Regardless of the product you’ll going to choose. If you plan to buy a house in the near future putting the 3a in a ETF invested product might not be the best choice. Depending on your risk appetite tho…

If you want to invest your 3a money Viac or Finpension are probably the best solutions at the moment, in terms of cost they’re in another league compared to UBS. Search in the forum, there’re plenty of good threads about them.

If you want to keep the money in a saving account (for example as @MrCheese said because you plan to use them for home ownership in few years) you could also consider to move it to another bank for some small improvements in interest rate, I think the best ones offer 0.30%, which would give you an extra 50CHF/year…not sure it’s worth the hassle.

VIAC also has the Account Plus option, with 5% invested in stocks and 95% in a 3A account yielding 0.10%, for 0% fees. So it serves both the conservative and agressive investor.

All in all, they seem to share a lot of FIRE values and offer a range of low fee index funds. Their strategies look well designed to me, I registered wanting to craft a personal strategy out of their range of asset classes (CHF, bonds, different kinds of stocks, real estate, gold) and ended up choosing a standard strategy (global 100).

My only slight concern is that they’re a rather recent actor but they’ve displayed well enough that they know what they’re doing for me to jump on their boat (which I was very reluctant to due to the aforementioned point of their recency). So I’m a new but happy customer of theirs: they’re the 3A solution that aligns the most with my goals and values.

Yes the fees are lower with VIAC but can be compensate with an higher performance of the fund. According my banker

VIAC is a startup, how long it will take for a traditional bank to acquire VIAC ?

I plan to keep this money on my account at least for the next 10 years and my risk appetite is high.

They’re already basically part of WIR bank. And if they are ever acquired by someone else who drastically changes the fee structure it would be very easy to move your money somewhere else.

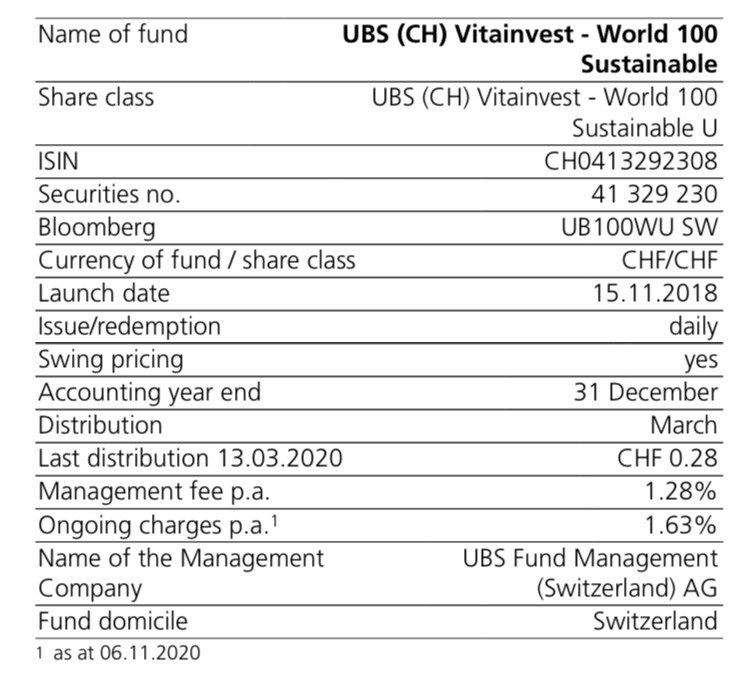

If you want to compare something that could be interesting, it would be the difference with same performance and lower fee like this graphique from Frankly, another provider of 3a that is similar to the Vitainvest as they have 70% of the fund hedged in CHF.

But if you are looking to buy an house in the next 10 years, yes maybe already have an UBS Solution could help you to take a mortgage with them; not sure if they will be the better ?

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.