This is an interesting topic to read from the start.

First few answers already smelling the rot and warning about it. Some people still going in, and now we are here.

Guys, use common sense! If it promises significantly better returns/safer returns than publicly traded stocks/bonds/reits, then it’s very likely either extremely risky in disguise (with a high chance of default) or a scam!

Check the yields on stuff like CHCORP/ term notes, check yields on funds like DRPF and look for average returns on public stocks if it’s equity.

Does your investment you’re interested in promises you significantly more than that? → You probably should stay away.

Let me give you an exemple this year ANF grow 100%, VSCO too 100% these are publicly traded companies and it’s not a scam neither a bubble (they are not at their ATH) they are clothing brands who buy textiles and sell clothes.

Take my personal exemple I bought a second hand vintage Louis Vuitton bag in good condition but quite dirty in a flea market, cleaned it and sold it to a second hand luxury shop much below market price. Still made an instan 30% profit (working hours accounted) in 1 week.

Why do I use this example ? Because for small companies the standards of publicly traded companies do not apply because they have an huge growth potential. Higher risk to fail yes, but higher reward.

Moonshot with Lebijou did not provided unrealistic profits. High returns yes, but not unrealisticaly high returns like your crypto scammer. 7.125% return on loan is not this big.

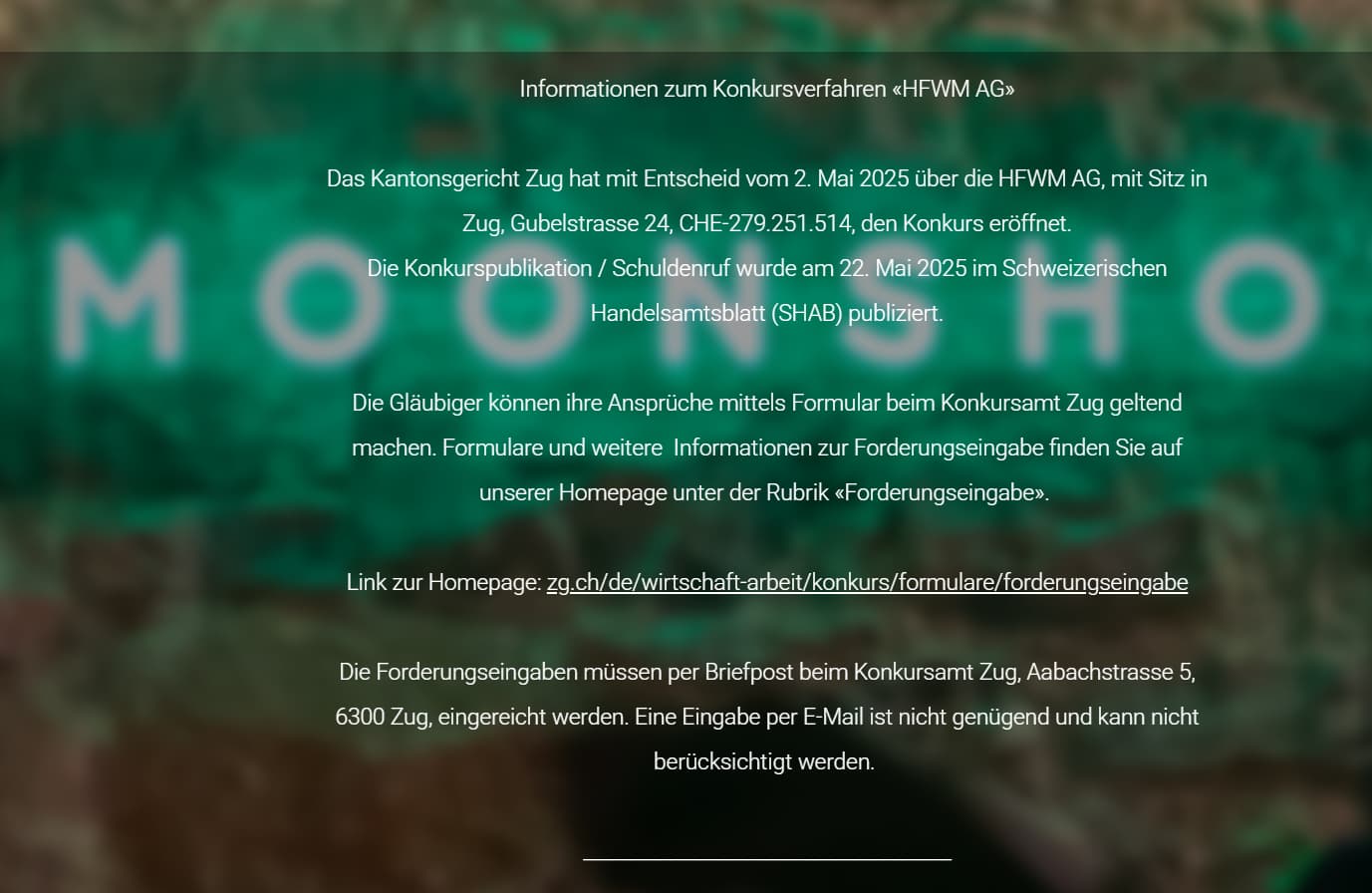

Common sense is important i give you that. But not everything that is good is too good to be true. Actually if I understand properly what was published by Finma it all had something to do with how they rented their place to the restaurant manager in Bern and since it was a sublease that was suspicious … the restaurant SUPERNOVA is now open so i’ll go have a drink over there and i’ll be back to you

The whole area of Bumpliz in Bern is built only on long term leases. Those huge buildings full with people paying their rent are leased until 2071 and people are still renting and buying them. The “landlord” just leased the land to canton Bern for a very long duration. The result is that the appartments are cheaper to “buy” but the rent isn’t. Of course a long term lease is much cheaper than owning the building but that may help to be profitable quicker.

That’s actually a green flag to me …

Well credit cards companies charge around 14% on their customers and credit firms (credit now, mutuo etc) are going up to 8.9% !

I personally lended my money to a swiss person at 8% through lendora.ch (i think it’s similar to lend.ch but for us aus welschland). And that 8% is witouth the margin generated by lendora and it’s credit partner.

That’s what some credit companies charge when banks are not interested, if they do I don’t see why Lebijou could not pay 7.125% it’s probably cheaper than other financing methods…

Also you are not buying senior corporate (priority) bonds which would be safer but you are buying unprioritized bond. It’s just a little bit safer than the stock …

Unfortunately I don’t have enough money to make a living out of 0.37% annual yield offered by 10 years - swiss governmental bonds

High rewards reflect high risks we have to be aware of that. It is not a safe investment. But yields alone do not mean this is a scam. I would say there is still hope.

and so in conclusion in an efficient market noone would buy anything else but government bonds. c’mon…

ofc there are risks, but these risks are either understandable and manageable (for the individual taking the risk) or you can walk away.

Construction financing is almost impossible these days under 6-8% and the 7.1% loan was exactly that - financing constructions that are risky, might not get a return in the end, and were to a large extent, unappropriatable (is that a word?) to a small-enough scope. Instead, you’ve put your money into a big heap and hoped for the best.

Could’ve been legit, could’ve been a ponzi scheme, you’ll never now until it comes back.

I’m with foxstone on multiple 6% loans where the secondary loan is collateral-guaranteed multiple times so I’d say getting back your money (and interest) has a very strong guarantee. 7-8% for a (good) bit of opaqueness on top is not really a giant leap.

You’ve already fallen for Lebijou’s scam. Shit happens, that’s just the way it is. Please make sure that you don’t fall for another scam! I say this because private WhatsApp groups sound alarming in this context and some scammed people are vulnerable to so-called recovery scams.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.