I can finally put money on the side for my 3a pillar at ~30yo, the goal is “simple”: I would like to own a house in order to be live decently when I’m getting old. I’m currently earning money only through salary with a good job where salary increase is expected.

I found Finpension thanks to all the community of Mustachian Post and other websites. However because I want a home in less than 10 years (best case scenario), I believe that investing in high risk equities is a bad idea, at least that’s what I’ve read. And because the market is so unstable with everything that is going on in the world (wars or also insider trading of Trump in the US with the taxes for example), I feel like it’s kind of a madness to do 100% equities now with my goals. But I’m also kinda uncertain if I will be able to afford a home if the home prices will continue to go up.

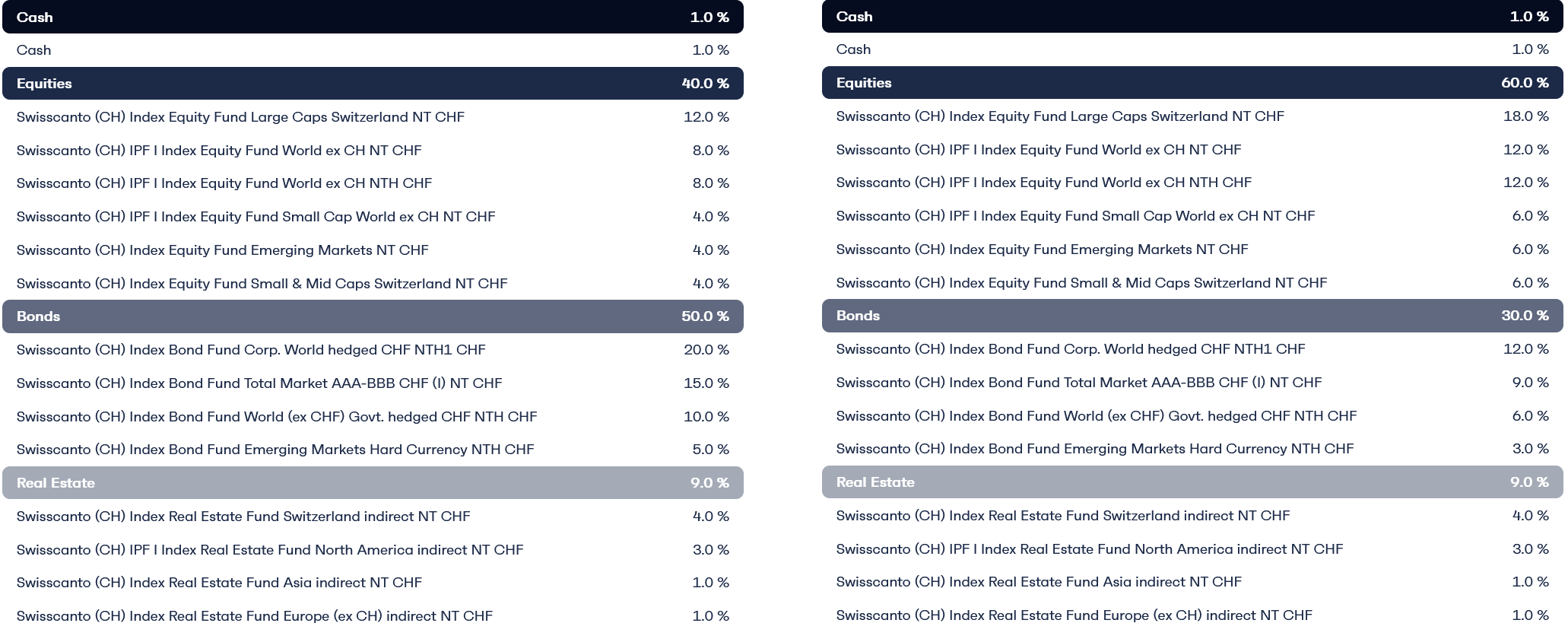

So my question is this, is it advisable to go with the default medium risk finpension Global 40 (Pension), or perhaps the 60%? I was thinking that maybe I could go in a 100% first year and following years I go with a 40%/60%?

And last question, in case I see or understand that a crash is gonna happen or is starting to happen, is it possible to move the money from equities to gold for example (if gold is not possible for 3a, transfer to cash/bond) for a a few month or is it not possible? I believe it’s possible but it can take a long time? So if something like this happen, we can’t really do anything right? I’m thinking a scenario where such as the 2022 war or something.

In case you have also good resources or tips about very important stuff I’m all ears, I did read a lot, but I’m still feeling kinda lost as I never invested before. I still need to put the money in something before the end of the year in order to reduce my tax rate for this year.

TL;DR: I’m thinking to go with Finpension Global 40 (Pension) (or 60%) with the plan of owning a house in around 10 years.

I must damit that I don’t really understand the bonds part of ETF. Hence I have stayed away for the last 20 years.

Given your expectation of a bleak economic future, it might make more sense to have 3 or 4 different ETFs: Stocks, Gold, Cash, maybe BTC. Maybe you can contribute 60%, 25%, 10% and 5% to 4 different pillar 3 accounts, each with a specialized ETF?

you are talking about 3rd pillar and 10 years, if you are going to contribute maximum amount it is 7000*10 = 70000CHF which will be around 4-8% of house price in 10 years (this is very rough estimation but I hope you see the point), what I am trying to say here is that even if your 3rd pillar value will drop in half it will not be significant factor for you dream to buy the house. This is why 3rd pillar is a good way to start investing, learn about it and understand your risk tolerance. The amount which can be lost is limited there (especially in first couple of years when you are learning about it) and you get tax deductions as a bonus anyways

At 30 years old I think you have a long time to go to recover from any market crash and I’d think you’d be best off to invest in equity heavy, well diversified, growth stock ETF(s)… even if you intend to buy a house in that time period.

Harvest the tax benefit of the 3a and continue with non-3a saving to get your funds for a downpayment together.

Thank you all for the feedback, very helpful. It’s true that I will need to also invest in other stuff anyway in the future and the 3a won’t be enough.

Also I’m reconsidering my goals, in case investment doesn’t go as fast as expected, I’ll just wait longer, this means I can maximize in equities at first and later I’ll be more prudent.

In the end for this first payment I went with VIAC Global 100. I will read more in the near future and open other 3a probably at finpension secondly. I found this new article from a couple of weeks ago that is very interesting in which 3a pillar to choose: https://www.mustachianpost.com/best-3rd-pillar-in-switzerland/

PS: I’ve also seen that the law in the OPP 2 article 55 limits the percentage per category in investment, however there are exceptions, am I required to invest only half of what I have in equities? Here is the law: Fedlex (link in german), Fedlex (link in french).

Well done. Whether VIAC or finpension (or neon 3a or frankly) doesn’t really matter, it matters that you started saving (good habit) and reaping the tax benefits. At 30yo, the best time to start your 3a journey was 10 years ago.

Whatever happens next year, don’t touch your strategy with VIAC. If a huge drop (20%+) happens (that everyone is waiting for since ~2018), like in this April , add your next year’s 7k (buy the dip). If you change your mind about the strategy, open another VIAC/fp product with a different strategy and start building that one. Better not to sell and flip-flop your strategy on the way.

If you want to hedge for real estate, make sure to add some real-estate exposure as well - as housing prices go up, your RE part of the 3a will also go up (and vice versa).

Stay the course for 10 years, you might be around 80-100k by the end of it. Good luck!

I will also open my first 3a investment account with finpension and I am in a similar situation.

With Interactive Brokers I already have a growth portfolio (VOO 49%, AVUV 4%, VXUS 24.5%, GOOG 6%, NVDA 3%, PYPL 4%, IBIT 2%, ZGLD.SW 5%) with a strong focus on US.

I was thinking to open a Equity 100 with focus on Switzerland account to add some home bias to my portfolio as with the Global strategy I have the impression to replicate most of my growth portfolio with just some extra Swiss positions.

Considering I have a 2a account and a couple of 3a accounts, does it makes sense to add home bias this way or would the Global strategy be perfectly fine?

Eventually a custom/hybrid strategy be better balanced introducing Swiss and Quality/Value position?

Asset Class

Fund Name

ISIN

Weight

Swiss Large Caps

UBS (CH) Inst. Fund – Equities Switzerland Passive Large II I-X-acc

CH0046164148

40%

Swiss Mid/Small

UBS (CH) Index Fund – Equities Switzerland Small & Mid I-X-acc

CH0110869143

10%

Asset Class

Fund Name

ISIN

Weight

Global Quality

UBS (CH) Index Fund 3 – Equities World ex CH Quality I-B-acc

CH0253609066

30%

Asset Class

Fund Name

ISIN

Weight

Emerging Markets

UBS (CH) Index Fund – Equities Emerging Markets NSL I-B-acc

CH0017844686

10%

World Small Cap

UBS (CH) Index Fund 3 – Equities World ex CH Small NSL Multi Investor I-B-acc

CH0214967314

9%

I am not so sure about the emergin markets and Small caps (total 19%) as they are already included in my VXUS etf. Therefore I would split this between the other position above.

That’s on the level of the foundation, individuals can invest 100% in equities as long as the foundation as a whole adheres to the limits. You don’t need to care about these limits.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.