We are about to buy a flat in the suburbs of ZH. Here are the numbers:

Flat has a size of 4.5 and approx 120sqm

Age: New will be built within the next 3 years

Location: Very good location with partially lake and mountain-view

Price: 1’660’000 incl. a parkingplace

People: 3 (Ms. Balaclava, our kid and I)

Age: early thirties

Income combined: 200k p.A.

Savings (combined mr and ms Balaclava):

2nd Pillar: 140k

3a: 130k

Bank Account: 60k

Depot 420k mostly VT

No Debt.

I know its a crazy amount for a flat without a helipad, but it checks all the boxes we want and the location is very good, so we decided to go for it.

Now to the questions:

Our plan is to pay 15% while taking out the cash of the 2nd and 3rd pillar, get a 10y mortage and amortize indirectly over 3a again. Is this a realistic scenario?

What mortage-rates can we expect?

Which banks are open to only 10-15% of downpayment?

Is it a whise decision to empty 2nd and 3rd pillar? we think its right since its reduces the opportunity cost compared to selling VT.

How much down must the mortage be if we want to FIRE with lets say 2 MCHF in NW? Will the banks still play the game if the income drops substantially to 80k p.A. ?

What are the questions I should ask but didn’t :-)?

Since I try to contribute here as good as I can, I really hope that some of you with deep expertise in mortages are open to take the time to answer my questions.

As far as I remember none since 20% is the legal minimum. Furthermore, max 10% can come from your 2nd pillar.

Questions : you say it will be built only in three years right ? That would be kind of a terrible deal to pay that money for nothing in advance. Furthermore, I would make sure that everything is properly specified…

On the other hand, you say it is from the thirties, so not sure how to interpret it.

Did you check quality of the main building with a professional (if you are not yourself)

What kind of copropriety it will be ? How is the financial status of the copropriety ?

From what I see, you got the financial power to buy it with a mortgage if you sell some of your VT. Mortgage rate others will be more qualified to reply.

I got a 10y mortgage in 2019 for 0.95% for 10years fixed. I’d assume you could get like 0.9% now?

I got offers from around 4 banks, decided which one I’d like to go with (more sympathetic than the other ones) and showed them the lowest offer I got from another bank. They undercut that offer by 0.05% without any issues.

Furthermore, more important than the interest rate could be flexibility (you have nice bonus possibles, which you could you use for faster down payment if needed)

There’s usually a reservation contract (for me it was a flat 50k CHF) which acts as a letter of intent. Then before the key handover there is the actual purchase contract.

It’s 20% downpayment minimum out of which only 50% can come from Pillar 2 and Pillar 3a. The other 50% have to come from cash or pledged assets.

Today I personally would rather pledge my VT and Pillar 3a to not be out of the market for too long.

Total annual cost 95’173

total annual income 250’000

affordability not given 38%

*) mortgage has to be down to 66% within 15 years

The affordability has to be below 33%. Even though we might have interest rates below 1.5% for the next 10 years, the banks elect to play it safe by calculating 5%. Play around with the UBS mortgage calculator to see how else you can afford it.

At least 10% of the value of the property must not come from Pillar 2. But it can come from the Pillar 3a.

I think this means that you can commit 10% of “hard cash” from 3a and taxable accounts and 23% from the 2nd pillar. This would help with the affordability because you don’t need to amortize.

First of all, fingers crossed that you get well soon!

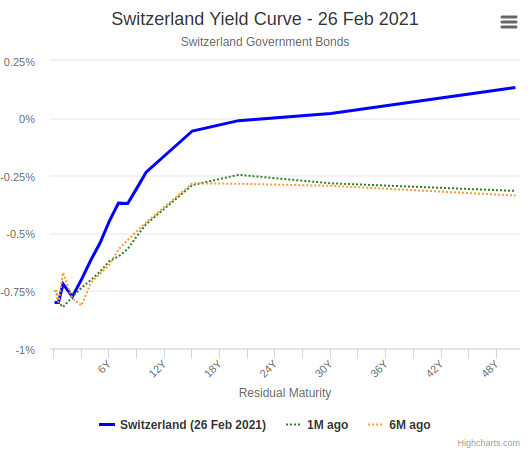

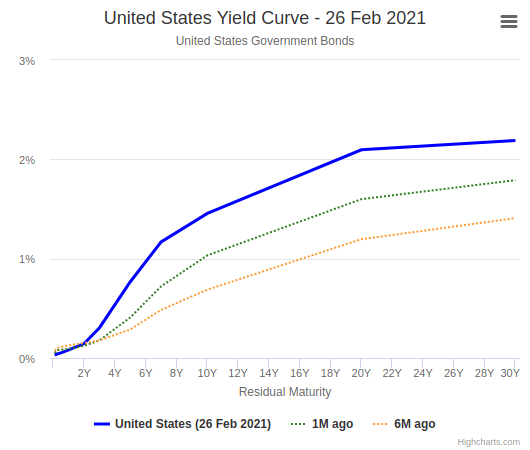

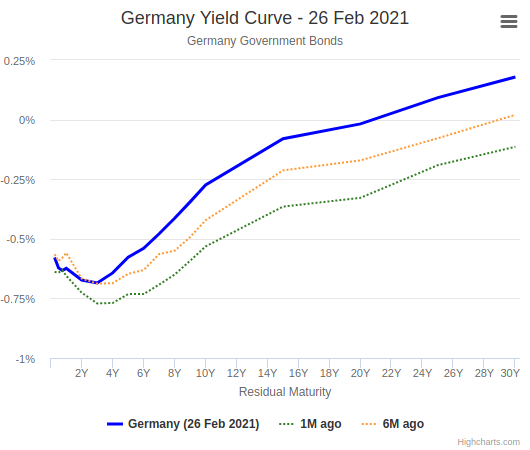

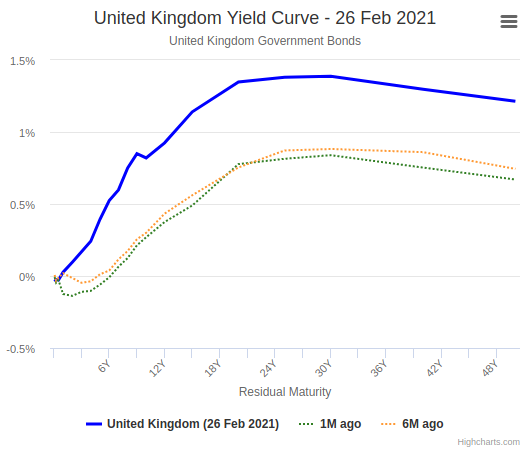

Now to the point - what do you think about what future brings as regards the rates? I guess they went up because of this bonds yield recent behaviour? (I’m asking that I might need the mortgage soon…)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.