While reading the documentation, I’ve noticed that even with 0% fees etf there is some minor Subscription Fees and Redemption Fees.

e.g. CSIF SMI (Subscription Fees : 0,02%; Redemption Fees : 0,02%). Swisscanto SMI (Subscription Fees : 0,01%; Redemption Fees : 0,01%).

You can find bigger differences for CSIF World ex CH Small Cap (Subscription Fees : 0,10%; Redemption Fees : 0,06%).

For the pro hedged CHF ETF, did you make the calculation that the 1% conversion fee to purchase USD ETF create more drag the CHF hedging or is it to keep 40% CHF allocation?

There is no free lunch. Those ETFs with a posted 0.0% TER must earn their money too. In fund classes for institutional clients that is through subscription and redemption as you posted, and certain funds also have special fund classes where they will require individual fee agreements before you can invest in it.

The subscription and redemption fees are there to not dilute existing investors. The money stays in the fund and the asset managers get nothing from these fees. They are solely there to cover the actual costs of buying/selling the underlying securities.

All 0% TER funds have special agreements with the providers selling them/clients using them. The funds wouldn’t be able to cover their ongoing costs just with subscription/redemption spreads.

This is not only an issue with this fund, but an issue in general with them. See also the initial post in this thread. In my opinion, this is some type of FX rip-off: they buy a lot of funds in foreign currencies even when they would be tradable in CHF. For that reason I switched all my Viac accounts to Truewealth, but also Finpension does not use this practice. I know, these costs anly apply when buying and selling, but in my opinion this is not the proper way to handle things.

Viac (which is not the case with Finpension) has deliberately chosen to use fund share classes traded in foreign currency even if CHF share classes are offered by the fund provider.

This has no advantage for the client sand has been done only to get more fees trough exchange fees.

Yes, my understanding is that this is a condition set by Bank WIR, which is the party that benefits from the exchange fees. As the Terzo Vorsorgestiftung is presumably controlled by Bank WIR, it may be difficult for VIAC to renegotiate this, but I don’t know any details. I hope they will manage to improve the situation at some point.

I always wonder if / what other tricks like this are played if I get behind such kind of clearly unfair handling of customers. For me, this leaves a bit of a taste like an “old school bank” which rips off clients in some way, with the hope that clients do not get behind it. The nice thing is that there is some competition in the 3a area now.

So does it then make Finepension an absolute winner being very transparent, having no FX fee practice and more optimized overall, plus located in Schwyz (in case of withdrawal after left the country)? Any absolute pros where VIAC is more beneficial (their insurance and mortgage possibility?).

I think anyone who is below 0.5% fees is going to be good. VIAC was original disrupter I believe , then came Finpension & Frankly. I don’t use VIAC though because I ended up with F&F.

But yes FP seems to be the cheapest in costs. I once read that people were not happy with 1% cash allocation of FP. For me it was not an issue but wanted to point out.

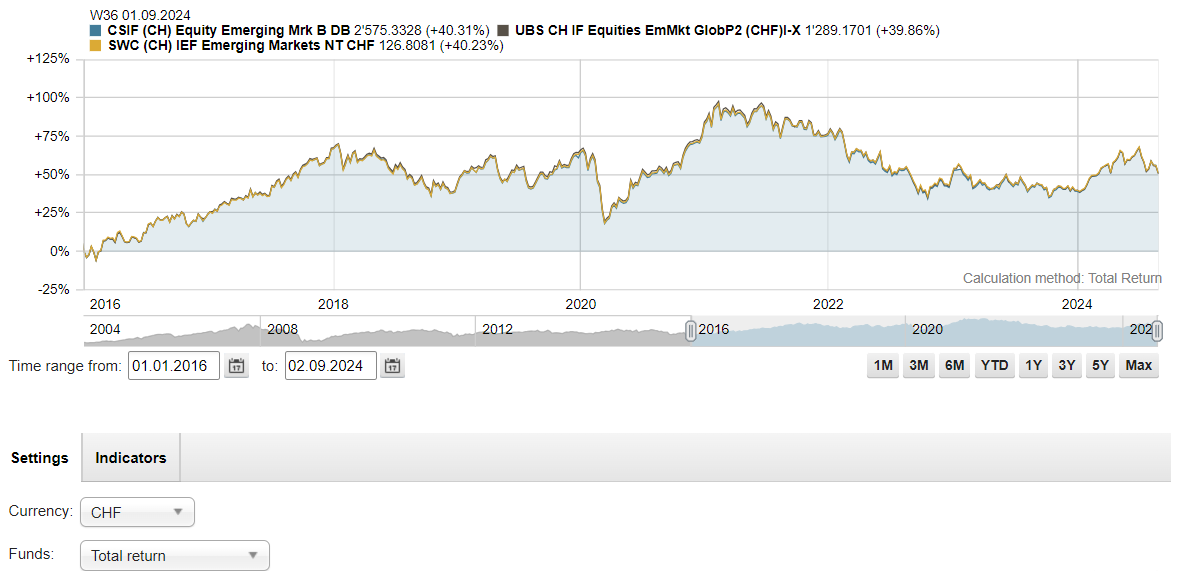

Can you specify the exact funds please, that’s a too large performance difference for index funds.

I know that the UBS one provisions the indian capital gains taxes in the NAV and therfore has a worse performamce and the CS one performs better because the redeeming investors bear the indian capital gains taxes. This makes me wonder why the Swisscanto fund is performing so great in comparison with a low redemption spread. It even outperforms the BM, this seems like they are tracking a different index.

If CS charges capital gains tax at redemption, this means even if investor buy the fund today and sell in 1 year , they have same redemption spread versus someone who bought into the fund 10 years back?

I think something is not adding up.

The total return calculations are showing numbers which are very close.

If CS funds do not accrue the capital gains tax payments to India , then should the NAV not increase much higher than other funds? But since NAV is not increasing much faster, this means something else is acting as a drag?

In the end they have same benchmark index.

Are you sure this high redemption is because of capital gains tax issue or something else could be the case for those redemption values?

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.