (P/E) multiple of about 7-8 until the end of 2027, the expected annual rate of return would still be about 9%.

Minus points (taking off my rose-colored glasses):

their businesses include legacy / old-school stuff like media and streaming services (NBC, Peacock, Universal Pictures). Not really sure what these are worth, if anything.

Cord cutting and declining cable TV business seems like a risk (but contained?).

it’s just a boring old company not at the forefront of technology, basically a consumer staple – for their businesses not questioned in the previous point – even if it’s in sector Communication Services.

I think the current multiple has room for even worse cons, but perhaps my stock picking colleagues see other issues that justiy the current price?

Shoot as you see fit!

(If people find this kind of discussion interesting, I’ll post a few more conundrums in my book.)

* In my book, below 2% of overall dividends generated, but it's only a soft limit.

** Of course, the market is always right, but I’d like to better understand why I am wrong (currently).

Your account will be suspended any minute now and the DICKS (Dividend Inquisition Conklave Katalyst Syndincate) will soon reach out to you regarding your punishment (probably death penalty).

Yes it DOES, accept it or the many people ready to hammer on keyboards in r/investing (and now r/dividends) will hold their breath until you accept your clear ignorance!

@anon17469660 who cares what the market thinks, the market thought Teslahahaha…can’t even finish the sentence, if your cost basis is good you’re getting raises for doing nothing.

Initially, your punishment was planned as a humane and (mostly) painless death by the guillotine. But now, with your recent taunting remarks, the market gods demand a – well deserved, if I may say – sacrifice.

In initial negotiations with QQQ and VOO we’re looking at additional … extraordinary and somewhat unique experiences for you.

OK. I will accept it if you show me a stock where the stock price fell by exactly the amount of dividend with a track record of at least 4 dividend payments.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.