I think it’s a mix of both effects (not buying as much and copying) but this type of sector is known to be cyclical so my gut feeling tells me buy on bad news:

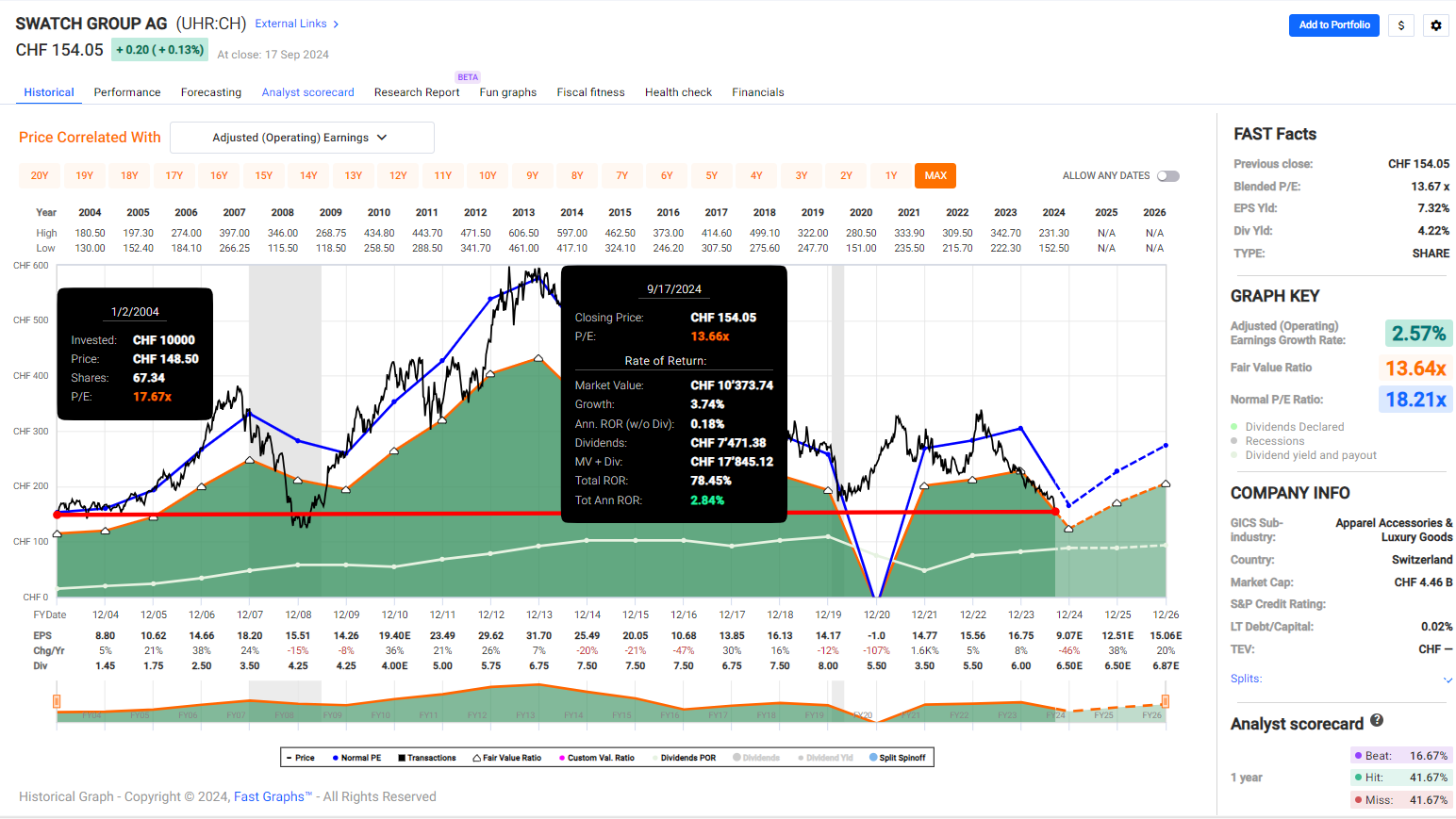

Didn’t do any research regarding the price of 30 but it feels good to buy at such a low price which has last been seen around 15 years ago. Last time I bought it was at 48 so I want to even it out a bit.

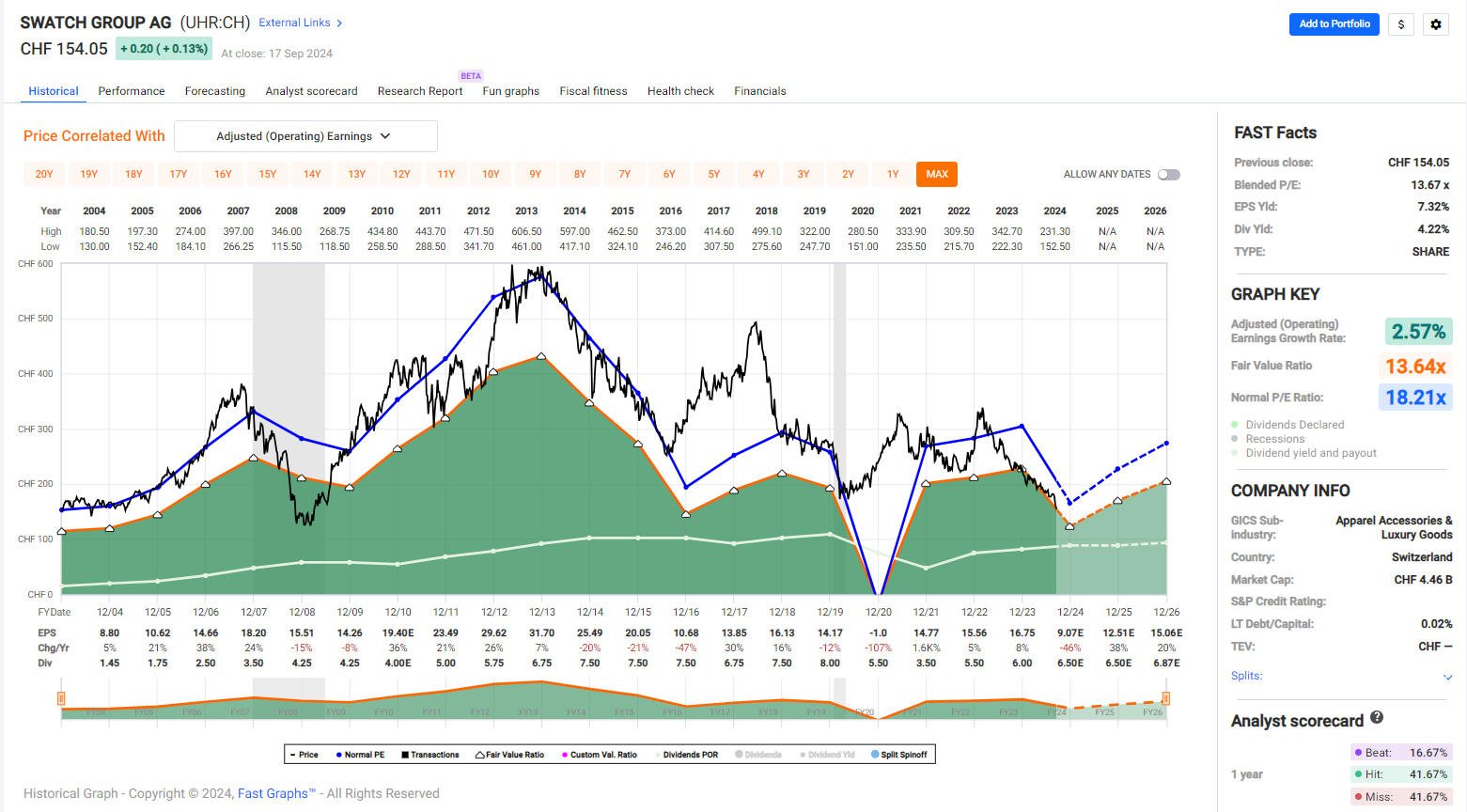

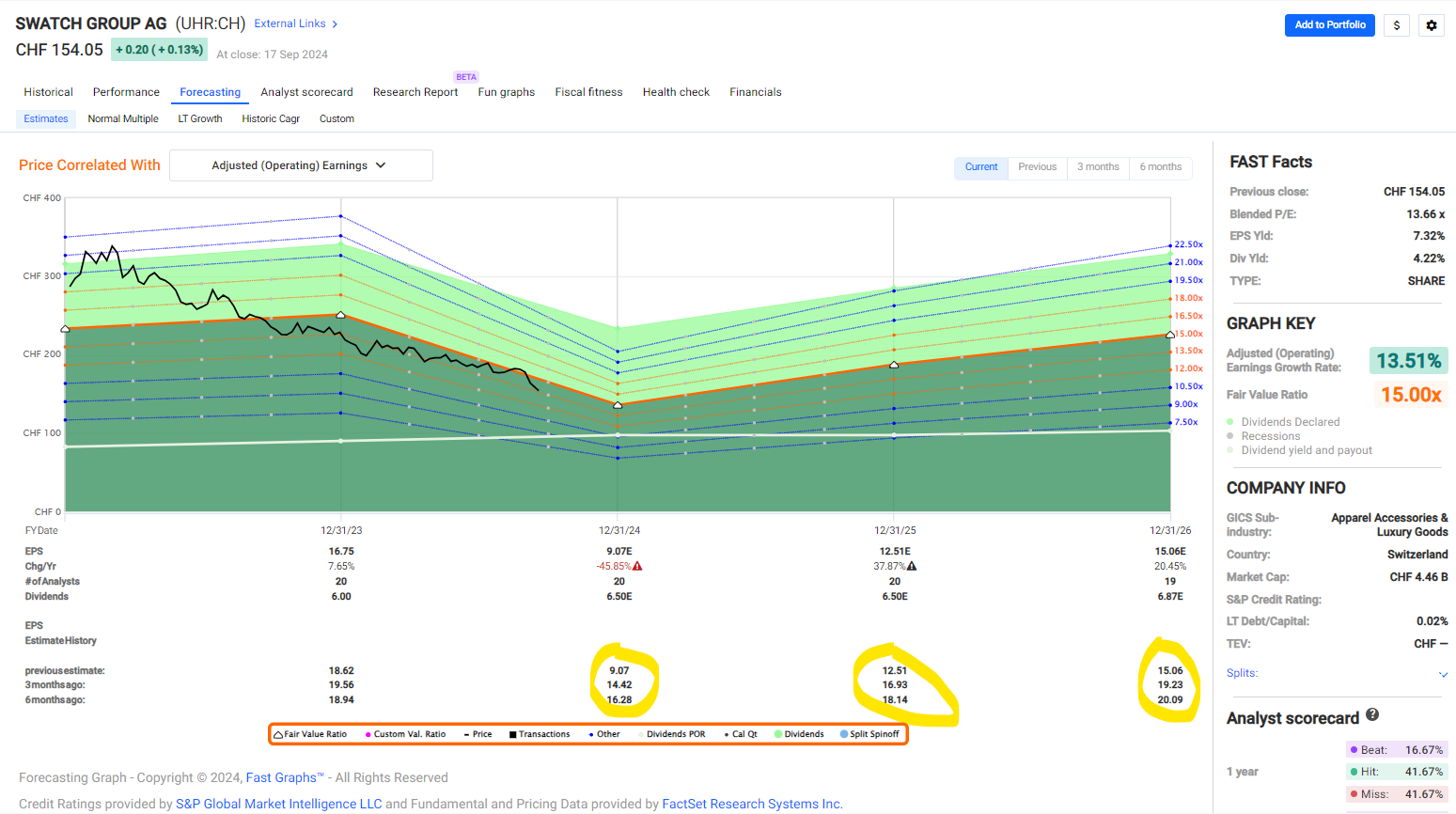

As already mentioned the company is cyclical but expected to grow earnings again in 2025 and 2026. The thing I like least about it is that analysts have revised down the expected earning from six months ago to three months ago and to their last / current estimate.

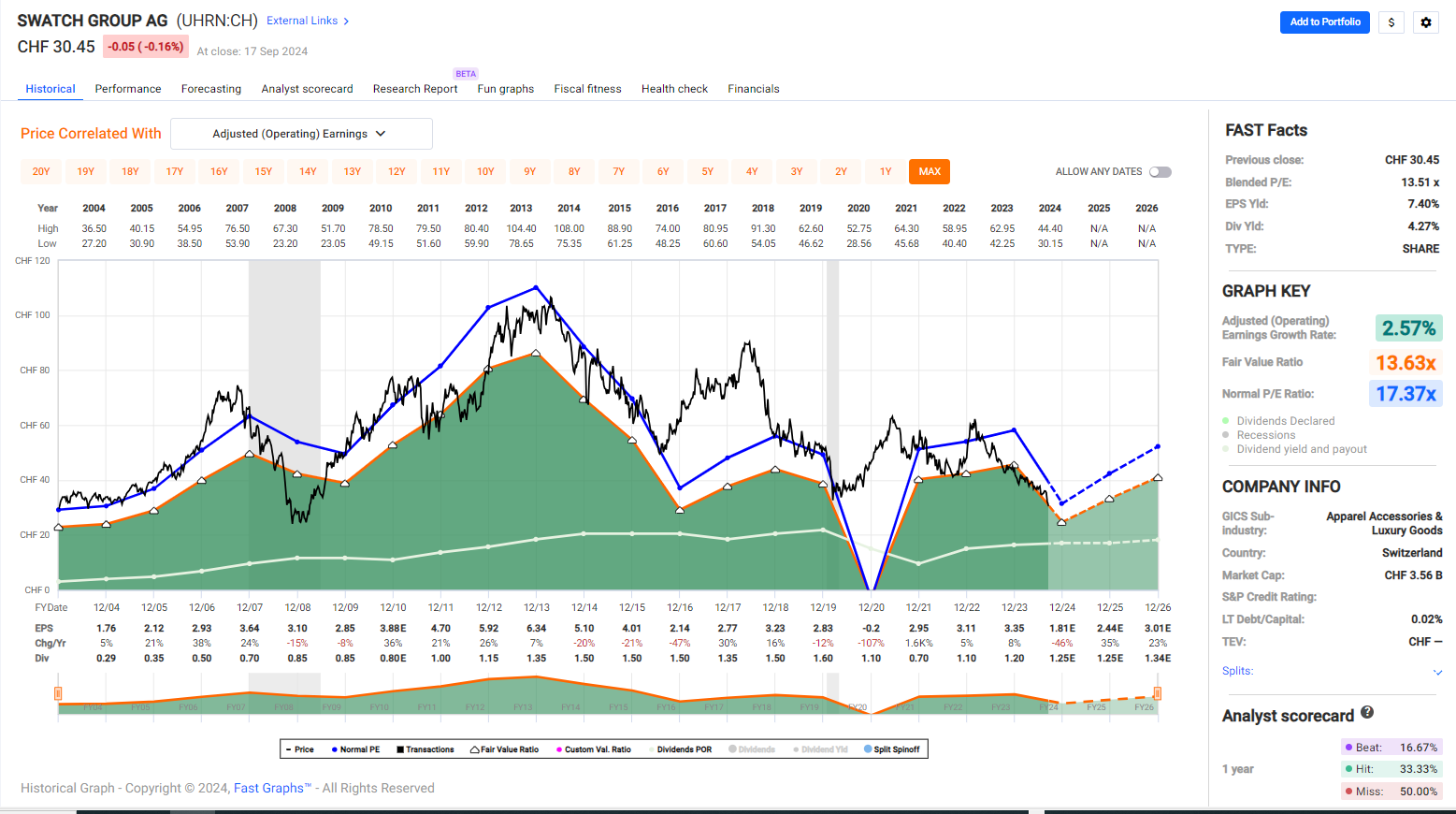

I suppose one has voting rights and the other does not.

Which is another thing I don’t like about the company: the Hayek family owns the one with voting rights and despite being an overall minority shareholder basically governs the company.

That exactly is a bright red flag. My gut feeling is that the Hayek family wants to see the shares tank, then will make a low-balled offer to buyout the company and take it private. They have a long history of despising the stock market and don’t even have an investor relations.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.