Hi all, been reading and searching through the forum for a while but this is my first post!

I have a few questions regarding my first attempt at building a portfolio (100% equities as 30 yo with very long time horizon, located at IB).

The idea is to hold the total world market with a small cap & value bias in the US market (as suggested by Ben Felix (YT link and his PDF about it link). The reason why to keep the bias only in the US market is because of lack of good small cap & value ETFs for the rest of the world.

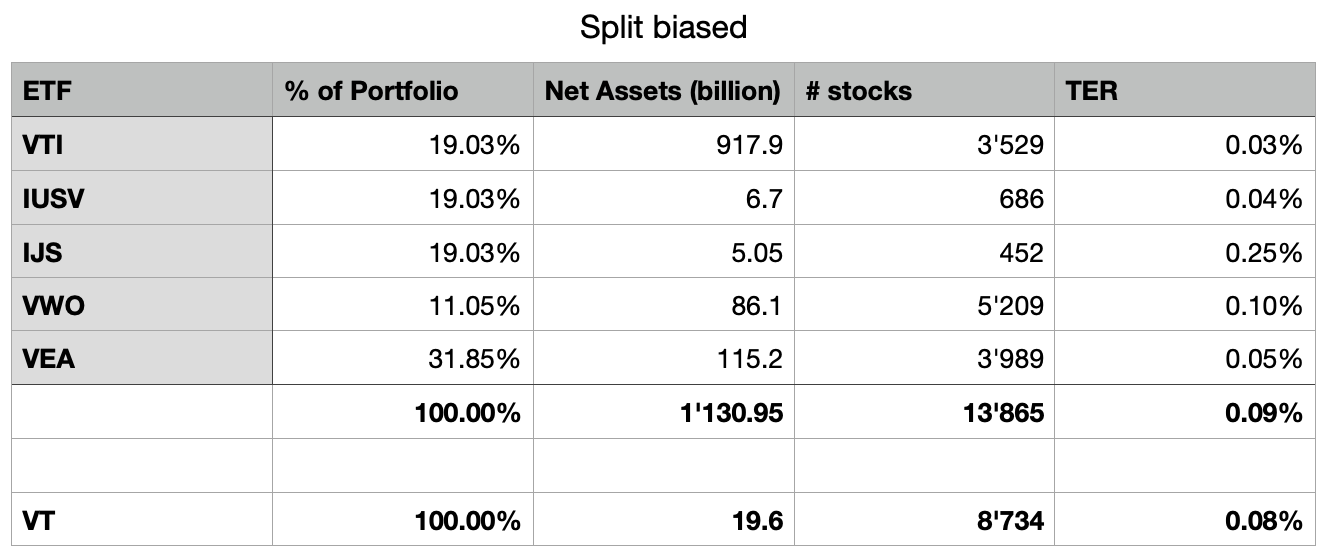

For the portfolio I started with VT, however, since it includes the entire world I would split it up into VTI + VXUS or even VTI + VEA + VWO for a bigger AUM and lower TER.

The next step would then be to apply the bias on the US market by swapping the VTI position for 1/3 VTI + 1/3 IJS + 1/3 ISUV.

Thus I would end up with the following (last row as a comparison w/ VT)

Am I setting myself up for failure or is that an actually sane approach?

Can I simplify it by using VT, ISUV, IJS?

I’m not sure how I would go about defining the percentages…

If I do a 3-way split of VT (ie. VTI + VEA + VWO), should I go with an Europe based ETF for the last two (eg. VDVE & VFEM in IRL)?

From reading the forum and my understanding, in practice it doesn’t make sense for VWO (emerging markets, stick to US ETF) but for VEA it could make sense as half of it is Europe. Is that correct?

Any other thoughts about this approach?

Thank you all for providing so much good and relevant (!!) information and discussion!

I would personally chose VIOV over IJS, but maybe because I’m just a huge Vanguard fan. And I would also try to simplefy it. No need to use VEA and VWO if you plan have the same ratio like VXUS.

Did you read the latest Fama & French paper on factors from January 2020? The value premium in the last 2-3 decades was so small that you couldn’t seperate it from statistical noise, especially with large value. So it begs the question if it even still exists. If it does, it might still be too small to make a significant impact on longterm performance.

There is always a risk of underperforming the market. Large growth annihilated value in general in the last 10 years! The difference in performance was (and still keeps getting) huge. If you can handle to underperform the market for longer periods of time, then sure, you could tilt it like Ben Felix suggested. I just think that the possible premium doesn’t compensate for the risk of underperforming the market.

There is a beauty in just owning the market without any tilts. You’ll never worry about underperformance, you’ll never question your strategy.

I hadn’t but now I read some bits of it and a couple summaries as I don’t really understand everything in the paper. Thanks for pointing it out!

@yakari After reading some more around the forum here and on the web, that’s probably what I’ll end up doing.

I will probably go with VTI + VXUS (as Cortana suggested) instead of plain VT as I keep the flexibility to still do a small cap & value tilt if I decide to later. Plus it’s not a huge increase in transaction cost or time in filling out tax forms.

At first I even wanted to just buy VXUS and wait for a possible change in political landscape in the US to buy VTI (new election and the current economical predictions) but some good articles on the web injected some sense into me and I’m going “all in”, lol.

Now I just need to figure out how to implement all that in IB ^^

ssppooff, nice work. I am also a DIY investor and proud Ben Felix fanboy with similar questions. I can also respond to some of the concerns raised above:

Re: If you owe the whole market, you don’t have to worry about whether factor tilting (the strategy we’re talking about) works. According to Fama and French’s factor model(s), owning the market gets you exposure to market risk which is only 1 of (at least) 5 factors. For more info, watch this.

Re: The value premium is dead. Ben Felix addresses this in his videos. Factors like size, value, and market risk rotate in their contributions to investment returns over time, just like industries. If you look at a longer timeline, the past 20 years isn’t the first time size and value have underperformed market risk for that period of time. It’s actually normal and expected.

Re: once an effective investing strategy is discovered and published, it’s effectiveness vanishes. Factors are not investing strategies and I don’t think they can be abused or arbitraged away, especially in this case. By definition, value stocks cannot be overbought.

Re: Tilting toward tech is speculative. This is actually similar to what Ben Felix would say, but doesn’t it depend on your timeline? Sure, tech is expensive right now if your timeline is 10 years, but what if it’s 30-40 years? QQQ might be an absolute steal right now if that’s your timeline.

Yes.

And on the other hand - if your timeline is 10-15 years (e.g. to FI/RE, and then you ease-out of stocks as an asset), the “trend” of tech overperforming might just last long enough so you profit decently from overweighting it; aka use the momentum.

But - as always - who knows whether it will be so (not many strong arguments against it though).

And btw QQQ is not “just tech”, it’s large growth (although its top 10 and 64% of it are).

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.