First, I am so glad to have found a FIRE community for Switzerland! (Is that an oxymoron? Just kidding…)

I would like to share my story and current financial status. The reason for my post is to receive any recommendations or advice on my path to FIRE, based on my financial situation below.

Background:

I recently accepted a job offer in the French-side of Switzerland. I am currently a 26 year-old engineer, with no significant other, and I am currently living in the United States in a relatively low COL area. I will be moving to Switzerland to start my job in January, 2019. The job is not with my current company, so I am going to be completely integrated into Switzerland on a B-permit.

Current situation:

Current Net Worth: ~$173k

USD Current Salary: ~$85k USD

Investment Accounts:

Roth IRA ($24k)

Company 401k ($73k)

Betterment Brokerage ($51k)

Savings:

Cash Account ($20k)

I know this is high for a savings account, but I will soon have some cash purchases to make with regards to my relocation.

Welcome and good luck in opening a Swiss bank account

Read all our posts about insurances first, since you might want to get one once you are here. “Third Pillar (a)” are the keywords for something similar to your 401k. You employer should have given you information about the second pillar as well. If you are confused read our posts about the third pillars.

uhm I think I missed another word together with 3rd pillar. Anyway what I wanted to say is to read the whole forum and once he get all the 3rd pillar posts, consider them as a swiss 401k.

Any recommendations on what I should do with my American 401k at my current company? Should I let it sit, or transition it into a Traditional IRA in order to continue contributing to it?

for this question, you will find better answers on the MMM investors forum as the swiss communicy lacks any knowledge on that system, or even post there. tons of threads on that topic.

from the big picture, if the contents of your 401k low cost index funds, then it’s already not too bad

Welcome! This is an amazing country to live in! (It’s also tiny compared to the US!)

So two pieces of completely unsolicited advice that I wish I had known when I first moved here:

First, as a fellow American, know now that a CPA who has experience with overseas Americans will be hugely helpful.

Because once you factor in income, rent, your employer’s contribution to your pension (which is considered as current earned income), you will be over the Foreign Earned Income Exclusion and you will owe taxes in the 32% tax bracket to the US Federal government.

A traditional IRA is helpful because it can offset to some degree your taxable income. A 3eme pilier (3a) is helpful offsetting your Swiss taxes, but that means you have fewer Swiss taxes to credit against your US taxes. My accountant declares my 3a as a savings account and puts the earnings on a Schedule A, rather than trying to figure out how to declare another pension account.

I hide nothing from the either the US or Swiss governments; the penalties are disproportionately high if you do and get caught.

The bonus is that all debt interest is deductible off your taxes here. So my US credit that I still carry a balance on? I deduct that interest off my Swiss taxes.

And the second piece of advice:

When you sign a lease on your apartment, double check the green sheet for the previous tenant’s rent. If the management company (regie) has raised the rent by more than 10% but not painted, renovated, redone the floors, you have 30 days to contest this and have the rent lowered. (Join ASLOCA the renters’ union, they will help.)

I thank you all so much for these helpful responses. This community is awesome!

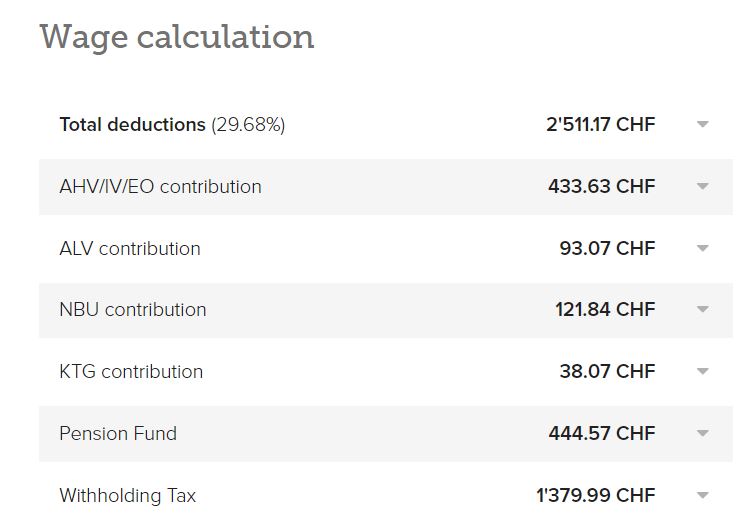

I do have one more question. I am having trouble reliably calculating my accurate take-home salary in the canton of Fribourg. I used the lohncomputer website based on my $8461 wage per month. I have a 13th month salary, so I just did 110,000CHF/13.

The estimate is ~5949 CHF, minus health insurance. Should I add 250 CHF back to that value, since my company will be providing me with 250 CHF monthly?

Do you believe that ~6200 CHF a good approximation for my take-home? My goal with trying to figure this out before moving is to support me with the creation of my monthly budget (i.e., percentage toward rent, groceries, ski passes, etc…)

Hi and Welcome! Another American in Suisse Romande here. Personally, I’d leave it in the 401k if you might transfer back to the US for the same company at some point, but move to an IRA if that’s not likely. Either way, you probably won’t be able to contribute to either. Between us, my wife and I have traditional and Roth IRAs at TIAA, Fidelity, and Vanguard, but as non-resident citizens, can’t contribute to any of them.

If you think you might buy here, then I do recommend the 3rd pillar contributions. My tax guy does include as a post-tax retirement account, but as other mentioned, the savings you get in CH are offset by the tax you still have to pay in the US. For all the talk of taxes, my numbers when we arrived are almost the same as yours, and most years we pay more to the accountant than to the IRS. (we did arrive with kids, so the child credit helps a lot there).

Hi! Yes, no doubt that would work. And it’s still earned income, so the IRS would be happy too. I’ve thought about doing the same, as it would also let us contribute to 529 accounts. My brother uses a UPS store mailbox to keep a US address, which might work too. I think it isn’t considered a PO box as it isn’t a USPS box.

Good luck setting everything up! On the Swiss side, we’ve had really limited options - only the cantonal bank will touch us. I’ll be trying out VIAC for 3rd pillar in January, as they seem to be the only option beyond 0.05% interest.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.