I had already asked a similar question in another forum. However, the answers were very different. That’s why I wanted to ask again here.

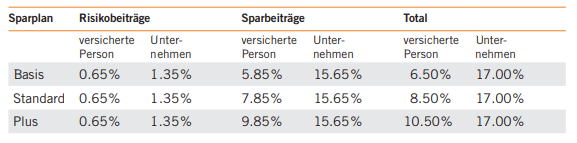

My company’s pension fund has given me the following options for adjusting the savings plan. (33 yo, fulltime, no family, income before taxes 120’000 CHF).

I’m currently on the Standard plan as standard, but I’m thinking about switching to the Basic plan. I currently see the following main advantage.

Advantage: I would have to pay in 2% less and could invest this amount in my ETF portfolio (standard ETFs MSCI World etc.). I could then pay the return generated back into the pension fund shortly before retirement. This would probably exceed the interest earned by the pension fund. The projected interest rate is 2%. In my opinion, it should be possible to exceed that.

In addition, the current interest rate on pension fund deposits:

What else is there to consider? Or do you see any alternatives in this area?

Thanks in advance

PH

Thoughts from others

If you earn a lot and/or live in a tax hell then it might be worth switching to Plus as it lowers your tax burden as everything you pay into the pension fund, you don’t pay tax on and lowers your net income. If you have a high income and pay high taxes, this can make a difference.

Assuming that your goal is to maximize your wealth (= free assets + second pillar + 3a), you can’t get around without doing some simulations. You might be surprised by the results.

Also, what about your assets allocation? Do you want to treat your pension fund balance as fixed income?

Taking money from the pension fund to finance a property purchase is a valid backup exit option, with some drawbacks.

I for myself switched to Basic (I am at MPK as well).

But just since I am not fan of the 2nd pillar (especially with the direction, where it heads to) and want to have as less as possible in there - also aiming to withdraw as early as possible, e.g. by changing the job or doing an early withdrawal through the mortgage process).

my prior employer had a similar offering. I opted to go with the highest contribution option, as they had very high annual returns AND I was planning to cash out some of the funds for real estate. I’ve changed jobs since and have not (yet) take cash out, but might in 2-3 years.

I’d recommend to build a personal opportunity cost model with your numbers (tax rate / savings, projected returns in pension fund vs. ETF investing). Typically the pension fund gets a head start with the tax savings but get’s overtaken by the higher return of an ETF portfolio around 7-10 years down the line. But do your own math.

First, you employer put a lot of money in the pension fund for a 33yo.

The pension fund seems to be very strong to offer 3.75%.

You also need to take into account the tax saved.

Another factor that may not have been discussed yet: the regular additional contributions (under your Plus model) are not same as the make-up / buy-in payments, so they are not blocked for 3 years for home purchase etc.

My employer will start offering a “Plus” plan as well starting next year, and one of the claim they make is that contributing extra via the “Plus” plan will allow for a higher maximum total contribution than via a voluntary purchase.

I asked them if they were sure, but it was “mostly, without anything to back it up”. I tried looking at the website, but it only tells me how much I can contribute extra now.

I thought the max available was strictly based on age * insured salary * fund specific ratio, but maybe it depends on the pension fund? It sounds a bit tricky, as you would need to keep a track of whether the extra-mandatory fund comes from a “direct” contribution, or via a voluntary purchase, but it’s certainly not impossible.

Any ideas?

Fund specific ratio is different for PLUS vs STANDARD. So yes, if you have PLUS, you also have higher “purchase potential” for Voluntary contributions. Typically there are different tables for different options.

They should update your fund regulations and then you would be able to see.

Same here. The fund regulation I know all have 3 buy-in tables in the annex for standard, plus, minus plans.

By changing to, for example +2% contributions in plus, your max buy-in limit can increase from 5% to more than 500% annual salaries, depending on age.

Note that this changes every time. So you could go minus in young years, lower contributions and likely no buy-in, anyway. And when you change your mind, move to standard or plus later on, increasing both.

Yes, if you include early retirement buy backs.

(Based on my work exp in a pension fund)

I have also seen a stat about that, but was not able to find it again.

But we can do a poll on this forum to see how many members have reached the maximum buy backs

Aren’t those kinda restrictive? (esp. if you plan on RE) (I’m close to having a closed gap at max contributions here, not planning on doing early RE buy back tho)

Normally the max is set to the limit as if you had contribute the max each year.

So anyone who contributed the max should be at the maximum buy back. Esp. if the fund performed and had returns on top. In which case, you’d be beyond the max and can’t contribute extra voluntary.

I think mainly those to moved to Switzerland without contribution history, or got promoted to higher salaries have extra headroom for contribution.

But a lot of pension fund plans start when you have 18 yo, so if you went to university, you likely didn’t contribute until 23-25 yo, so these years can be bought back. Same if you were unemployed at some point or took a sabbatical.

Also you salary increases over the year, so you can do buy back of the previous years based on an higher salary.

In short, no.

The only case is if you decide not early retire as you said to the pension fund and stay in the pension. The pension fund could reduce pension.

But currently, some experts disagrees on this point :

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.