Thanks, I had the same impression.

Please check as well their investment opportunities/the products in the background.

Do you have another list than what I posted earliere here with a screenshot?

@oswand Swisscards recently also had the 75k promo, they regularly have it, but not ver often (ca. once, twice a year).

Moreover, I don‘t know what happens with the Amex Platinum if you are cancelling your Alpian account; can you switch the billing account, what does happen to the points?

This and probably no one in this forum. Nevertheless, I like being up to date regarding various banking institutions despite I will probably never use them.

For example, Revolut recently opened a (backoffice) branch at Paradeplatz; who know, this could be of use in future, if they intent to get the Swiss banking licence, for example.

You nailed it! The debit, labelled as “Droits d’inscription” and “Tax” matches the 35% witholding tax on interests so that was it. I’ve been confused by the label.

Then I don’t understand their promotion strategy: they promote their solution by offering banking perks (free account holding for 6/12 months, free cash bonus), emphasize their metal debit card and require the user to go through the physical card payment experience using the chip in order to get the sign in bonus.

My understanding is that many new clients get confronted to the banking part of the application first, then get eased into the investing part. I find the debit card experience to be really weird and not build confidence on the actual exclusivity of their investing solutions but, as you state, I’m not in their target audience so may not be assessing this properly.

Is there a way to access their investment vehicles list without signing their investing mandate? I don’t intend to open an investing relationship with them and would rather avoid the hassle of having to close it afterwards.

It should be freed 6 months after all conditions are met (wire 500.- on the account and do 2 payments using the card). They seem pretty reactive, I’ll keep you informed in January next year about how it went.

Hmm, I don’t think so. There was only a questionnaire to assess your risk appetite and then you have to accept it - as long as there is no cash, they will not charge you anything. So: keep the assets only on your Alpian bank account, without choosing an amount.

Did not have a hassle with closing the account couple of days later (I did not use any codes intentionally).

The selection of potential funds was that day very poor, I did not saw a benefit to have some cheap basic ETFs in one basket, which everybody can handle. And here we go again: we are not the target audience

It was the same for me. Once I fulfilled all requirements (use card, transfer money) I received the bonus within a few days if I remember correctly, so you likely won’t need to wait for 6 months. FYI, if you close your account within 6 months they do have the right to claim back that bonus [1]. But if your account has a balance of CHF 0 what are they going to do lol.

I guess they internally know what the conversation rate is. So you spend X amount of money (sign-up bonus) to get Y amount of customer assets. It must work, otherwise they wouldn’t do that.

No, but I’d guess they mainly invest in ETFs - they use IBKR in the background. To gain access to their offering, you’d have to give them at least 10k (Guided by Alpian) or 30k (Managed by Alpian) [2].

Because they are an Effektenhändler [1] [2] and are therefore required to pay the stamp duty, doesn’t really matter what broker they use.

Die Abgabepflicht obliegt dem inländischen Effektenhändler, der als Vermittler oder als Vertragspartei am steuerbaren Geschäft beteiligt ist.

Neben den dem Bankengesetz unterstellten Banken sind vor allem auch Anlageberater und Vermögensverwalter sowie Holdinggesellschaften als Effektenhändler zur Entrichtung der Umsatzabgabe verpflichtet.

Alpian is a bank licensed by Finma [3].

They pass on the costs to you so that it doesn’t eat into their margins. But I think that was not the actual question.

Alpian has also lowered their interest in line with the other neo-banks.

0-100‘000chf yields 0.75%

100k-1000k yields 1%

This is somehow a weird setting. I have decided to not realize one part of my project and hence need less cash, therefore I switched 50k to wiLLBe and the rest goes to IB and into VT.

Nevertheless,

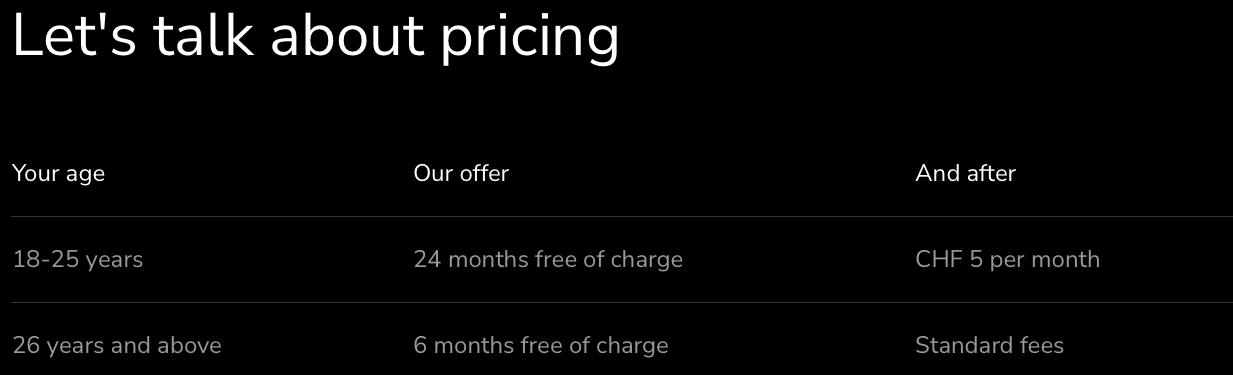

I liked the Alpian app (better than wiLLBe and I also like it more than Yuh) so far, as long as the account is free I will keep it but once they start charging I‘m gone.

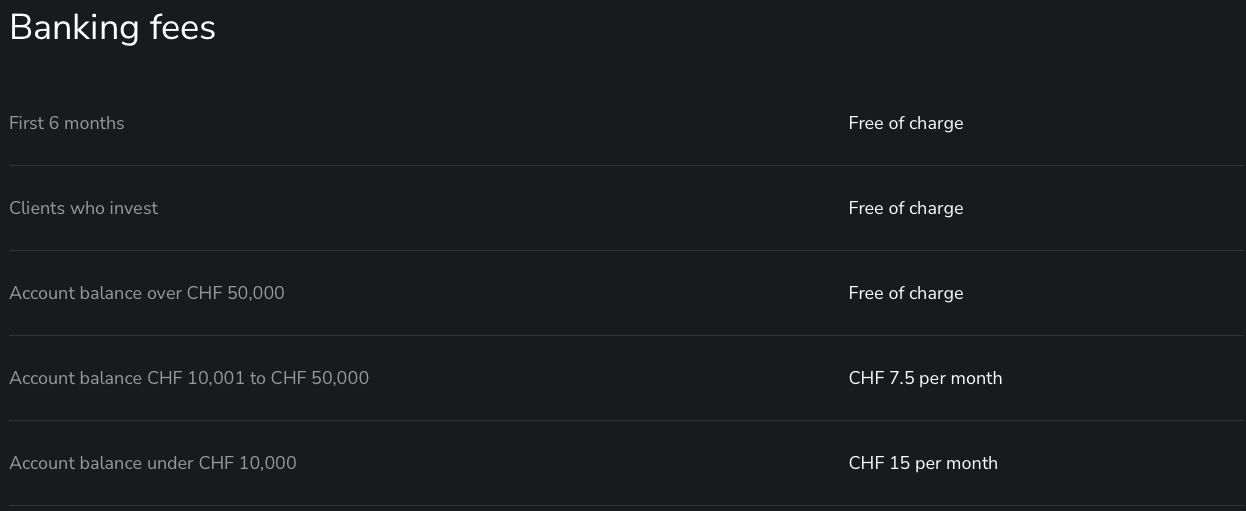

Moreover, they charge a hefty fee (CHF 7) if you are sending a currency to a country, which is not using this currency: e.g. sending EUR from Alpian to your EUR account at bank XY in Switzerland.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.